Dominican Republic

The Dominican Republic’s First Oil and Gas Licensing Round was concluded November 27 with the award to Apache Dominican Republic Corp, a subsidiary of Apache Corp, of the SP2 block offshore in the San Pedro de Macorís basin.

The other areas proposed by the MEM in this first round were declared void and will be available for the next round. The terms and conditions, as well as the Round 2 schedule will be published in the days following the conclusion of this first process. The areas to be auctioned in Round 2 will be the areas not assigned in Round 1 as well as those that are proposed by stakeholders and approved by the MEM within the process schedule of Round 2.

Source: Dominican Republic Licensing Round

API applaud North American trade deal

WASHINGTON –

The American Petroleum Institute issued the following statement after Democrats announced a deal with the administration to finalize the U.S.-Mexico-Canada Agreement (USMCA), clearing the way for congressional approval of the revised trade pact.

“We applaud the bipartisan consensus reached on USMCA,” said API president and CEO Mike Sommers. “Canada and Mexico are our top energy partners, and maintaining the tariff-free flow of natural gas, oil and refined products will help ensure that American families have continued access to affordable and reliable energy, strengthen U.S. energy leadership and grow the economy. This isn’t just about the potential impact to the U.S. energy industry—but also to small businesses, manufacturers and U.S. jobs. We urge Congress to take up and pass this bipartisan agreement.”

API joined over 200 companies and associations covering a wide range of industries in the USMCA Coalition, which has been working to secure the agreement’s approval in Congress. The coalition’s broad membership helps illustrate the wide, positive impact of free trade across the U.S. economy.

API

-National Petroleum Council Reports

New research underscores opportunities to sustain U.S. energy leadership and environmental progress

The American Petroleum Institute hailed two reports by the National Petroleum Council that demonstrate how the United States can address the dual challenge of providing affordable, reliable energy while mitigating risks of climate change by advancing carbon capture, utilization and storage and spurring investments in new energy infrastructure.

The NPC, first organized during World War II, is a federally chartered committee that advises the secretary of energy and the administration on energy policies.

“Our industry is leading the way in meeting the world’s growing energy demand while delivering solutions to reduce greenhouse gas emissions,” API president and CEO Mike Sommers said. “The natural gas and oil industry continues to drive emissions to their lowest levels in a generation, and as this study shows, we can build on this progress by fostering collaboration between the private and public sectors and advancing CCUS research and development. We urge Congress to make bipartisan CCUS legislation a priority and support innovative efforts to reduce emissions and achieve environmental progress.”

The United States is uniquely positioned as the world leader in CCUS and has substantial capability to drive widespread deployment. API supports bipartisan legislation to incentivize research and development of CCUS, including The USE IT Act (S. 383), introduced by Sen. Barrasso (R-WY) and Sen. Whitehouse (D-RI) and The LEADING Act (S. 1685), introduced by Sen. Cornyn (R-TX) and Sen. Coons (D-DE).

NPC found that America’s largest energy sources will continue to be natural gas and oil through at least 2040 and highlighted the need for new infrastructure to maintain affordable and reliable energy for all Americans.

“Investing in energy infrastructure is essential to sustaining and growing America’s energy leadership, keeping energy costs low for working families and promoting economic development,” Sommers said. “But red tape is stalling infrastructure projects not just in the energy industry, but across the entire U.S. economy. As we consider ways to unlock America’s infrastructure potential, modernizing the National Environmental Policy Act’s maze of permitting rules is a necessary step to ensure safe and environmentally responsible development of the nation’s vast energy resources.”

Overlapping and duplicative regulatory requirements, inconsistencies across multiple federal and state agencies, and unnecessarily lengthy administrative procedures have created a complex and unpredictable permitting process. While there have been bipartisan actions by Congress and the Executive Branch to expedite the permitting process, more improvements are necessary.”

USA BLACKLISTED SIX TANKERS

(REUTERS) – The Trump administration blacklisted six oil tankers involved in the shipment of Venezuelan oil to Cuba, the latest in a series of sanctions aimed at pressuring Havana to abandon its support for socialist Venezuelan President Nicolas Maduro.

Six vessels belonging to soc PDVSA, were targeted, according to a statement from the U.S. Treasury Department.

“Cuba and the former Maduro regime continue trying to circumvent sanctions by changing the names of vessels and facilitating the movement of oil from Venezuela to Cuba,” said Treasury Deputy Secretary Justin Muzinich.

“The United States will continue to take necessary action to protect the people of Venezuela,” he added.

The Treasury Department also identified a vessel named Esperanza as property of blacklisted Caroil Transport Marine Ltd and said it was previously designated under the name Nedas.

The United States and more than 50 other countries have recognized Venezuelan opposition leader Juan Guaido as the legitimate president. Guaido invoked the constitution to assume a rival presidency in January, arguing Maduro’s 2018 re-election was a sham.

But Maduro retains the support of the military, runs the government’s day-to-day operations and is backed by Russia, China and Cuba.

“Cuba continues to prop up Nicolas Maduro, subverting the Venezuelan people’s right to self-determination and undermining Venezuelan institutions,” U.S. Secretary of State Mike Pompeo said in a statement on the latest sanctions.

Pompeo said Caracas ships oil to Cuba in exchange for security and intelligence assistance from Havana that supports Maduro.

Under the latest sanctions, Americans are prohibited from engaging in transactions that involve the blacklisted vessels.

(Reporting by Daphne Psaledakis and Doina Chiacu; Editing by Matt Spetalnick, Steve Orlofsky and Jonathan Oatis)

Venezuela investors lose hope in 2019

The Financial Times Colby Smith in New York DECEMBER 20 2019

‘Hardcore fear of missing out’ prompted a big rally that did not last.

Early in 2019, Venezuela’s bondholders felt something they had not in quite some time: optimism. Authoritarian leader Nicolás Maduro’s grasp on power was slipping, after more than a year with the majority of the country’s bonds in default. Regime change looked imminent, with the rise of Juan Guaidó, the president of Venezuela’s congress, who had the backing of the US and 50 other nations.

The hope was that a new leader would bring new policies that would help put an end to the humanitarian crisis sweeping the country. Growth would return and after Venezuela had some breathing room to rebuild its ravaged economy, a path would be forged for a restructuring to untangle the country’s whopping $150bn debt burden. Such hopes helped to fuel an over 40 per cent rally in the bonds in January, albeit from a low base. The country’s benchmark dollar bond maturing in 2027 saw its price surge above 30 cents on the dollar for the first time since 2017.

Those issued by the state oil company PDVSA also jumped, with some notes trading as high as 25 cents on the dollar. But the rally, driven by “hardcore fear-of-missing-out” proved to be fleeting. On the eve of 2020, with Mr Guaidó’s momentum flagging, optimism appears to be in even shorter supply as bondholders settle in for another year of stasis. “It has not been a good year for bondholders in Venezuela,” said Caracas Capital Management. “There is no way you can put a silver lining on it.”

Within days of January’s rally, Venezuela’s bondholders, which include Fidelity, T Rowe Price, BlackRock and Pimco, received the first of a string of surprises — all of which helped to strip the price of the sovereign and PDVSA’s bonds down to their current levels of roughly 10 cents and 8 cents on the dollar, respectively. In an effort to cut off the flow of foreign currency to the regime, Washington announced sweeping sanctions on PDVSA at the start of 2019, banning US citizens from buying any debt linked to the state-oil company. Less than a week later, the US Treasury’s Office of Foreign Assets Control (Ofac) extended those rules to the country’s sovereign bonds. US creditors could still hold the debt, but the only people they could sell it to were foreigners.

The restrictions brought trading to a halt and sparked a protracted, yet ultimately fruitless effort by one bondholder group holding roughly $8bn of the country’s debt to compel the Treasury department to address what it believed was an “ill-advised” trading ban that risked forcing the bonds into “rogue” foreign hands.

JPMorgan landed another blow in July when it announced it would wind down the weighting of Venezuelan debt from its widely followed emerging market bond benchmarks. Pressure mounted on index-tracking US investors to sell their positions into the broken market at extremely distressed prices.

“We all knew the risk we were taking in buying defaulted Venezuelan or PDVSA debt, but the surprise was the Ofac sanctions,” said one international bondholder. “These sanctions were just a disaster, and all this has done is damage the holders of the bonds, many of which manage money for US pensioners.”

The Treasury waded in once again in October ahead of a widely anticipated default of debt issued by PDVSA maturing in 2020. The department barred bondholders for three months from collecting on their collateral — Citgo, the crown jewel of Venezuela’s oil industry.

The interim government followed up days later with a lawsuit against the investors, claiming the debt should be annulled. Creditors have since accelerated the bond, meaning the more than $1.8bn owed by PDVSA is now due. The PDVSA 2020 saga is not the only litigation between creditors and the country.

As Duke University law professor Mitu Gulati warned, the type of people snapping up Venezuelan debt at pennies on the dollar will be “litigation specialists”. More than a dozen lawsuits have been filed by bondholders since 2018, including a joint case involving six hedge funds over missed payments on debt maturing in 2034 and a $128m claim from Contrarian Capital, a Connecticut-based hedge fund.

According to Mr Dallen, the number of lawsuits is set to rise significantly next year, as bondholders seek to ensure that their claims — some of which begin to expire three years after a default with no legal action — remain valid.

“We will see multiples of what we see now,” he cautioned.

But with regime change stalled, US sanctions firmly in place and protective measures enforced to shield one of Venezuela’s last-remaining coveted assets, creditors will be unlikely to feel much besides disappointment in the year ahead.

VENEZUELA FEELS THE HEAT

Punishing US sanctions will continue to inflict heavy losses on the country’s oil sector

(Petroleum Economist et al)

The Venezuela oil industry has been on a death spiral since 2016, with is roots in the short-sighted policies of presidents Hugo Chavez (1999-2013) and his successor Nicolas Maduro—made worse by the oil price fall of 2014. Both presidents destroyed the national oil company by politicising it, firing its most qualified workers and over-extracting resources from it.

The partial expropriation of private operators and service contractors discouraged foreign investment in new projects. In 2019, the collapse trajectory was exacerbated by the imposition of oil sale sanctions by the US. In the last quarter of 2019, production had fallen to c.650,000-700,000bl/d, about half of the 1.3mn bl/d a year. In Maracaibo, PDVSA rarely reports oil spills. The plight of fishermen is one case among 7 million requiring humanitarian aid.

Tons of waste are dumped in the bay. The lake is infested with weed. Polution threatens species and risks disaster for the rich biodiversity of reptiles, birds, mammals and shellfish.

Venezuela increases oil output

OPEC announced that oil pumping in Venezuela in November reached 697.000 bpd. But one country’s increase in production may not have a positive impact in the near future in view of OPEC’s decision to curb output in an attempt to keep inventories at a level that holds profit margins attractive.

The Organization of Petroleum Exporting Countries reported a gradual recovery in Venezuela’s oil production in Venezuela with a figure of 912,000 barrels per day (bpd), 151,000 above October’s output, as the Venezuelan Government continues to target February’s 1.4 million barrels.

Economic sanctions imposed by the United States affect the well-being of Venezuela where oil played a crucial role in world development. Being able to meet the future global demand for oil depends on countries like Venezuela. Imposition of sanctions on Venezuela is also an imposition on OPEC, other producing countries and the world oil industry . The best years are yet to come, Venezuela has a bright future, it is a very rich country, with a very enterprising and educated people. .

In spite of OPEC’s latest agreement with its allies to further reduce the output of crude oil, inventories could go up worldwide, the International Energy Agency (IEA) said .

Analysts also estimated in London that a cut in pumping planned by the United States and other countries outside OPEC further lead expectations in that direction.

“Despite the additional reductions (…) and a reduction in our forecast of supply growth outside of OPEC in 2020 to 2.1 million barrels per day (bpd), global crude oil inventories could amount to 700,000 bpd in the first quarter of 2020,” said the Paris-based IEA in a monthly report.

In Tokyo, crude oil prices rose , recovering some of the losses on the previous day after the increase in inventories in the United States, as the market changed its tone and opted for relief after that OPEC predicted a supply deficit next year.

Brent international benchmark futures earned 28 cents or 0.44%, at $ 64 a barrel, after losing 1% due to the increase in oil inventories in the United States, while the futures of the West Texas Intermediate in the United States (WTI) improved 8 cents, or 0.14%, to $ 58.84 a barrel, after yielding 0.8% the previous day.

ROSNEFT ON VENEZUELA SERVICE CONTRACTS

BY FABIOLA ZERPA CARACAS (BLOOMBERG) –

A Rosneft subsidiary took over contract discussions with local service providers , replacing PDVSA on joint projects with the SOC. The move is a major turnabout for PDVSA, which in the past typically operated all aspects of the joint ventures.

Previous advances yielded key activities to Rosneft, underscoring Russia’s growing influence in Venezuela’s oil industry. PDVSA was forced to cede more control amid an exodus of experienced workers, corruption and lack of investment that has driven production down to less than 800,000 bpd in October from more than 2.5 MMbpd in 2015.

The Russian major is entering to reinforce current assets and expand its presence in the country as some partners such as China National Petroleum Corp. have signaled reluctance. CNPC affiliates have shied away from construction works and projects at oil facilities.

PDVSA and Rosneft plan to boost production at three of their five joint ventures — Petromonagas, Petrovictoria and Petromiranda — that were hit by power failures and U.S. sanctions. Rosneft now trades much of Venezuela’s oil from an office in Panama staffed with former PDVSA employees.

Rosneft receives oil as part of its joint ventures with PDVSA, and also as repayment for loans. It is not subject to U.S. sanctions that restrict American refiners from importing Venezuelan crude. Most international oil companies and trading houses avoided buying oil from PDVSA since the sanctions were imposed.

Precision Drilling de Venezuela, previously owned by Weatherford International Plc and now wholly owned by Rosneft, is approaching local companies including holding discussions on scope of work and potential payment in rubles. .

Maduro to relaunch Petrocaribe program in 2020

Havana 15 Dec 2019

Nicolas Maduro told the closing event of the 17th Bolivarian Alliance for the Peoples of Our America (ALBA) summit, in Cuba that Venezuela would “relaunch the Petrocaribe project in the first half of 2020 with great vigor.”

The program was launched on June 29, 2005, by former President Hugo Chavez, under which the country supplies oil to other Caribbean countries on favorable financing terms.”We have decided to relaunch with great force for the first half of the year 2020, the PetroCaribe project, the Miracle Mission and ALBA Cultural (…) ALBA has demonstrated the practical capacity to impact in the lives of our peoples,” Maduro declared.

The historic agreement allowed Caribbean nations access to gas and oil without the adverse consequences of intermediation, prevailing market prices, and speculation. Chavez’s idea was the resolve “asymmetries in access to energy resources through new favorable, equitable and fair exchange schemes between the countries of the Caribbean region,” without state control of the supply of resources.

The payment system allows for the purchase of oil at market value for five to 50 percent upfront with a grace period of one to two years, the remainder can be paid through a 17-25 year financing agreement with one percent interest rates if oil prices are above US$40 per barrel.

If these countries lack the liquidity to pay off what’s owed, Venezuela makes an exception by accepting payment in goods and services. For instance, Cuba pays part of its through medical, educational, and athletic services, while Nicaragua pays with meat and milk.

During the ALBA summit, Maduro urged the international body and its member-states to also relaunch the social program Operation Miracle, which offers ophthalmologic procedures and eyecare for impoverished countries and communities in the region. There are a total of 17 members; 12 of the members are from the 15 member Caribbean Community (excluding Barbados, Montserrat, and Trinidad and Tobago). The others are Cuba, Nicaragua, the Dominican Republic, Bahamas, and Haiti.

It was launched in 2004 by late revolutionary leaders, Fidel Castro, and Chavez. During its first year, only Venezuelan patients were treated but in 2005 it was extended to other Caribbean, Central and South American countries. Initially, patients had to travel to Cuba for treatment, but in 2006 the program set up ophthalmology centers in several nations, which as right-wing governments took over were dismantled.

The program offers 100 percent free optometry consultations, exams, surgeries and medications to low-income people.

CITGO REPORTS $215 MILLION NET INCOME

HOUSTON — CITGO Petroleum Corporation reported strong financial and operational performance as the Board of Directors reviewed with the Shareholder the company’s performance during the first nine months of 2019 at CITGO headquarters in Houston.

CITGO Petroleum Corporation reported strong financial and operational performance as the Board of Directors reviewed with the Shareholder the company’s performance during the first nine months of 2019 at CITGO headquarters in Houston.

The report included net income of $270 million for the first nine months of 2019, $215 million in the third quarter, all during a particularly challenging time to many Gulf Coast refiners. The report also reflected an approximate 20,000 barrels per day (bpd) increase in refining capacity. This increase is just the second refinery capacity increase in 20 years.

CITGO is also on pace to have one of the best years in its history in terms of safety and environmental performance, which remain vital core values of the company. Additional operational and performance highlights include:

- — Refinery output. Total refinery throughput in Q3 was 825,000 barrels-per-day (bpd) of which crude runs were 724,000 bpd, utilizing 94% of rated crude refining capacity. Additional intermediate feedstocks accounted for 101,000 bpd. YTD refinery throughput was 784,000 bpd, of which crude was 676,000 bpd and intermediate feedstocks totaled 108,000 bpd.

- — Enhanced flexibility. Due to the flexibility of its refineries, the company continued maximizing margins through purchases of economical crudes. Q3 domestic crude runs in the Gulf Coast averaged 366,000 bpd, setting a new quarterly record assisted by the additional light crude processing capability added during the recent Corpus Christi refinery turnaround.

- — Increased exports. The company continued to take advantage of the location of its Gulf Coast refineries by increasing participation in export markets, which now represent 36% of Gulf Coast light fuels production.

- — Corporate governance. Since its appointment in early 2019, the Board has instituted a number of measures to enhance corporate governance, including a review of the company’s regulatory compliance system and a comprehensive audit.

“CITGO’s strong performance is a testament to the dedicated efforts of our Board, management team and employees,” said CITGO Board Chair Dr. Luisa Palacios. “Throughout 2019 we have worked diligently to strengthen the company — building financial strength, operational flexibility and sounder corporate governance. These efforts should continue to pay off as we look to 2020.“

President and Chief Executive Officer Carlos Jorda said, “While we have faced many challenges this year, we remain committed to making and selling quality products, serving our customers and supporting our communities. This focus, in combination with the Board’s leadership, positions us for continued success.”

IMF :- THE KINGDOM OF THE NETHERLANDS — CURAÇAO AND SINT MAARTEN:

December 2, 2019

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF’s Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

The monetary union of Curaçao and Sint Maarten (the Union) has been grappling with negative shocks and is facing significant challenges. Curaçao is in a protracted recession owing to significant spillovers from the Venezuela crisis, which has exposed long-standing structural rigidities and weaknesses in public finances. Sint Maarten’s recovery after the devastating 2017 hurricanes has been uneven, given small island constraints and structural impediments exacerbated by frequent bouts of political instability. Wide-ranging reforms are needed in both countries.

I. Recent Developments and Short-term Outlook

Curaçao

Curaçao is facing a fourth year of recession due to continued spillovers from the Venezuela crisis. Despite robust growth in tourism, real GDP declined by 2.2 percent in 2018 as the Isla refinery effectively shut down production in the first half of 2018, negatively affecting supporting sectors (although largely retaining its direct employment). The unemployment rate increased to 21.2 percent in early 2019 and GDP is expected to fall by 2 percent this year. Inflation increased to 2.7 percent in October 2019, in part due to switching to more expensive fuel suppliers and tax measures introduced in September.

Curaçao’s fiscal position improved in 2018 following expenditure containment measures, but still fell short of meeting the fiscal rule. Zero indexation and tighter transfers reduced the current fiscal deficit in 2018, but still triggered an Instruction from the Kingdom in 2019 as it fell short of the balanced current account rule. In 2019, the government also signed the Growth Accord with the Netherlands setting out revenue and expenditure measures, implemented short-term revenue measures and introduced a 3:1 attrition rule for central government employment. These measures and a one-off tax windfall from the tax sharing system with the Netherlands led to a fiscal current account surplus in the first 9 months of 2019.

The recession is projected to deepen in 2020 . Based on a cautious assumption that the refinery will close in end-2019 when the contract with PDVSA expires, GDP could contract by 4½ percent in 2020 despite a positive contribution from tourism. Inflation is projected to accelerate to 3.7 percent in 2020 driven by indirect tax measures.

Sint Maarten

Sint Maarten is gradually recovering from the devastating 2017 hurricanes. GDP fell by an estimated cumulative 16.9 percent in 2017−18 as tourism plummeted, although a construction surge financed by large private insurance payouts partially mitigated the shock. A recovery of tourism in 2019 is projected to support GDP growth of 5 percent, although the broad recovery is constrained by the gradual absorption of Trust Fund resources. Inflation is estimated to have increased to 2.9 percent in 2018, in part driven by higher oil prices, but declined to 0.6 percent in the first half of 2019 according to published data.

Due to the hurricanes, the overall fiscal deficit widened to 3¾ percent of GDP in 2018 but started to improve this year . Revenue has been recovering while spending remained contained, largely due to delays in capital spending. None of the budgeted capital projects, including the tax and public financial management (PFM) reforms, have been implemented so far due to the late budget approval and a delay in external project financing. Without liquidity support, the fiscal liquidity buffer is likely to decrease in Q4 due to scheduled payments, posing the risk of payment arrears. Staff estimates that government debt increased from 44½ to 53¾ percent of GDP between 2016 and 2018.

Real GDP is likely to grow by nearly 3 percent in 2020. The projections assume that the airport and hotel reconstruction will be completed by 2022, leading to a continued recovery in stayover tourism. Cruise tourism is however expected to decline in 2020 due to scheduled changes in cruise itineraries. Inflation is expected to ease to 1.3 percent in 2019, driven by low resource utilization and international prices and remain around 2 percent afterwards in line with U.S. inflation.

The Union

The external position of the Union worsened in 2018. The current account deficit (CAD) widened to 20.6 percent of the union GDP driven by stronger imports in Curaçao, in part due to a higher oil bill. In addition, the trade balance in Sint Maarten was affected by 2017 hurricanes as they reduced exports, particularly receipts from tourism and increased imports. Staff estimated that external debt reached 174 percent of union GDP in 2018. International reserves declined from 4.1 to 3.7 months of imports of goods and services between end-2018 and mid-October 2019. The pressure on reserves was cushioned in part by substantial drawdown of foreign assets of the private sector. The external position of both countries is assessed to be weaker than warranted by fundamentals and desired policy settings.

II. Pursuing Fiscal Reforms and Strengthening the Framework

The Growth Accord between Curaçao authorities and the Netherlands presents an opportunity to improve public finances. Staff’s baseline projections assume a rollout of the new general spending tax (ABB), continuation of wage policies, the implementation of an early retirement plan for civil servants and containment of other expenditure in 2020. Despite the measures, the overall fiscal deficit is projected to expand to 3.7 percent of GDP as the recession deepens.

Consistent implementation of good quality measures will be key for reaching medium-term sustainability in Curaçao. The authorities should consider broadening the ABB’s base to domestically produced goods in conjunction with a comprehensive tax offset mechanism, in line with advice from the recent IMF technical assistance mission. The early retirement program should be accompanied by a broader civil service reform that structurally reduces the number of positions to secure long-term savings.

Moreover, Curaçao would benefit from implementation of PFM reforms, including strengthening of expenditure controls and better incorporation of fiscal risks. The authorities should compile timely information on balance sheets of all public sector entities and keep track of arrears and guarantees. An envisaged investment guarantee fund (Invest-Curaçao) involves significant risks and would require a cautious approach, including proper risk management and strong supervision capable of assessing the risks. Strong public communication of measures is critical for their social acceptance.

In Sint Maarten, the sustainability of public finances hinges on the implementation of several critical reforms. The authorities have prepared plans in many areas such as tax policy and tax administration, PFM and pension and health systems, but their implementation has been lagging, in part due to political differences and lack of financing. Suboptimal organizational structures and procedures and outdated IT systems pose fiscal and business continuity risks. The revenue and PFM reforms need to be implemented as a matter of priority and it is critical to secure financing for their implementation. These reforms would help with fiscal consolidation and support the authorities’ efforts to eliminate the endemic arrears to the domestic sector. Reforming the civil service pension system should improve its sustainability and generate budget savings. The current health system is financially unsustainable, and its envisaged reform is a step in the right direction, although it needs to be done in a way that prevents long-term fiscal risks.

Both countries would benefit from introducing long-term fiscal anchors and broader Fiscal Responsibility Frameworks. The government debt-to-GDP ratios could be used as long-term anchors supported by operational rules with targets for the primary balance and current expenditure. The debt target should be set at a relatively low level (for instance 40 percent of GDP), which would provide more fiscal space in the event of negative external shocks. Due to significant external risks, the framework should contain clearly articulated escape clauses defining the circumstances justifying deviations from targets while retaining sustainable policies. As meeting a long-term fiscal anchor would require primary surpluses, it might be compatible with the golden rule over a longer time horizon, although compensation for past deficits could take longer than envisaged in the current framework.

III. Pursuing a Supportive Monetary Policy and Strengthening the Financial Sector

Monetary policy needs to support the exchange rate peg. In the short term, the CBCS should develop the policy rate communicating the stance of monetary policy in line with recent IMF technical assistance and be prepared to increase interest rates to prevent capital outflows. Monetary policy instruments and operations need further development: the CBCS should widen operations with its certificates of deposit and introduce an overnight credit standing facility. The governments of Curaçao and Sint Maarten should consider operationalizing the Treasury Single Accounts in the CBCS. Over the longer term, the authorities should consider revising the current standing subscription framework to allow the development of domestic debt markets.

Financial system vulnerabilities need to be addressed. The protracted recession has increased financial system fragilities in Curaçao. Whereas the system-wide capital buffer is at its regulatory minimum, it varies across banks. The authorities should agree on a plan to address fragilities as a matter of priority and encourage higher provisions against non-performing loans. A comprehensive review of the bank resolution framework and strengthening of supervision are needed to improve governance in the financial sector. To improve transparency, the CBCS should prepare and publish a Financial Stability Report. The authorities should prioritize efforts to bolster stability of the financial system over seeking progress in the fintech area.

IV. Enhancing Potential Growth, Overcoming Small Island Constraints, and Strengthening Resilience to Natural Disasters

In both countries, broad structural reforms are needed to address long-standing structural impediments and increase potential growth. Reform priorities include improving the business environment (facilitating construction and other permits, business licenses and cutting red tape); increasing labor market flexibility while fine-tuning safety nets and addressing skills gaps; and boosting the implementation capacity of the public sector. Both countries should update their tourism master plans setting out a long-term vision for the sector. Sint Maarten should continue its rebuilding efforts with the “Build Back Better” principle and develop a comprehensive Disaster Resilience Strategy drawing on the expertise of international partners. Moreover, stronger economic integration in the Union, e.g. building common institutions such as financial sector infrastructure, would improve resource allocation and the functioning of the Union.

V. Strengthening Governance

Both countries need improvements in governance frameworks. The recent passage of AML/CFT legislation in Sint Maarten is an important step in the right direction. In both countries, effective implementation of the AML/CFT framework will be key for reducing risks. Both countries need to provide adequate resources to the relevant AML/CFT entities and increase public awareness of the issues, e.g. through a national forum. The national risks assessments in both countries will be instrumental for detecting gaps. To reduce opportunities for corruption, both countries need to strengthen institutions and ensure strong implementation of existing laws and procedures. The authorities should make efforts to operationalize the Integrity Chambers.

VI. Medium-Term Outlook and Risks

Curaçao’s medium-term outlook is challenging. Marginal growth would stabilize at suboptimal ½ percent in the medium term, reflecting weak productivity growth. Despite the fiscal measures assumed in the baseline projections, current fiscal deficits may persist through 2024, implying a sizeable financing gap over the projection period in the absence of financing. Government debt would increase to 62.1 percent of GDP in 2021 and decline only gradually to 61.1 percent of GDP by 2024. Debt sustainability could be subject to risks stemming from contingent liabilities.

In Sint Maarten, fiscal deficits are likely to persist despite the continued economic recovery. GDP is likely to converge to around 2 percent over the medium term, supported by a gradual improvement in aid absorption.Better tax administration and revenue growth reflecting the post-hurricane recovery would help increase tax revenue from 18⅔ percent of GDP in 2018 to 20⅔ percent of GDP in 2024. However, given the slow pace of reforms, the current fiscal deficits in Sint Maarten are likely to persist through 2023. Government debt would increase to 60⅓ percent of GDP by 2024 in part due to the airport reconstruction loan from the European Investment Bank.

The Union’s external position would remain weak. The Union’s CAD is projected to decline from 20.6 percent of GDP in 2018 to 11.2 percent of GDP by 2024. The external debt of the Union is projected to increase to slightly above 190 percent of GDP in the medium term, although the risks are mitigated by substantial foreign assets.

There are risks to the projected growth outlook both in Curaçao and Sint Maarten. In Curaçao, finding a new operator for the refinery would improve the short-term outlook significantly. On the downside, a closure of the refinery and the planned fiscal adjustment measures could deepen the recession more than projected. Delays in putting together a consistent and credible framework supported by broad-based fiscal and structural measures could exert pressure on the exchange rate. In Sint Maarten,political instability and small island capacity constraints could delay reconstruction of the airport, constrain absorption of the TF resources, and stall critical reforms, which would delay the recovery and undermine the sustainability of public finances. Sint Maarten also remains vulnerable to natural disasters. On the other hand, tourism recovery and growth effects from airport reconstruction could be stronger than expected. Weaker growth in the U.S. and the EU could reduce tourism and growth in both economies.

As an illustration, staff developed alternative scenarios in which both countries reach the debt target of 40 percent of GDP in 10 years in order to bolster debt sustainability. In Sint Maarten, this objective—in conjunction with building a fiscal buffer—would require achieving a primary surplus excluding grants of about 0.9 of GDP by 2024, requiring an ambitious additional fiscal consolidation of 2.1 percent of GDP relative to the baseline projections. In Curaçao, this objective would need a primary surplus of slightly over 2 percent of GDP by 2024, requiring additional fiscal adjustment of around 2¼ percent of GDP, although stronger growth or a longer timeframe would reduce the needed fiscal adjustment. A gradual adjustment approach would be preferable, although it depends on availability of financing. To avoid increasing the tax burden further, additional fiscal measures should be focused on expenditure.

VII. Capacity Building and Improving the Data Framework

Significant capacity building supported by adequate resources is needed to enable the reforms. In both countries, capacity limitations constrain policy implementation and lead to data gaps that hamper effective macroeconomic analysis and surveillance. Better planning, addressing the weaknesses in IT systems, tax administration, and PFM would improve policy implementation and contribute to stronger growth. Given capacity limitations, both countries need to set priorities and realistic timelines supported by accountability for implementation. In Sint Maarten, building macro-fiscal capacity would aid budget preparation and overall policy making. The recently acquired membership in CARTAC by Sint Maarten presents an opportunity to support the authorities’ capacity building efforts. In both countries, major improvements in statistics are needed to inform policymaking. The authorities should address the shortages of human and financing resources limiting data collection coverage and timeliness, particularly for the National Accounts in both Curaçao and Sint Maarten.

The mission expresses gratitude to all Curaçao and Sint Maarten authorities and all counterparts for their warm hospitality, cooperation and candor.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: RANDA ELNAGAR

PHONE: +1 202 623-7100EMAIL: [email protected]

ORGANISATION OF AFRICAN, CARIBBEAN AND PACIFIC STATES (OACPS).

The African, Caribbean and Pacific (ACP) Group yesterday ended a two-day summit here, agreeing to rename the 45-year-old organisation as the Organisation of African, Caribbean and Pacific States (OACPS).

The organisation is now better positioned to counter the policies of more developed nations.

“We could best be seen and eventually evolve and grow into the counterfoil to what is the OECD — the Organisation for Economic Cooperation and Development. That’s the club; they do a lot of analytical work.”

“The OACPS will be the counterfoil, the voice of t.. developing countries, in the analytical work, in the policymaking..The OECD, looks after the club of .. developed countries, and now some that are developing are also going in that direction.”

The OECD is an intergovernmental economic organisation with 36 member countries, founded in 1961 to stimulate economic progress and world trade. It is a forum of countries e committed to democracy and the market economy, providing a platform to compare policy experiences, seek answers to common problems, identify good practices, and coordinate domestic and international policies of its members.

OACPS is now a more formal body. “We are an organisation because we have not only a permanent secretariat but we have a formal constitutive act, that is the Georgetown Agreement.”

The agreement that brought the ACP into existence was signed in 1975 in Guyana.

“So from being just a group of states, we are an international organisation — recognised. We already have observer status in the United Nations but we are not present on an ongoing basis. So our observer status now, as an international organisation, will be important for us to utilise that terminology… this organisation is linking members from three continents: Africa, the Caribbean, and the Pacific. So it is a more formalised way and we have elaborated, …, not only changing the names but also the objectives, the preamble, the structures.”

Another innovation is where the ACP had parliamentary assembly and a joint parliamentary assembly as a project out of funding with the European Union.

“But now we have put that as part of our organs. There will be an ACP parliamentary assembly.”

OACPS will institutionalise certain things to show it has been elevated to formal organisational structure with several functions. The reconstituted bloc will have increased visibility.

“We are, on certain periodic occasions, taking part in side events [of the United Nations]. We will have a greater say… as an organisation, using our observer status, to collaborate on an event on the programme; not a side event, but when the General Assembly or some other activity [that] is taking place. The Organisation of African, Caribbean and Pacific States will host, organise — in collaboration with member states — an activity in the UN or elsewhere.”

OACPS will work closely with other groups of nations that share common interests.

The summit has been historic. Among the five major outcomes is that, on intra-ACP cooperation, leaders have called for the establishment of an intra-ACP and trans-regional cooperation policy framework.

The outgoing secretary general said this will guide the group’s efforts towards strengthening ties and solidarity among the member states and regional organisations.

Leaders proposed a Nairobi Pledge for Urgent Climate Action that will canvass and circulate through the UN System.

“This will focus on our own sovereign agency that acts collectively across our 79 member states to address climate change and its consequences on the daily lives of several people.

On the blue economy, the summit agreed to an intra-ACP blue strategy under the leadership of Seychelles.

The first-ever women and youth forum and ACP Business Summit, held on the sidelines of the heads of government summit, led to ACP leaders calling for an ACP women and youth forum.

This will be a platform to support all ACP states in their efforts to engage women and youth.

The summit has noted the progress that Kenya made in promoting the interest of youth and women, in both legal and regulatory framework, and wishes to see it replicated in other countries.

The summit also called for the need to establish the business summit as a continued framework for the ACP heads of state and government to engage the business sector.

The bloc has a lot of potential.

“It has many ideas, and particularly at this time that we are at, the state of reforming the organisation to make sure that as we go into the 21st century, we are stronger in the reformed organisation, firm toward multilateralism, to make sure that we do compete better in the international arena…strong, beautiful and better”.

Panama Canal Challenges

PANAMA CITY – On Dec. 31, 1999, Panama took control of the canal built by the United States and run by that country since its inauguration in 1914. Its big challenge, overcome in the new period begun 20 years ago, was the expansion of the route through which 6 percent of the world’s trade passes, but now the water needed for its operation poses a new challenge.

“No sooner had we Panamanians received it that we realized that the future of the canal depended on the largest ships being able to sail through it,” said former President Aristides Royo, now canal affairs minister

“Seven years after the canal was handed over to us the enlargement works were begun. That, I would say, saved the canal” and helped make it “a good business,” said Royo, who served as president from 1978 to 1982.

In April 2006, the board of directors of the Panama Canal Authority (ACP) presented to Panama’s then-President Martin Torrijos, who was in office from 2004 to 2009, the proposal for the first and up to now the only expansion of the interoceanic waterway.

Two months later, in June 2006, the government approved it, and in October of that year it was ratified by popular vote.

Getting the canal’s enlargement started was not easy. Jorge Quijano was ACP administrator from 2012 until last September, when he passed the position on to Ricaurte Vasquez, former economy and finance minister and who had been the deputy administrator of the canal at the start of the 2000s.

“We were not like the United States, which could start a construction project for $5 billion or $6 billion without thinking twice. We had to go launder money abroad, with the only guarantee being the good work we had done” since the year 2000, said Quijano, an engineer with 40 years of ACP experience.

The expansion was “very complex – not even the Americans attempted it during their time. They started to try it in 1939 but had to stop because of World War II. They continued studies for a larger canal between 1966 and 1969, but aborted it in the midst of negotiating treaties,” Quijano recalled.

The negotiations that led to what are known as the Torrijos-Carter Treaties began to take shape after Panama rejected an accord reached in 1967 on three suggested pacts (The Panama Canal Treaty, The Treaty for the Defense of the Panama Canal and its Neutrality, and The Sea-Level Canal Treaty).

The Torrijos-Carter Treaties were signed in Washington on Sept. 7, 1977, and took effect on Oct. 1, 1979.

In September 2007 the expansion works began, whose main project, the new locks of Cocoli on the Pacific side and Agua Clara on the Atlantic, built by the GUPC consortium led by Spain’s Sacyr construction company and including Italy’s Impregilo, the Belgian Jan de Nul and the Panamanian CUSA company.

This new third lane, which allows the passing of New Panamax ships with triple the cargo capacity of the Panamax vessels that travel the original centenary route, was inaugurated on June 26, 2016, two years later than planned and amid economic demands by GUPC that are still being resolved in international courts.

-

- “In the first year of the Panamanian administration, in the year 2000, we invested $167 million. During the fiscal year that closed on Sept. 30 we invested $1.78 billion, almost 11 times mored. Climate change in the Panama Canal is very much in evidence” and affects the availability of water, the administrator Vasquez said last October, upon announcing that the option of desalination is being studied because it would mean “long-term sustainability and control” of the resource, indispensable for keeping the canal functioning.

The Panama Canal is fed by the Gatun and Alajuela artificial lakes, but their water also supplies the Panama City metropolitan area with its population of close to 1.5 million.

“We’ve been using water from Lake Gatun for 106 years and water from Lake Alajuela for another 84 years, and we’re straining them to the maximum.”

Royo said it was necessary this year “to reduce the tonnage” carried by ships on “three occasions,” because the canal was below the sufficient water level due to the lack of rain, which was some 27 percent below the historic average, according to ACP data.

Guyana to Chair G77

Demonstrating confidence in the Co-operative Republic of Guyana, the Group of 77 (G77) and China elected Guyana to serve as its Chair for 2020. At its 22 November plenary, the 134 Member States of the Group elected Guyana by acclamation without preconditions.

The election follows a decision of the Caribbean Community (CARICOM) earlier in 2019 to ensure that a regional candidate assumes chairmanship in 2020 of this largest negotiating group of developing countries in the United Nations. Consequently, for its accession, Guyana received the unequivocal support of CARICOM and the majority of countries in the Group, including from Africa, Asia Pacific and Latin America.

During its Chairmanship, which coincides with the United Nations seventy-fifth anniversary and its national Republic jubilee, the country is committed to endeavour to strengthen multilateralism for the benefit of all developing countries, including by presiding over global sustainable development and climate change negotiations, and efforts to improve the efficiency and effectiveness of the Organization.

Election as G77 Chair was hailed as a timely and fitting tribute with recognition of the good standing and capacity of Guyana to effectively undertake responsibilities at the highest levels of the international community.

The Minister of Foreign Affairs emphasized that “in keeping with its deep commitment to principled conduct and the rule of law, Guyana will discharge the important responsibilities of the Chairmanship of the G77 and China with integrity, faithfulness to the principles and objectives of the Charter of the United Nations.” The , country resolves to use the opportunity to further the interests of all developing countries.

The duties of the Chairman will be discharged with the support of a range of bilateral partners and international organizations. Team members will be drawn from the Ministry of Foreign Affairs, other Government Ministries and agencies and from the Guyanese diaspora.

Main activities of the Group take place at United Nations Headquarters in New York. G77 Chapters are based in Geneva, Nairobi, Paris, Rome and Vienna, and the closely allied Intergovernmental Group of Twenty-Four on International Monetary Affairs and Development (G24) in Washington DC.

The official ceremony for the handover of the G77 Chairmanship from the State of Palestine — which served in the capacity in 2019 — to the Co-operative Republic of Guyana will be held on 15 January at United Nations Headquarters in New York.

COLOMBIA

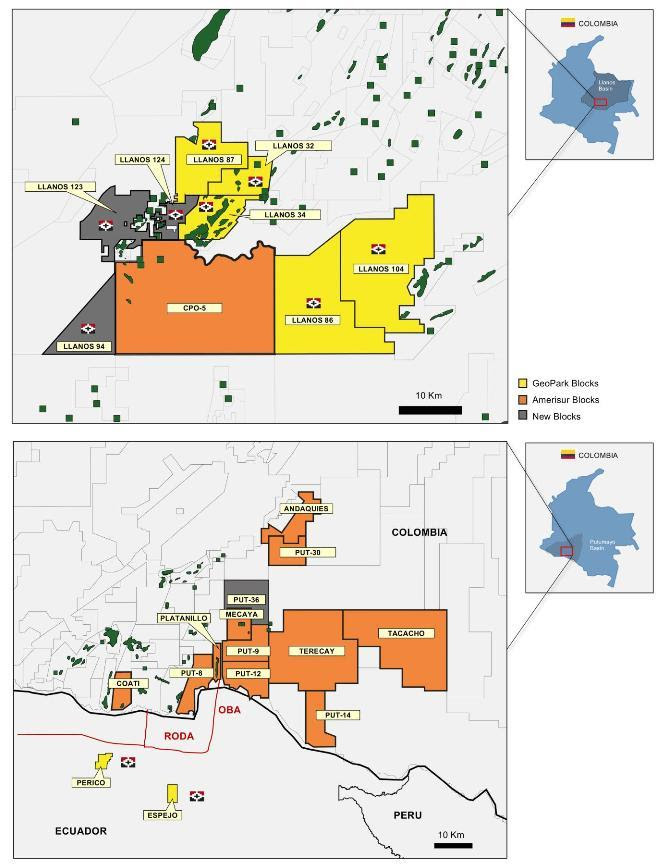

GEOPARK EXPANDS ACREAGE AROUND LLANOS 34 BLOCK

17 DEC 2019

GeoPark s announced expansion of its portfolio in Colombia following a new successful Agencia Nacional de Hidrocarburos (‘ANH’) bid round and an agreement with Parex Resources.

As part of the second cycle of ANH’s Permanent Process for the Assignment of Areas (‘PPAA’) in Colombia, GeoPark was awarded the Llanos 123 and Llanos 124 blocks in partnership with Hocol (a 100% subsidiary of Ecopetrol). Final contracts are expected to be signed in December 2019 or early 2020.

GeoPark and Parex executed an agreement in which GeoPark will assume, subject to ANH approval, a 50% WI in the Llanos 94 block in exchange for funding its 50% pro-rata share of existing commitments, with no carry.

On November 15, 2019, GeoPark announced that it will acquire the entire issued and to be issued share capital of Amerisur Resources in an all cash transaction with closing of the transaction expected in January 2020, following approval of Amerisur shareholders and subject to customary regulatory approvals. As part of the PPAA, Amerisur was awarded the PUT-36 block.

Llanos Basin

The acquired blocks represent attractive, low-risk, high potential exploration acreage in the Llanos basin near GeoPark’s successful Llanos 34 block (GeoPark operated, 45% WI), and surrounded by multiple producing oil and gas fields and existing infrastructure (see map below).

The Llanos 123 and Llanos 124 blocks are located adjacent to GeoPark’s Llanos 34 block. GeoPark will be the operator with a 50% WI and Hocol (a 100% subsidiary of Ecopetrol) will have a 50% WI.

The Llanos 94 block is located on trend with GeoPark’s Llanos 34 block and adjacent to the CPO-5 block (ONGC Videsh operated, 70% WI, Amerisur 30% WI).

GeoPark and its partners have preliminarily identified multiple oil prospects and leads in these blocks, resulting from existing 3D seismic as well as other relevant data. Geoscience evaluation is ongoing and field operations are expected to start in 2020.

With the addition of new blocks during 2019 and following the closing of the recently announced acquisition of Amerisur, GeoPark will significantly expand its acreage position around its core Llanos 34 block by adding approx. 1.4 million gross acres – 17 times the size of the Llanos 34 block.

The table below summarizes relevant information related to the new blocks acquired in the Llanos basin:

(1) Commitment includes reprocessing existing 3D seismic and drilling two gross exploration wells during the first exploration phase over the next three years.

(2) Commitment includes acquiring and reprocessing existing 3D seismic plus drilling three gross exploration wells during the first exploration phase over the next three years.

(3) Commitment includes acquiring and reprocessing existing 3D seismic plus drilling three exploration wells during the first exploration phase over the next three years.

Putumayo Basin

The PUT-36 block represents attractive exploration acreage in the Putumayo basin adjacent to Amerisur’s Mecaya block (Amerisur operated, 50% WI and Oxy 50% WI) and PUT-9 block (Amerisur operated, 50% WI and Oxy 50% WI) and near the producing Platanillo block (Amerisur operated, 100% WI), as well as other exploration acreage held by Amerisur (see map below).

With the addition of this new block and following the closing of the recently announced acquisition of Amerisur, GeoPark will further expand its position of more than two million gross acres in the Putumayo basin, with existing production, a nearby dedicated cost-effective transportation solution with spare capacity and significant exploration potential.

(1) Commitment includes reprocessing existing 3D seismic and drilling two gross exploration wells during the first exploration phase over the next three years.

(1) Commitment includes reprocessing existing 3D seismic and drilling two gross exploration wells during the first exploration phase over the next three years.James F. Park, CEO of GeoPark, said:

‘Congratulations and thanks to our partners, Hocol (a 100% subsidiary of Ecopetrol) and Parex, and to our Colombian team for successfully acquiring these highly attractive, low-cost blocks – which further strengthen GeoPark’s leading acreage position in the Llanos basin – specifically surrounding our prolific Llanos 34 block. Subject to the closing of the Amerisur acquisition, the new Putumayo block helps leapfrog GeoPark into one of the leading land holdings in the high potential underexplored and underdeveloped Putumayo basin. We also express our appreciation to the Colombian government for its commitment to and follow-through in opening up more attractive hydrocarbon areas for investment – and we look forward to getting to work.’

Source: GeoPark

COLOMBIA

HOUSTON AMERICAN ENERGY DOUBLES PARTICIPATION IN HUPECOL META,

Houston American Energy announced the acquisition of an additional interest in Hupecol Meta, doubling its interest in Hupecol Meta previously announced on October 22, 2019. Hupecol Meta owns the 639,405 gross acre CPO-11 block in the Llanos Basin in Colombia, comprised of the 69,128 acre Venus Exploration area, operated by Hupecol, and 570,277 acres which was 50% farmed out to Parex Resources by Hupecol. In total, the CPO-11 block covers almost 1000 sq miles with multiple identified leads and prospects expected to support a multi-well drilling program. Through its membership interest in Hupecol Meta, Houston American now holds a 2% interest in the Venus Exploration area and a 1% interest in the remainder of the block.

The increased participation in CPO-11 complements Houston American Energy’s recent efforts to expand its acreage position which, over the last year, has resulted in the acquisition of positions in two blocks in the Midland sub-basin of the Permian Basin totaling approx. 6,500 gross acres plus the 639,000+ gross acre CPO-11 block. The company expects those acquisitions to provide a multi-year inventory of drilling prospects with the potential return to growth in production, proved reserves, revenues and a potential return to profitability.

Jim Schoonover, CEO of Houston American Energy, stated:

‘We are in the midst of a three phase plan designed to return Houston American to sustainable revenue growth, profitability and growth in shareholder value. Phase One, focused on reducing our overhead, has resulted in a substantial decrease in our general and administrative expenses since 2017. Phase Two, focused on identifying and committing to projects that offer both scale and revenue potential necessary to regain sustained profitability, has resulted in recent acquisitions of positions in acreage covering more than 645,000 gross acres, including two San Andres projects in the Midland sub-basin of the Permian Basin plus the CPO-11 block in Colombia. Having executed on Phases One and Two, we are now focused on Phase Three, executing on the development of these newly acquired assets, while continuing to identify new opportunities.’

Surce Houston American Energy

Canacol Energy wins three exploration blocks

12/9/2019

CALGARY – Canacol Energy successfully secured a 100% operated working interest in three new conventional gas exploration contracts in the recent bid round administered by hydrocarbon regulatory authority, the Agencia Nacional de Hidrocarburos.

Mark Teare, senior vice president, exploration, commented “Our success in the bid round enables us to build out our existing land position in the Lower Magdalena Valley basin where the Corporation has established itself as Colombia’s leading independent producer of conventional natural gas. Furthermore, with a view to expanding our exploration portfolio, we have established a new core conventional natural gas exploration area in the Middle Magdalena Valley basin where we have won two blocks totalling 160,666 net acres. We expect to initiate exploratory activity on our new blocks in 2020 with a view to drilling in 2021 and 2022.”

“By extending our exploration efforts for conventional natural gas to the Middle Magdalena Valley basin, the corporation continues to execute its successful conventional gas exploration strategy to replace declining production from the mature gas fields located in the Guajira and at Cusiana-Cupiagua in the Llanos basin.”

Under its wholly owned subsidiary CNE Oil & Gas S.A.S., Canacol was awarded conventional exploration contract VIM 33 (155,310 acres, 62,852 hectares) in the Lower Magdalena Valley basin, and conventional exploration contracts VMM 45 (12,422 acres, 5,027 hectares) and VMM 49 (148,244 acres, 59,992 hectares) in the Middle Magdalena Valley basin. On a net acreage basis, these conventional exploration contracts increase the corporation’s land position for conventional natural gas in Colombia by 29 % from 1.1 mm net acres to 1.4 mm net acres.

The winning bids commit the corporation to an exploratory work program including geological studies, seismic and wells over a three-year phase (Phase 1) on each of the exploration contracts. Once Phase 1 is complete, the corporation has the option to extend the exploratory work program by an additional three years (Phase 2) on each of the exploration contracts.

Parex among winners in bid round

BOGOTA, Dec 5 (Reuters) – Companies including Canada’s Parex Resources and Ecopetrol SA won contracts to operate oil blocks in Colombia’s auction round on , as the Andean producer seeks to reinvigorate its petroleum sector.

Ecopetrol and its subsidiary Hocol SA, Frontera Energy Corp and Amerisur Resources Plc were all awarded one contract each, the national hydrocarbons agency (ANH) said, after their initial bids did not receive counter-offers.

Other successful bidders included Gran Tierra Energy and Parex, which were awarded two contracts each, while CNE Oil and Gas SAS was awarded three contracts.

A consortium of Ecopetrol and Parex was awarded one contract, as was a consortium of Hocol and Geopark LLA.

Block SN 26 was awarded to a consortium of La Luna and Captiva, whose bid beat a rival submission from Hocol.

Just one counter-offer was received for block Llanos 124 by Parex. In earlier bidding, the block received bids from Parex and a consortium of Geopark and Hocol. Last year Colombia’s crude reserves rose 9.9% to 1.96 billion barrels, equivalent to 6.2 years of output. The government wants to increase reserves to at least 10 years equivalent.

Average oil production is about 860,000 barrels per day, half of which is exported.

“Six years of oil reserves and less than 10 years of gas reserves is very low for Colombia,” Luis Miguel Morelli, head of the ANH, said. However, after securing some 31 contracts this year, Morelli said he expects 2020 “to bring a radical change” to the country’s oil sector.

Previously, the ANH had hoped to generate investment of around $800 million in this auction, the second this year, from a targeted 20 bids.

However, just 10 companies placed 17 bids in the first round of the auction for just 15 of the 59 blocks available in November, which the ANH said it expected to draw more than $500 million in investment.

The first auction in June awarded 11 oil contracts to six companies, which the ANH expects to generate some $500 million in investment.

Earlier this year, companies including Royal Dutch Shell Plc , Noble Group Ltd, Exxon Mobil Corp, Repsol SA and Parex signed on to operate new blocks. The ANH said investment from the contracts awarded in 2019 have a current value of $2.71 billion, although this could rise, depending on the outcome of today’s one counter offer.

Reporting by Oliver Griffin Editing by Daniel Flynn and Chris Reese)

Ecopetrol completes offshore seismic shoot

COL-5 block lies adjacent to Kronos, Gorgon gas discoveries

By Julia Martinez

SOC Ecopetrol has wrapped up its first deep-water 3D seismic shoot in the offshore COL-5 block. The 2000-square kilometre shoot took about two months.

Latin America to attract upstream investment

Latin America will have its day in the sun and is well-placed to shrug off any transition headwinds.

The best upstream oil and gas opportunities will attract investment over the coming decade, despite headline-grabbing messaging around the energy transition. A flurry of business development activity in recent years which have seen the industry’s largest E&P firms rapidly build exposure to some of the best resource opportunities around, from the Brazilian pre-salt to Argentina’s unconventionals, reinforce that Latin America will remain an attractive destination for investment While political risk in the region is, admittedly, never far from the surface, the industry’s appetite for what the region has to offer is clear