Dragon dance

After meeting Venezuelan officials in Caracas Energy Minister Stuart Young expressed confidence that Trinidad and Tobago would successfully conclude and execute a deal to receive gas from Venezuela’s Dragon Field, but his update lacked details owing to ongoing negotiations.

Challenges before first gas are not to be underestimated. The two-year waiver by the US Treasury Department is a tiny window in the timelines of petroleum extraction and the limitations on payment to Venezuela are an additional constraint.

In this file photo, Energy Minister Stuart Young greets Venezuelan President Nicolas Maduro in Caracas in June 2022. –

The deal relaxes severe sanctions the US placed on Venezuela and the terms may offer an opportunity for TT, which exists to serve the needs of the US amid energy constraints from the invasion of Ukraine.

It is unclear how long Russia will wage war, how long Ukraine will resist and what the US plans for relaxation of sanctions would be in the complex circumstances likely to exist at the end of the licence by the Treasury Department’s Office of Foreign Assets Control (OFAC).

A PDVSA resource discovered in 1985, the giant Dragon field, comprises an estimated 4.2 trillion cubic feet of natural gas reserves, idled under US sanctions, that borders mature but active Hibiscus field off north-western Trinidad.

In 2018, TT negotiated for access to the field, which has the potential to deliver significant supply to Trinidad’s under-utilised LNG production facilities when tighter US sanctions scuttled talks.

Leading the development of the project, gas pioneer Shell operates Hibiscus and has a long and frustrating history of trying to exploit the field for decades since the Mariscal Sucre project.

The US cleverly positioned the deal as a step forward for energy security for the Caribbean Basin, targeting Jamaica, paternal homeland of the US VP. Estimated yield from Dragon is 150-350 million cubic feet of gas per day, a production capacity that will surge past regional needs to northern markets.

TT requested a ten-year guarantee of access to the field but the US insists that it must continue to act the OFAC way, having overturned severe policy decisions regarding Venezuela in its own interests. TT must also protect its interests to avoid being stranded .

Venezuela is largely silent about the OFAC deal, perhaps mulling the real-world value of the hardline restriction on cash payments and what it means for value revenue as payment for its natural resource.

President Nicolas Maduro dismissed the limitation as modern-day colonialism but the troubled country cannot afford to ignore the lifeline.

Shell gas pipeline from Venezuela to Trinidad

Shell 17 Km gas pipeline from gas field Dragon to gas field Hibiscus

(NB Date)…Petroleum world 03 17 2017

Shell 17 Km gas pipeline from gas field Dragon to gas field Hibiscus

Oil and gas giant Royal Dutch Shell is expected to build a 17 kilometre (10.6 mile) pipeline from Venezuela’s shallow-water Dragon gas field to its Hibiscus platform off the north coast of Trinidad, following agreements signed Wednesday in Caracas, according to Venezuelan government statements.

Minister in the Office of the Prime Minister Stuart Young is expected to make the announcement today at the weekly post-Cabinet press briefing in Port of Spain.

On Wednesday in Parliament, he said he “just came off a plane” and would make an announcement within 24 to 48 hours on what Government is doing to help the declining oil and gas sector.

Hours before, he was excused from the Lower House sitting by Speaker Bridgid Annisette-George who said he was out of the country.

At a press conference in Caracas yesterday, Young said he wanted “to also welcome to the table, Shell, who have shown themselves to be a willing partner with both the Government of Venezuela as well as the Government of Trinidad and Tobago, and to emphasise and to concur with my fellow minister, his excellency (Venezuela’s Oil) Minister (Nelson) Martinez in telling Shell that we want to contract and crunch the time frame and to make this happen as quickly as possible and you have the full support of both Governments and our respective teams to make this a reality.”

Venezuela’s State-owned oil and gas company Petroleos de Venezuela (PdV) President Eulogio del Pino said at the press conference: “We’ve signed an agreement to supply gas to Trinidad through the National Gas Company of T&T (NGC) and Shell, and also to build a gas pipeline between Venezuela and Trinidad.”

US$100m investment

NGC Chairman Gerry Brooks signed on behalf of NGC while del Pino signed on behalf of PdV and Port of Spain-based Luis Prado, on behalf of Shell. NGC President Mark Loquan was also on the one-day trip to La Campina, Caracas. Young signed on behalf of the Government of T&T while Martinez signed on behalf of the Government of Venezuela. The agreements were not shared with the media. However, Young was quoted in one of the Venezuelan Government’s statements as saying the development of the project could entail an investment of more than US$100 million.

The agreements cover “the construction, operation and maintenance of a gas pipeline from Dragon field, located in the north-east of the Paria Peninsula, Sucre State, to Trinidad’s Hibiscus platform,” a Venezuelan Government statement said.

“After this pipeline is completed, natural gas will be supplied to the Trinidadian domestic market and to a gas plant on the island, from where it is expected to be sold to the international market,” the Bolivarian Government said.

“The initial idea is to start producing for Trinidad and Tobago, between two to three years, some 200 or 300 million (standard) cubic feet of gas (per day),” (mmscfd) Martinez said at the press conference at PdV headquarters in Caracas. Martinez said the gas to be exported to T&T “has the potential to be transformed into liquefied natural gas (LNG) or any kind of raw material,” suggesting both Atlantic, majority-owned by Shell, and Point Lisas could benefit.

Enough to supply T&T plus export

“The Dragon field is the closest to Trinidad and has a very interesting perspective, since it can generate gas for the domestic market and for export. Gas exports are of particular interest,” Martinez said. He said Venezuela has the gas potential – around 197.1 trillion cubic feet (tcf) of proven natural gas reserves – to fully satisfy T&T’s domestic market and still have leftover to export.

From Wednesday, a team of experts from Shell, PdV and the NGC will work together to define the operational, commercial and legal parameters that will govern the project, Martinez said.

“We already have the infrastructure on the Trinidad side and we have the willingness to accept this challenge. The benefit for the two countries is very clear,” he said.

The Dragon field is one of the four fields that make up the 14.7 tcf Mariscal Sucre Project (MSP) to the north of the Paria Peninsula, which aims to produce in the long term, 1.2 billion cubic feet (bcf) of gas and up to 28 thousand barrels of oil per day. Other fields in the MSP are the Patao, Mejillones and Rio Caribe fields.

After the signing, Young paid a courtesy call on Venezuelan Foreign Affairs Minister Delcy Rodriguez, and then flew to Piarco, whence, according to Opposition Leader Kamla Persad-Bissessar, he was whisked with “flashing blue lights” to Parliament to contribute to a bill to make borrowing from the Corporacion Andina de Fomento (CAF) legal.

Rowley: Dragon at ‘Business Plan’ stage

On March 6, Opposition Member of Parliament for Caroni Central Dr Bhoendradatt Tewarie asked: “Would the prime minister provide an update on the status of negotiations with Venezuelan authorities regarding the Dragon Field Project and advise this House on his assessment of progress made up to this point?”

Prime Minister Dr Keith Rowley responded: “Madam Speaker, as you know, these are very delicate negotiations, except to say that we have made some progress. We are at the stage of finalizing the kinds of documents that would put us on a path to move from concept to business plan, but I do not want, at this stage, to publicly discuss where we are at, given that these are very delicate and sensitive negotiations.”

An improved gas-reservoir delineation from seismic-derived impedance and density interpretation at Dragon field, Venezuela

Authors:César Vasquez and Wilmer Ochoa

https://doi.org/10.1190/tle33070764.1

Abstract

Dragon field of Norte de Paria, offshore eastern Venezuela, was discovered in the 1980s and offers a good opportunity for production of gas methane. Since 2008, several development wells have been drilled for production of gas reserves. After analysis of exploratory well E1 and development well D1, gas was found in the former and water in the latter. A recent study showed that analysis and interpretation of seismic amplitudes can differentiate fluids that saturate rocks and thus can optimize the production of hydrocarbons. Seismic amplitudes show significant differences in the same stratigraphic level, depending on the presence of different fluids — brine, gas, or a mixture of the two. Differences are associated with density and compressibility of fluid under the pressure and temperature conditions of the reservoir. After computing Poisson’s ratio and acoustic impedance from analyzed wells, it was observed that those values were lower at the gas-bearing sands than for the encasing rock. Based on that result, an acoustic-inversion exercise was performed over the existing seismic data to interpret lateral heterogeneities associated with gas saturation. However, the well-known effect of low gas saturation on seismic velocities introduces an appreciable uncertainty in interpretation. To overcome this issue, it is proposed to estimate densities from an elastic inversion of the seismic data and to interpret fluid distribution in the reservoirs at Dragon field using this attribute.

Shell

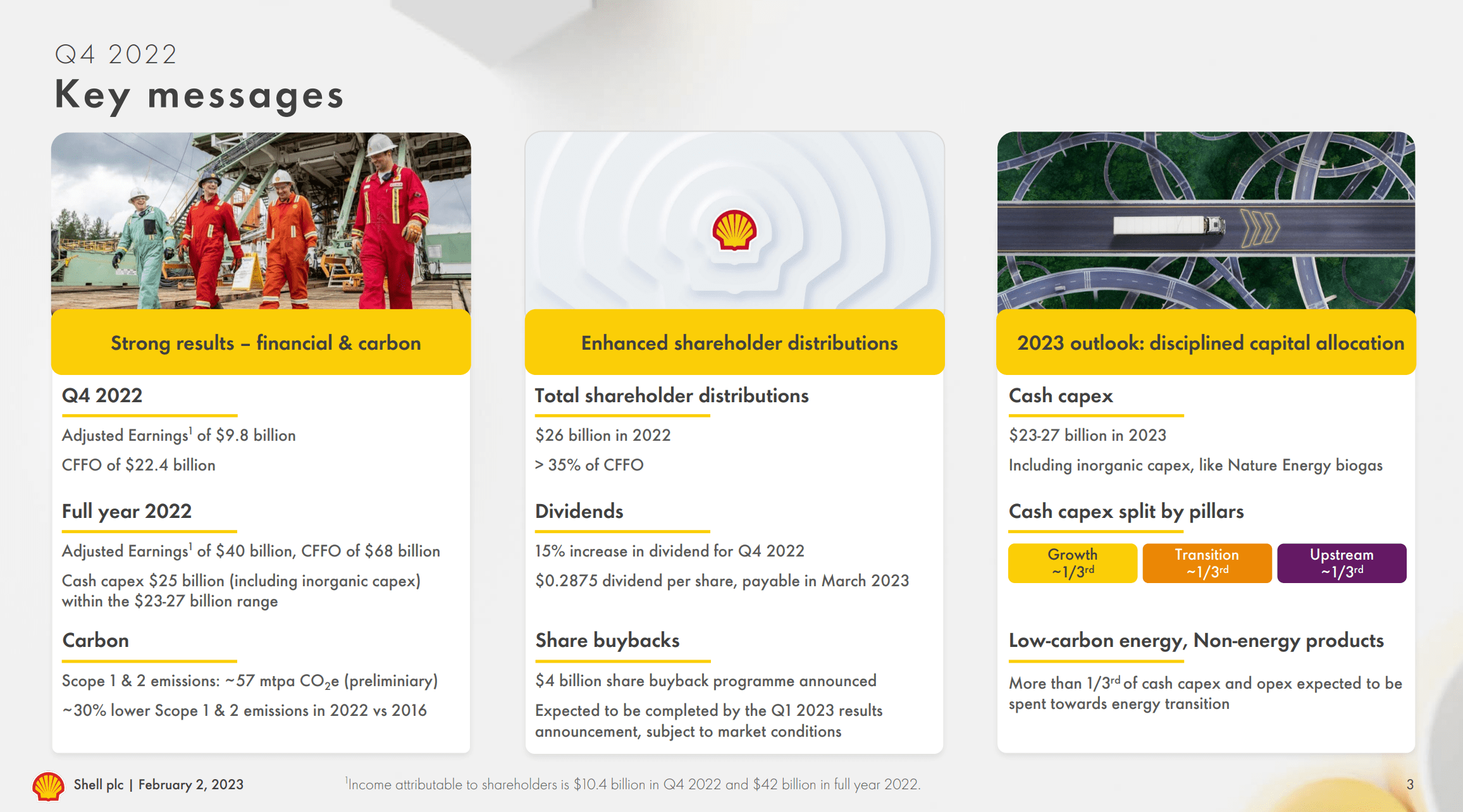

Nearly 115-year-old British energy giant Shell reported its highest annual profit ever—nearly $40 billion in 2022, after record announcements from American heavyweights Chevron and Exxon Mobil as the industry capitalizes on energy prices and market upheaval caused by Russia’s invasion of Ukraine.

Shell announces fourth quarter 2022 results

02 Feb 2023

Shell released its fourth quarter results and fourth quarter interim dividend announcement for 2022.

Chief Executive Officer, Wael Sawan, said:

‘Our results in Q4 and across the full year demonstrate the strength of Shell’s differentiated portfolio, as well as our capacity to deliver vital energy to our customers in a volatile world.

We believe that Shell is well positioned to be the trusted partner through the energy transition. As we continue to put our Powering Progress strategy into action, we will build on our core strengths, further simplify the organisation and focus on performance. We intend to remain disciplined while delivering compelling shareholder returns, as demonstrated by the 15% dividend increase and the $4 billion share buyback programme announced today.’

STRONG RESULTS, DISCIPLINED CAPITAL ALLOCATION

-

-

- Strong performance in a continuing uncertain economic environment. Q4 2022 Adjusted Earnings of $9.8 billion, with Adjusted EBITDA of $20.6 billion, despite lower oil and gas prices compared with Q3 2022, with higher LNG trading and optimisation results.

- 15% dividend per share increase for the fourth quarter. $4 billion share buybacks announced, expected to be completed by Q1 2023 results announcement.

- 2022 full year shareholder distributions $26 billion. Total distributions in excess of 35% of CFFO for 2022.

- Strengthening the portfolio with the announced acquisition of Nature Energy (Denmark), a renewable natural gas producer, winning the wind tender for Hollandse Kust (west) VI as part of the Ecowende joint venture and further simplifying the portfolio with the merger of Shell Midstream Partners (USA).

- 2023 cash capex outlook: $23 – 27 billion.

-

(1) Income/(loss) attributable to shareholders for Q4 2022 is $10.4 billion. Reconciliation of non-GAAP measures can be found in the unaudited results, available on www.shell.com/investors.

Source: Shell

Shell sets record as profits more than double to $40bn

Shell hit a new all-time earnings high after the supermajor more than doubled year-on-year profits.

Shell PLC (SHEL) Q4 2022 Earnings Call Transcript

Feb. 02, 2023

Q4: 2023-02-02 Earnings Summary

EPS of $2.60 beats by $0.29 | Revenue of $101.30B (18.79% Y/Y) beats by $59.98B

Shell PLC (NYSE:SHEL) Q4 2022 Earnings Conference Call February 2, 2023

-

-

- Company Participants

- Wael Sawan – CEO & Director

- Sinead Gorman – CFO & Director

- Conference Call Participants

- Oswald Clint – Sanford C. Bernstein & Co.

- Biraj Borkhataria – RBC Capital Markets

- Christopher Kuplent – Bank of America Merrill Lynch

- Amy Wong – Crédit Suisse

- Irene Himona – Societe Generale

- Lucas Herrmann – BNP Paribas Exane

- Henri Patricot – UBS

- Peter Low – Redburn

- Alastair Syme – Citigroup

- Lydia Rainforth – Barclays Bank

- Giacomo Romeo – Jefferies

- Michele Vigna – Goldman Sachs Group

- Jason Gabelman – Cowen and Company

- Christyan Malek – JPMorgan Chase & Co.

- Paul Cheng – Scotiabank

-

Operator

Welcome to Shell’s Fourth Quarter 2022 Financial Results Announcement. Shell’s CEO, Wael Sawan; and CFO, Sinead Gorman, will present the results, then host a Q&A session. [Operator Instructions]. We will now begin the presentation.

Wael Sawan

Hi. I’m Wael Sawan, and I’m pleased to present to you for the first time as Shell’s CEO. Today, alongside Sinead, we’ll be presenting Shell’s fourth quarter and full year results. I’d like to start by thanking Ben for his leadership over the last 9 years and for building the strong foundations that I now inherit. We have a world-class organization with exceptional people, a leading portfolio and the right strategy, all of which, I believe, position us very well for the future.

2022 was a year in which energy security was front and center. The world mobilized. We saw policy progress with Fit for 55 in Europe and the introduction of the Inflation Reduction Act in the U.S. This is evidence of moving from ambition into action. Despite this progress, the energy system still faces huge challenges, and it continues to need bold, decisive actions by companies, governments and society at large. The world requires a secure supply of affordable energy and, at the same time, needs this energy to be increasingly low carbon to make the transition to a net-zero emissions energy system.

In short, the world needs a balanced energy transition. Moving too fast by dismantling the current energy system before the new system is ready could worsen the situation. But moving too slowly could waste precious time and lose the momentum to build necessary solutions for low-carbon energy at scale. However, this transition will not be linear and will play out with different solutions needed at different times in different places across the world.

We at Shell will do our part. We will invest with discipline where we have differentiated capabilities. We aim to deliver the oil and gas that the world sorely needs today while also leveraging our unparalleled customer reach to develop the scalable and profitable low-carbon products that are urgently needed. Shell, under my leadership, will work to be the trusted partner of choice as the world’s energy systems transition for our customers, governments and investors. By doing so, we aim to deliver competitive returns and create significant shareholder value over the coming years.

Now let’s look at our Q4 and full year results and financial framework. And for that, let me hand over to Sinead.

Sinead Gorman

Thank you, Wael. By continuing to provide the energy our customers need, we have again produced strong results. Our safety performance was impressive. We made good progress in both personal and process safety year-on-year. We also made good progress on carbon. By the end of 2022, we were more than halfway towards achieving our target reduction of 50% by 2030 for Scope 1 and 2 emissions.

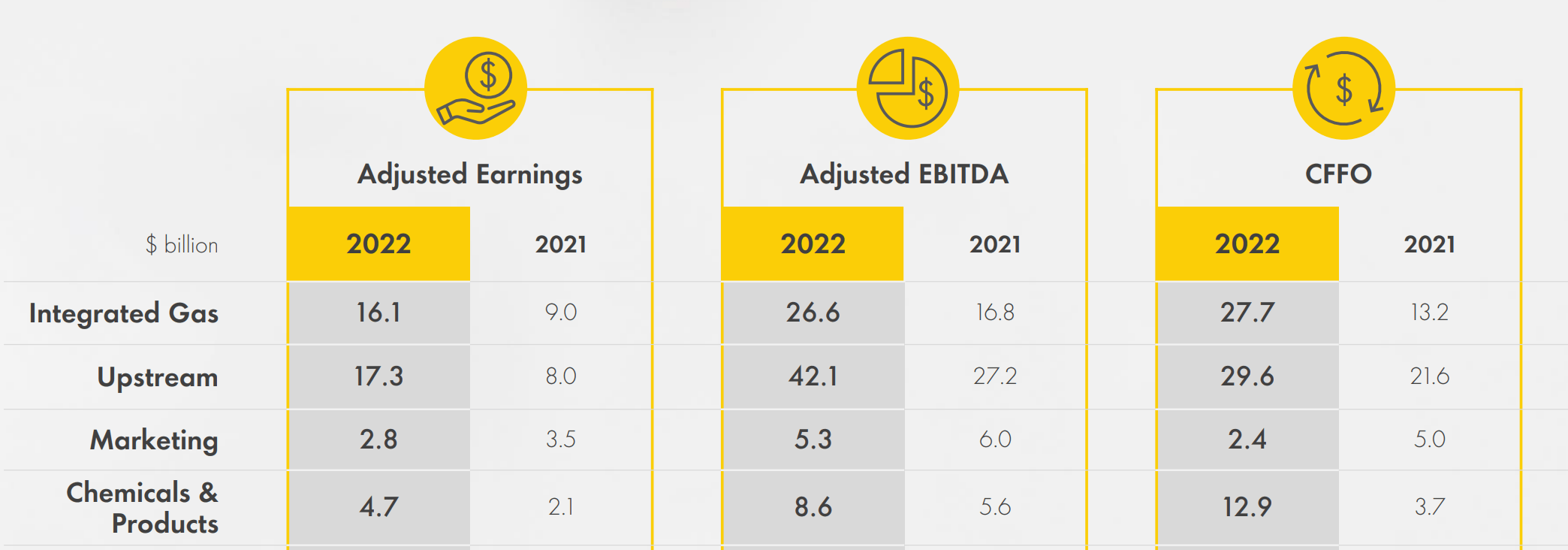

Moving to our financial performance. Our adjusted earnings for the fourth quarter were $9.8 billion, with strong contributions from our Integrated Gas business, and we generated $22.4 billion of cash flow from operations, including a positive inflow of $10.4 billion of working capital.

These strong quarterly results helped us to achieve our highest ever full year results, with adjusted earnings of some $40 billion, more than double those of last year and around $17 billion higher than in 2014 when Brent prices were similar. We delivered a full year cash flow from operations of over $68 billion. And our organic free cash flow was around $48 billion.

In 2022, our financials were impacted by additional taxes of around $2.3 billion. Of this, around $1.5 billion related to the EU solidarity contributions in the Netherlands, Germany and Italy, with cash outflows expected in 2023 and 2024. For the U.K. Energy Profits Levy, they impact us some $900 million.

And now on to our financial framework. Our strong performance over the year has allowed us to enhance our distributions to shareholders. Our total shareholder distributions for the year were around $26 billion in excess of 35% of our 2022 cash flow from operations. And today, we have announced a new $4 billion share buyback program, which we expect to complete on time of our Q1 results announcement. As planned, we have also increased our dividend per share by 15% in the fourth quarter.

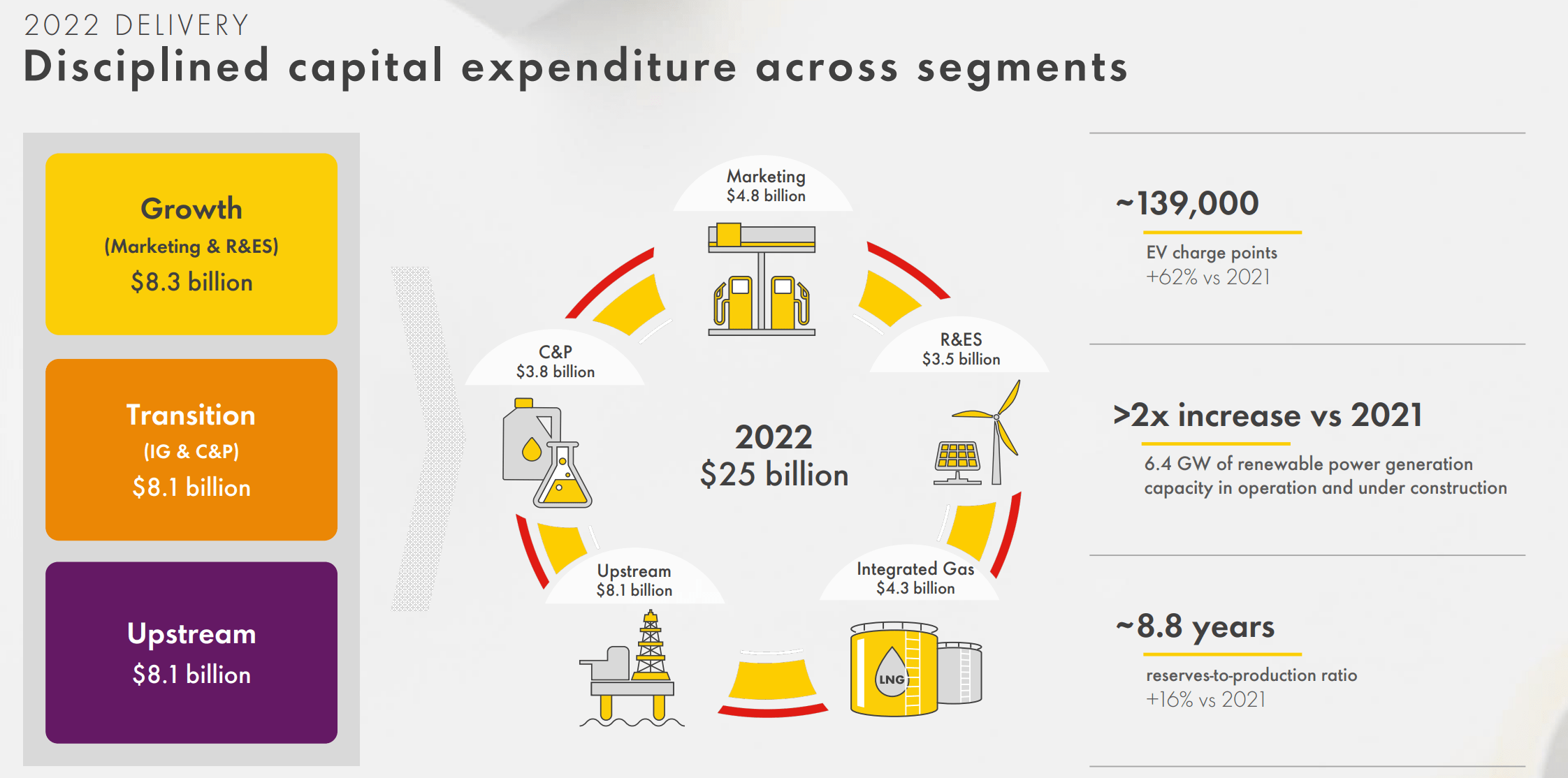

Demonstrating discipline, our total cash capital expenditure for 2022 was $25 billion. And our outlook for 2023 is to maintain the $23 billion to $27 billion range, absorbing inflation. Our AA credit metrics ambition remains. We intend to continue to reduce our net debt as part of our robust financial framework. Finally, we will continue to target shareholder distributions of at least 20% to 30% of our cash flow from operations.

And now I’ll hand back to Wael.

Wael Sawan

As you’ve heard, our results for 2022 were strong in what was a volatile external environment. So what do we expect to see for 2023? The balance between global energy supply and demand remains extremely tight. Small changes on either side can have a significant impact. So volatility and uncertainty will continue to be the watch words in 2023. And how will Shell respond to that? With confidence in the direction of our strategy and the strength of our businesses and with discipline and a focus on value. We’ve worked hard over the years to strengthen our portfolio. We have a clear strategy empowering progress. Our focus now is to further operationalize and profitably deliver this strategy. We will build from our strengths, where we will prioritize value over volume while reducing carbon emissions.

In Upstream, we will continue to proudly deliver energy that the world needs while driving strong results with our high-graded portfolio. In Integrated Gas, we will leverage and extend our world-leading LNG position. And in Marketing, we will build on the robust performance that we have seen in recent years.

Performance will be top of mind. In every area of show, we aim to demonstrate progress at pace, not through words but through results, and we will continue to simplify our organization. One example of this is the more aligned and focused senior leadership structure that we announced earlier this week, with fewer rules and greater accountabilities, simplifying decision-making. By building on our strengths, focusing on performance and simplification, we intend to deliver compelling shareholder returns. Shell is already a great company, and we are determined to be a great investment. And to give you more insights on how we plan to do this, join us in New York for our Capital Markets Day in June. Thank you.

Question-and-Answer Session

Operator

A – Wael Sawan

Thank you for joining us today. We hope that after watching the presentation, you’ve seen how we delivered strong results and how we intend to further operationalize our Powering Progress strategy. Today, Sinead and I will be answering your questions. And now please, could we have just 1 or 2 questions each, so everyone has the opportunity. And with that, could we have the first one, please, Dan?

Operator

The first question is from Oswald Clint at Bernstein.

Oswald Clint

Thank you very much, and good afternoon to both of you, and welcome, Wael, to the Q&A interrogation. First one on capital investment, please. Spend levels looking into the year in line with your guidance. That’s good. I think Sinead mentioned the guide is also absorbing inflation. So I was curious just how much and where you’re experiencing those hot spots at the moment. It doesn’t imply any activity has to be phased or pushed back. And I see within CapEx, Marketing steps up a bit this year. I assume that’s Nature Energy. But I’m just looking at Marketing, wondering that the earnings there are still a little bit below trend. And does Asia reopening here really start to help the earnings trend within that Marketing business? That was the first question.

Secondly, I’d love to ask about Integrated Gas. Wael, you mentioned volatility, uncertainty, your watch words for this year. We obviously had one hiccup last year around this business around hedging. So curious to know what the lessons learned were from 2022 and what’s the hedging strategy for this year, if there’s any changes needed in that approach.

Wael Sawan

Super. Oswald, thank you for that, and I appreciate being here for the interrogation. I guess I’ll get used to it. Let me start by maybe giving you, Sinead, the floor on the Marketing question and maybe also the Integrated Gas learnings. I can reflect a bit on inflation in a moment.

Sinead Gorman

Certainly. So indeed, thank you for that, Oswald. So in terms of Marketing, so taking a step back for the moment. So 46 sites and regional sites, #1 in lubes, if anyone can make substantial returns out of this, it is us. We are well positioned for it. In saying that, I agree. $400 million of earnings for this quarter was a little bit disappointing. But if you take a step back and look at why.

So what we’re very comfortable with is seeing the fact that COVID has really not completely played out. So we’re still seeing the impact of that. And you’re right, you point out China as well. So we have great expectations with China opening up to be able to see that advance, and we’ve got green shoots already. And particularly in our lubes business, of course, we have a bit of a parachute effect. The normal where the high cost of the inputs, it takes a while for that to be passed through as well. So those combinations, including with our differentiated offerings, we’re pretty confident in terms of how you will start to see some of our marketing results begin to improve.

The second one was in relation to IG and the volatility around it. I’m just going to take a bit of an opportunity also to take that stuff back. We talked before about the fact that for IG, you really need — or Integrated Gas, you need to look at it over a series of quarters, not one specific quarter. We use price risk management. Our hedging is price risk management, and we use it to look at the exposures we have across the period, not specifically quarter by quarter by quarter. Of course, that does mean that you see different things play out.

You do see correlations becoming more or less effective. This quarter, you saw them being very effective because we didn’t see those dislocations between the EU and, in fact, JKM, et cetera. But those breakdowns are typically temporary, and that’s what you saw as it came through. So this quarter, hedging acting very much as intended, and that’s what we like.

Wael Sawan

Thanks for that, Sinead. And Oswald to your first question, just to play back. So the $23 billion to $27 billion includes a few things. One, we have said is it will include Nature Energy, which you know is to the tune of around $2 billion. Secondly, we’ve also said it includes general inorganics. So that’s also within that number. And then thirdly, indeed, there is inflationary pressure that we’re absorbing. The inflationary pressure we’re seeing at the moment is in the range of, say, 10% to 12%, typically. Of that, we’re being able to mitigate a decent portion of that but not all of it. Most of the mitigations come from long-term contracts with suppliers where we have these enterprise framework agreements that we can lean on because of the scale of our purchases with those suppliers. So that allows us to mitigate some of the exposure.

You talked about delaying projects and the like. There are examples of that, of course. We took the decision on Gato do Mato, which is our Brazilian offshore opportunity, to recycle that project because of the cost estimates that came in were higher than we were comfortable taking a final investment decision on. And so with a disciplined focus on our capital allocation, we said this is not the right time to do it. And therefore, we punt it until there is a better environment to be able to invest in. So hopefully, that just gives you a bit of a flavor of how our thinking has gone with that.

Oswald, thanks for the question.

Operator

The second question is from Biraj Borkhataria at RBC Capital Markets.

Biraj Borkhataria

I’ve got 2, please. The first one is a few days ago, there were some headlines around you looking to review your U.K. electricity business. I was just wondering, I know this is not a huge part of the portfolio, but is this part of a broader review of your low-carbon efforts? Or is it specific to this business? Because I guess if I look from the outside in, this is a fairly low-margin business that actually has needed quite a lot of capital given all the volatility in power prices. So just wanted to get a sense of what has triggered that review there.

And the second question is in the Upstream. So in 2020, 2021, you put out your emissions targets and all the targets related to the energy transition. And one of those was declining oil production, 1% to 2% per annum. If I look at the last 2 years, it’s down something like 10% to 12%. So clearly, you’ve moved a lot faster on some divestments and so on, and that’s been a part of that. So given you’re well ahead of where you intended to be on that front, what does this mean for Upstream volumes going forward? Should we expect more stable production now or even growth? Because I guess the realities of the energy market are very different to when you put those targets out there as well. So just some thoughts on that.

Wael Sawan

Super. Thank you for that, Biraj. I’ll take both of those and start off with the SERL one, so Shell Energy Retail. The broad — the review of SERL is specific to SERL. It’s not a broader review of low-carbon investments. Ultimately, we are looking at every single one of our investments in its own right and trying to understand whether we can totally unlock the value out of that investment opportunity.

For Shell Energy Retail, what we have found is despite a few years of trying to make that work as part of an integrated value chain, the market conditions are just structurally not there for us to be able to create the returns we expect. We have seen significant interventions from the government, including price caps, including windfall taxes. We have seen nationalization in that sector. And so it is not a structurally advantaged sector for us to play in here in the U.K.

It also meant we had to review our German and Dutch positions because they run off a lot of common infrastructure. It wouldn’t make sense to look at just one of them in isolation. That’s what triggers the review and our ability to be able to understand how we can — or what position we need to take going forward, and that will take a few months.

Our broader low-carbon opportunities will, again, like everything else, also in our Upstream, be assessed on their own merits. Opportunities that we can see running room in, we’re going to continue to scale up and invest in and grow. And we’ve seen some of these opportunities, and we can talk about that as well in the coming hour.

On the — on where we are with Upstream. Having had the privilege of being with Sinead in the Upstream business at the time when we set these targets, we have indeed moved very fast on being able to monetize the parts of the portfolio that we felt did not fit into the broader core of what we wanted in the Upstream. And just as a reminder, we’ve done a lot of work in the Upstream over the past several years to fundamentally high grade the quality of that asset base. I referenced earlier in the morning, the fact that in 2014, at the similar Brent price, we were delivering — we had in 2022, 7% less production than we had in 2014, yet we’re able to deliver some 80-plus percent free cash flow and 70-plus percent earnings. And therefore, the quality of the Upstream has significantly improved as a result of this focus on value over volume.

As we look into the future, longevity of Upstream and our Upstream resource is a key focus area for me and for Sinead. That’s going to be something we focus on. More on exactly how that looks, I think, is better discussed in our Capital Markets Day in June 2023. But longevity is a core part of our focus.

Thank you for that — for those two questions, Biraj.

Operator

The next question is from Christopher Kuplent at Bank of America Global Research.

Christopher Kuplent

Wael, let me take your last comment and ask you a very mean question. What else did you feel like you can’t tell us today that you’re going to focus on in June? So apologies already for that question. But maybe I might want to make a suggestion to review that payout ratio. How do you feel about the formal 20% to 30%? As you’ve highlighted, you’ve gone well beyond that. It seems a little outdated. So hopefully, we can look forward to an update on that front as well as the longevity point that you just made. So any other thoughts in terms of what keeps you busy as you prepare for June would be great. And I’m not asking for a full preview of that event.

And then a quick one, hopefully, for Sinead. Just wondering whether you can give us a little bit of detail in terms of what you expect into Q1, Q2 when it comes to both the net working capital potentially a bit reversing as well as those derivative margining costs that went the other way in Q4.

Wael Sawan

Thanks, Chris. I’m going to ask Sinead, if you want to cover Q1, Q2 and maybe also the point around distributions. The — and then I’ll come back and cover any other items on June.

Sinead Gorman

Super. Indeed. No. Thanks, Christopher. And specifically on working capital. So in terms of the working capital, we’ve had comments in the past about the fact that our working capital has been an outflow. And as you saw this quarter, it was a substantial inflow of over $10 billion as well. Volatility comes with working capital. Our working capital comes from volatility is probably a better way of putting it. And we are in a great position where we have the financial framework that allows us to take this and have the capability to make money from us, of course.

So as we play through that, what are we expecting to see? In terms of the working capital that occurred this quarter, there were a number of things. It was price that came down obviously impacted. We saw a change less outflows with respect to margin, which you referred to as well, and that was to active management. We really looked at what are the right returns we need for that side of things and for the margining. And the third one is some one-offs. So in those one-offs, we saw quite a few people actually prepaying us towards year-end, so their own form of active cash management. And we also saw, of course, some cash deposits from some of our joint ventures who have to pay tax in January rather than in December. So just a change in terms of how taxes are playing out for them.

As such, specifically to your question, how much do I expect to see? I’m probably seeing $4 billion to $5 billion of that number that came in, I would expect to see flow out. Now of course, that’s just simply about things that will reverse in Q1. How working capital will play out will depend on, as you well know, the pricing and the different deals that we do during that quarter. So I won’t speculate more than that. I would say that our margin, we’re very active in looking at, and we’re ensuring we have an appropriate return for it.

You also asked about the payout ratio, which I think you said was outdated. With respect to the payout ratio, as you know, we’ve been quite clear on this and the fact that we have 20% to 30% range of CFFO. And taking a step back from that as well, 20% to 30%, well, as you can see, when market conditions and economic conditions allow for it, we go beyond that. So you can see in the course of the year, we actually got to 35%. That’s not about being outdated. That’s about an effect of us having 20% to 30% through the cycle, and that’s why we are very, very clear on the fact that it is a soft ceiling and a hard floor if that helps.

Wael Sawan

Thanks for that, Sinead. Let me touch on the broader question of what to expect in June. I think Chris, it’s worthwhile to sort of restate here that I continue to believe that our Powering Progress strategy is the right strategy for us and that the focus that at least I’m really keen to bring is how we’re going to operationalize that strategy.

When we start from an incredibly privileged position; when you have something as strong as your current core Upstream business that is delivering significant value, higher margins, strong, strong performance overall; when you have this world-leading Integrated Gas business, of which we’ve been able to significant strength as well in 2022 with the many announcements we’ve made; and when you have the customer interface that we have with a very strong Marketing business, we start from a very strong position. And we recognize that as we move forward, we can continue to grow and strengthen that position while continuing to decarbonize our own assets and help our customers decarbonize their energy.

So that core is very, very strong. But there’s 2 pieces that I have said, and I’ll continue to reiterate. Our focus is going to be on performance and discipline. Performance is going to be very much about how do we continue to drive operational excellence in our business? How do we focus on making sure that we are getting the consistency and the predictability in our overall results? And so that has all sorts of elements around how we think about working capital and the like. But also how do we continue to be lean and fit in what is an inflationary environment? So those are all elements of the performance.

And why do we focus on performance? Because I think there’s a lot more running room in the company. I know we’ve left money on the table in my previous business in Integrated Gas this year, so we can do better. And that’s the aim. We want to really drive that performance.

And ultimately, to your question around distributions, if we can drive the performance to its full potential, we will have sufficient cash to be able to distribute even more to our shareholders. And that’s very much a core part of our focus. And when it comes to discipline, it’s about making sure we continue to be ruthless in our allocation of capital towards the value-enhancing opportunities we see there.

And so you’ll hear a lot more of that. I’ve given you a bit of a preview, and you’ll get a bit more of the details as we work them out over the coming few months. Chris, thank you for that question.

Operator

The next question is from Lydia Rainforth at Barclays.

Lydia Rainforth

Two questions, if I could. Firstly, Wael, on the exec committee changes, you’ve talked about making the business simpler and that pure interfaces mean greater cooperation, discipline and faith. What in practice are you changing about that capital allocation process? And what leaves it to be better effectively?

And then just picking up on what you’re thinking about the operational performance and particularly in Integrated Gas, it does look like that’s been disappointing certainly relative to history. What can actually be done to improve that performance? And I’m not asking you to give too much, but just in terms of any kind of gap that you think is really there that we need to look at.

Wael Sawan

Yes, sure. I think on the first one, on the executive committee changes, I just mentioned to Chris’ question there, Lydia, the fact that performance and discipline were key going forward. And those were the 2 that also played in the decisions around the executive committee changes. And let me elaborate on that. And through that, maybe pick up on the operational performance question as well.

The structure we are creating is one where we’re trying to minimize interfaces to be able to really allow the front line to deliver the value that’s needed with clear line of sight that the business directors have. In this case, our Upstream, Integrated Gas director as well as our Downstream and RES directors to have clear line of sight towards those business outcomes while the integration of our strategy as well as finance as well as M&A into one shop that will report into Sinead is meant to be able to allow us to ensure that strategy, capital allocation, the monitoring of performance to make sure that our capital is being allocated to where we see sustained strong performance, that loop has been sort of cut across 3 different parts of the organization comes together now. And so when we talk about discipline, it’s our ability to be able to look life cycle at the choices we make in the way we allocate capital and continue to improve the way we do that in an objective way, unemotional way, rather than leaving it to each business to sort of try to pitch for their own capital.

So that’s really a core part of it. In that strand, when you talk — when we talk about operational performance and coming to the Integrated Gas assets, I want to maybe correct a bit of an impression because there’s 2 things that we’re working on hard in Integrated Gas. There’s one element around feedstock in certain areas like Nigeria and Trinidad that has nothing to do with performance. The assets are doing very, very, very well. The problem is it’s really challenging in Nigeria, given sabotage of the pipelines and the like to be able to get sufficient gas into the system. If we can overcome some of those challenges, the machine runs well.

In Trinidad, it’s simply a lack of gas supply. And you’ve heard recently that the U.S. government has — OFAC has allowed now Trinidadian government and Shell to consider bringing gas from the Dragon field in Venezuela. So those are the sorts of solutions for that part of the problem.

The other challenge we’ve had is, in particular, Prelude has been a challenge, and that’s one that we are very focused on right now with the team, and the leadership in Australia is really looking forensically at what are the things that would potentially mitigate further challenges.

And that’s what I would say at the stage, Lydia, around where our focus has been. Thank you for the question.

Operator

The next question is from Michele Vigna from Goldman Sachs.

Michele Vigna

Really, congratulations for the excellent delivery in the quarter. I wanted to ask 2 questions. The first one is about the EU green taxonomy. It’s going to be one of the biggest new regulations from an ESG perspective in Europe. It’s far from perfect, but it still offers an interesting insight in change towards a greener company with especially the percentage of green CapEx. And I was wondering if you had an initial assessment of what percentage of your CapEx would be green taxonomy-aligned.

My second question relates to the gas market. You are one of the largest players worldwide. It seems to me like the market is getting a little bit too relaxed about the risks in the second half of the year. The price incentive is moving away from substitution. Gas-intensive industries are restarting in the EU. And I wonder if we run into a risk of potentially having another crisis this winter and how you think you can position yourself to be best positioned to benefit from that.

Wael Sawan

Thank you for those, Michele. Do you want to start off, Sinead, with EU green taxonomy?

Sinead Gorman

Indeed. So indeed, Michele, it’s a really interesting one, the EU green taxonomy because, as you know, it will play out and be delivered across just a different period of time. Whether you’re in the EU, whether you’re part of the U.K., the timing of that will change. What you can do is actually, if you look back at our annual report from last year, you can see where we actually showed a breakdown of how the taxonomy works. And actually, the spend that we would say fits very well, and we sort of described our points of why we didn’t feel the taxonomy was actually properly worded, et cetera. So that taxonomy is playing out. As you know, definitions are being challenged at the moment, and a variety of that will happen.

So I would say, look back at our one from last year. So from 2021, and you’ll get a very good indication of that. What I would say as well, of course, is that we want consistency. That’s the main thing. We have so many different regulations and rules that are coming, whether it’s from the U.S., whether it’s from the EU, whether it’s coming from the U.K., or a benefit to all of us is to have standardization, transparency where we all use the same definitions. And we’re very keen to do that as an industry.

Of course, what we’ve said before, and I described it this morning several times as well, was the fact that if you were to look at our CapEx and our OpEx together, we would say that 1/3 of that approximately at the moment is spent on low-carbon or zero-carbon investments or expenditure as well.

Wael Sawan

Thanks for that, Sinead. Michele, to your question around gas markets. When asked this morning in both CNBC and Bloomberg, my answer was the same that we are not out of the energy crisis in Europe. Far from, I think. And I would agree with your point that there seems to be some who feel that it’s all back to normal. This is, I think, a multiyear energy crisis, and we want to have to collectively figure out how we address that.

Why do I say that? I think just looking at some of the facts. So last year, what happened with Russia was roughly 2.5% of global gas demand was taken out because of the reduction in gas supplies from Russia into Europe. That caused havoc in the markets, as you know well.

What supported or what bridged the gap, of course, LNG played an important role. Mild weather played an important draw, and critically, demand destruction also played an important role. Let’s take the first one. There isn’t a huge amount of LNG coming into the market over the next 2 years. It’s around 20 million tonnes is what we see, but that’s about it. And that one shouldn’t also forget that many of these machines have been running hard now for a good year. And you’re beginning to see some of the challenges in just the reliability of the machines around the world. So that’s an issue.

The second issue, of course, is that China was the one that diverted roughly 50% of its LNG to come here to Europe or 50% of Europe’s needs was met with diverted LNG cargoes from China. That might change or is likely to change given where things are going with the recovery — the economic recovery in China.

So you look at that, you don’t want to be in a position to be depending on the weather as your savior or the fact that you’re going to destroy more demand. And so I do think this is a multiyear issue. We’ve been very vocal with governments here in Europe that we’re going to have to move faster. What the Shell do as a result of this, of course, our portfolio has typically been positioned for Northern Hemisphere winters. That’s where we typically have our . We, of course, work on significant support in storage this year — or last year, sorry, we invested in storage in Germany and in Austria, which was part of where we used our working capital, for example. We’re investing in projects right now. We have Pierce depressurization that’s coming on stream in Penguins in the U.K.

So we have a lot of opportunities to be able to supply the market and, of course, create value through the tremendous portfolio that we have in LNG. Thank you for the question, Michele.

Operator

The next question is from Christyan Malek at JPMorgan.

Christyan Malek

Congratulations on the results. So 2 questions from me. Just first, sort of slightly different topic but some related on the industrial and financial logic of renewables at this stage with energy transition. One of your peers sort of appears to be dialing back in renewables and into the returns proposition or the evolving returns. Can you share more views on the case to scale clean energy at this point, be it M&A or organic and so the time lines around how you think about the transition in the context of clean energy?

My second question is regarding the oil outlook specifically. What does it take for you to grab the bull by the horns in oil investment and break out of the range you provided? As it still seems somewhat in contrast, the U.S. majors who are leaning into low-growth . Yes, you framed the mood as more volatile and uncertain, and you’re talking about energy crisis again on the other hand. So I’m just trying to understand what are the key milestones we’re looking to see for you to step in on particularly the crude side.

Wael Sawan

Super. Thank you, Christyan, for those 2 questions. Sinead, do you want to start with the industrial and financial logic of how we’re thinking about renewables?

Sinead Gorman

Yes, indeed. I’ll keep it simple, Christyan. It sounds like you’re in an airport without a doubt. But what I am seeing on that is the logic is very simple for us. We look first at whether any of the investments that come to us are fitting our strategic way forward. And then we’re looking at very much how does it fit in terms of the returns profile. And we probably had this conversation before on that. Each investment has to fit both aspects of it. And on the return side, what we’re seeing, of course, is that we have many different projects that are open to us. So we’re not short of investment opportunities. It’s finding the right one where we can actually differentiate and we can get those specific returns. I’m very comfortable that we have the right strategy for that. So that’s where we’re going to.

But in terms of the — are we dialing back or any of that side of things, you can see from our capital investment, we have a very healthy budget within the side of things with respect to renewables, in respect to green. But it will depend, of course, on the returns that we see as those come through, and that will continue to be the case. At the moment, we’re seeing good opportunities, Nature Energy being a great one where, of course, it’s just a logic where it fits through. We’re good at molecules. We’re able to move those to different locations. And of course, having the sort of business that we have with a number of customers to be able to decarbonize them, it’s a very clear logic as well.

Wael Sawan

Thanks for that, Sinead. Let me take the oil bit, Christyan. I think first to step back, I think the strategy that we have is a very balanced strategy. I mean we’re playing the game for the short, medium and long term. So we’re looking at how do we create value for our shareholders today but also how do we create the value opportunities for 2040 when the energy system will be fundamentally different.

By the way, by 2040, I’m still convinced you’re going to need oil and you’re going to need gas and you’re going to need a lot more renewables. And so our strategy is one that’s saying, how do we play across these multiple energy forms but really focus on the opportunities that create the most value for us, a bit like what we’ve done in Upstream, where we have gone to the core of 8 countries and really doubled down. And you’re seeing the benefits of that through margin expansion and our ability to really focus on value drive.

Does that mean we will continue to look at that? Absolutely, you’ve heard me say earlier as well, we will continue to look at how do we have longevity in our oil business. But I would also say I love the fact that we have a world-leading Integrated Gas business that actually has a significant portion, north of 70% of our term contracts indexed to Brent. I want to continue to grow that part of the business because I can get exposure to a business that we are uniquely differentiated in that gives Brent exposure and, at the same time, where we are able to have much more resilience as we go through the energy transition because of the lower-carbon footprint of that business.

That is at the core of the strategy. And so we will continue to follow that. And we’ve built on that in 2022, the North Field expansion, North Field South, our ability to be able to pick up significant volumes from the U.S. through Venture Global, Mexico Pacific Limited. And so we’re really putting that strategy into action to be able to grow without necessarily saying it just has to be oil, but oil exposure is a good thing for us as a company, and that’s what we’re really looking. That exposure to Brent is going to be important.

Thank you for the question, Christyan. Safe travels wherever you’re going as well.

Operator

The next question is from Irene Himona at Societe Generale.

Irene Himona

My first question, if I can go back to the cash payout ratio, please. You point to 20% to 30% through the cycle and 35% at current prices. To be fair that 35% was clearly helped by the proceeds from the Permian disposal. My question is, can you give us a sense and indication of what for you is the Brent oil price which you would consider as average through the cycle and which would, therefore, correspond to the 20% to 30%?

And then the second question, just a numerical one on RES. Capital employed more than doubled basically between Q2 and the end of the year. I presume this was due to the spike in power prices possibly more working capital for trading. Is that correct? Or is there anything else behind the increase?

Wael Sawan

Thanks. Do you want to take both?

Sinead Gorman

Yes. I’ll take both. So on the RES one, Irene, very simply put, there’s a mixture in there. You’re completely right. The working capital part of it is to do with power. But a large part of it is to do with the build into storage. So we talked about earlier, Germany and Austria, also some storage in the U.K., of course, as well. So you saw — between Q2 and Q3, you saw that go up. You saw a little bit of that come down in terms of the storage side of things as well as it played out. So that’s part of what occurs there. That will play out as we release out of storage as well.

If I were to look at the first one as well that you asked around the payout ratio, fundamentally, it’s — if you said Permian, it’s still above 30% as well. So I do acknowledge, yes, the Permian is in there. But of course, that’s part of the capital allocation that we have. We make choices about which assets we are best kept — best suited to keep and which should go out of the portfolio as well. Of course, that has implications on the CFFO as well that plays through. But we were over 30% in either way that you look at it.

We tend to look at in terms of price because you were quite specific on the price. I’m not going to be drawn on what specific price it is. As you can imagine, we look at scenarios. We don’t look at one specific price or strip probably quite sensible as you can imagine, given how volatile we’ve seen in the last year as well. So we look at the different aspects of that. And that’s how we play out as we plan beyond just next quarter but through the cycle as we look to invest.

Wael Sawan

Thank you for that, Sinead. Irene, thank you for the question.

Operator

The next question is from Henri Patricot at UBS.

Henri Patricot

A couple of questions from me. The first one, a follow-up on renewables and the changes to the executive committee. Can you expand on the rationale for grouping renewables with the Downstream and whether this has any implications for the strategy for renewables?

And then secondly, on Chemicals with the start-up of Shell Polymers Monaca, not just making full contribution. How long do you expect for that asset to ramp up to get to full contribution to earnings? And should we expect to [indiscernible] improvement in the first quarter? Or does that take a bit longer?

Wael Sawan

You want to take the second question [indiscernible]?

Sinead Gorman

Sure. Absolutely. No, indeed. And thank you, Henri. Yes, Shell Polymers Monaca, really great to see it actually starting up and beginning to run through. It’s quite exciting when you’re actually there and just see it. In terms of the ramp-up, you can imagine with anything of this size, I’d love to say we’d get up and running within a couple of months. It doesn’t. It always takes approximately 12 months by the time you run up, you get certified on the quality of the products, et cetera. So that’s what we’re seeing. So you’ll start to see it play out in the results more and more. Of course, we’re getting all of the costs coming through now that we’re operating, but the true value of it will take approximately 12 months to play out, and then you’ll really see it hitting.

Wael Sawan

Thank you, Sinead. Then on the first question, Henri, on the RES-Downstream grouping. Dial back to 2017 when we started the renewables business, it was really nascent. We were looking at how do we think about power, how do we think about hydrogen, how do we think about CCS. And so that’s been evolving. And what you have seen, in particular in 2022, we made some big moves, right? So we made a fine investment decision on a green hydrogen project in Rotterdam, leveraging our requirements in Pernis while, at the same time, being able to leverage our leading commercial road transport business as a potential sync for that green hydrogen and leveraging, of course, also the very strong incentives from the European government. We’ve made moves in India and in the U.S. around Sprng and Savion, respectively. And we continue to look at those opportunities.

So we have a good base. The reality, of course, is we’ve always talked about a customer-backed strategy, and the majority of our customers have traditionally sat in our more conventional business in Downstream. And so there has been quite a bit of an interface between renewables and Downstream, what products should we be selling to our customer and the like. And so what this is doing is actually it’s strengthening our ability to access customers with green products that we are developing in our renewables business. It also harmonizes things because, currently, biofuels, for example, sits in Downstream, doesn’t sit in renewables. EV charging sits in Downstream, even though the power generation and power trading sits in renewables. So this is bringing cohesion, removing interfaces and duplication and allowing us to make sure that we can deliver for our customers the decarbonized products that they want. And then being agnostic as to what green electron or green molecule they want just trying to maximize value for the group from doing that. Thank you for the question, Henri.

Operator

The next question is from Lucas Herrmann at Exane.

Lucas Herrmann

A couple, if I might. Sinead, this is probably directed at you because it’s LNG and it’s first quarter. And look, we’ve had a year of considerable volatility. You’re a month into the quarter. Price has obviously been volatile. But can you give us any help in terms of how we should be thinking about the way that the current quarter is likely to shape up in LNG? Sorry, it’s so short term.

And perhaps staying with gas, if I go back to last quarter, gas storage, a lot have gone into gas storage. You indicated the benefits of that would be seen through the fourth quarter, maybe the first quarter. Where are we in that process? Has it all been released? Have the benefits been seen? Please, just commentary around both those items.

Wael Sawan

Go for it both.

Sinead Gorman

Thank you. Indeed. Thanks a lot, Lucas. Indeed, so you’re commenting, first of all, and let’s start with the LNG one, specifically. So in terms of the volatility and what we expect to see coming into this quarter. So strong pricing. Now if you go back to what happens, we’ve talked about supply, seasonality and, in effect, the dislocations.

So in terms of the supply, you typically see us being a bit longer in terms of Q4 and Q1. And we would expect to see that playing out as well. Hedging will work as intended. I have enough sense to not try and go anywhere on that because it will depend on where the markets will play out at the same time. But seasonality and the supply side, we hope and expect to work for us on that.

Of course, it also comes down to how much third-party volumes we can actually access as well. And that’s — as Wael already discussed, it’s going well. And of course, the performance of our equity production as well. It’s great to see Prelude up and running and performing well at the moment.

In terms of the gas and referring to, basically, we talked about — last quarter, I talked about how we had been injecting into storage as well. We’ve seen some being drawn out of that, particularly around Austria, so that has come out in this quarter, but we still have quite a bit in storage as well. Of course, it’s mild at the moment in terms of the winter warmer, if you want to put it that way. So that will have to play out as it goes through as well. I hope that helps.

Wael Sawan

Thanks, Sinead. Thanks for that, Lucas.

Operator

The next question is from Paul Cheng at Scotiabank.

Paul Cheng

Two questions, please. First, Wael, as the new CEO, first, congratulations. That how you look at Europe in the long term as a part of their long-term portfolio given the political environment for your legacy business, I mean, you’ve been reducing your Upstream exposure in Europe by half over the past 5 years. The Downstream still has a lot of operations there. So I mean how do you look at that?

And secondly, that if we look at in the past, both Shell and your peers sort of target or accept the wind and solar on an absolute return will be lower than your legacy business, like that you will target 8% to 10%. But is that acceptable going forward? And as a new CEO, when you look at it, will you be willing to accept just because there’s no carbon that we generate a much lower return than your legacy business?

Wael Sawan

Thank you very much. Thanks for that, Paul. And let me take both. So on Europe, you’re right. We don’t have a huge amount of Upstream left in Europe. We still have, of course, positions in the U.K. We still have positions in Norway and Italy. But the majority, in particular, when you think deepwater is in the U.S. and in Brazil. And then we have strong positions, of course, in Kazakhstan, in Oman, in Brunei, Malaysia and so on. So you’re right to point out that it has shrunk over time. And we still have, indeed, in particular, when you think about our Energy and Chemicals Parks, we have the Energy and Chemicals Parks in the Netherlands as well as the one in Germany.

It is fair to say that there’s a couple of considerations around Europe. We see Europe much more going forward as an energy transition play. We see a lot more in terms of the incentives that play into Europe. We see our ability to be able to leverage our German and Dutch position in a way as well as our marketing positions in Europe in aviation, in commercial road transport, in passenger transport. Those lend themselves very well to be able to play in the energy transition, and it is in line with where Europe wants to go.

So I see a strong part of our focus, and you see it. You see it with the investments we’re making, for example, with offshore wind in the Netherlands, green hydrogen in the Netherlands looking at opportunities to continue to decarbonize customers in Germany, in Italy and so on and so forth. So there is more of that while we continue to be committed to our oil and gas businesses in other parts of the world as well as whatever we still have here. But definitely, I think the disproportionate share of capital that’s going into Europe is an energy transition theme.

The important thing I keep trying to remind the government in Europe is that, that capital that really needs to be — or I need to be comfortable that we see investment stability in the climate in Europe. And I have to say 2022 did not reinforce that confidence. We have seen ad hoc interventions in windfall taxes, in price caps, in some areas, nationalization and the like. Of course, these are extreme conditions. I fully understand that. But any time you start to move from trying to manage risk to trying to manage price creates all sorts of concerns in a company like ours that’s investing for the long term. So I would just leave that out there as well.

I think on low carbon, let me be, I think, categorical in this. We will drive for strong returns in any business we go into. We cannot justify going for a low return. Our shareholders deserve to see us going after strong returns. If we cannot achieve the double-digit returns in a business, we need to question very hard whether we should continue in that business. Absolutely, we want to continue to go for lower and lower and lower carbon, but it has to be profitable.

And so I recognize there’s a different risk profile. Let’s be clear, Upstream hasn’t always been in the 20% returns. On a commodity — or on a commodity basis, you find that the risk typically plays between the 10% to 15%. We need to be able to see those sorts of returns on an integrated value chain basis in the renewables as well, and that’s what we’re focused on. And we have great examples of that. We’ll share a bit more of that in Capital Markets Day through getting in at the right time, through diluting, through creating more value all the way down the value chain, but it is important to say we will continue to focus on value and returns.

Operator

The next question is from Amy Wong at Credit Suisse.

Amy Wong

A couple of questions from me. The first one is looking at your operating expenses. It seems like it’s been creeping up across the group. So could we get a bit more color on what’s happening with underlying OpEx and whether management has plans to address that?

And then my second question is unrelated, but it’s related, and it’s more about your Upstream and Integrated Gas business, particularly your exploration strategy. It’s not an area we hear a lot about on your exploration there. I mean a couple of years ago, you told us that you had a commercial resource base of over 20 years of production. I’m just kind of rolling that number forward. Where do we sit there?

Wael Sawan

Amy, thank you. Do you want to take both of these?

Sinead Gorman

Sure. So on the OpEx or operating expenditure, Amy. So for this year, it has gone up, where it’s sort of some 39 billion. What we’re seeing there is, number one, there’s a bit of a Q4 effect, which is always there related to just some of the costs that tend to come through. But if I take a step back because, of course, it’s one that I watch very closely. When you look at it for the full year, what are we seeing for that increase? We’re seeing inflation hitting. It really is. We’re seeing that come through in just across the different cost bases. We’re also seeing, of course, our D&R or decommissioning and restoration. We’re spending more in that space as well. That’s good expenditure, but it’s also an element of inflation in there as well.

We’re also growing. So a number of those new investments that have come in, that OpEx for those new ones at the start is just more. We have to get on top of that, and it’s higher than we’re seeing in terms of the divestments that are coming through. So that’s flowing as well.

And then finally, just the same as everyone else, the utility costs, of course, have increased this year. We’re seeing it flow through our own results. Are we happy with it? No. Will it be an area of focus? Yes.

In terms of your second question, which was really around our exploration strategy, we have a great exploration team. And they’re still very much focused on various areas. You’re seeing some of the progress coming through in terms of Namibia and some other aspects as well. What you we’re talking about specifically, I’m going to take it back to sort of our reserves numbers there as well. So you’ll see our reserve replacement ratio, of course, at 120% for this year as well. But what I would look at there is we’ve often talked, of course, and you’ve heard us say many times about volume over value. But fundamentally, we want to see the longevity of our Upstream and IG businesses. These are fabulous businesses, and they’re generating great returns, and we’re very much focused on that.

The reserves numbers that we see coming through, those are very much around the requirements that you have, the SEC reporting, and we adhere very, very closely to that. Of course, it does mean that some of the things just don’t flow through in those numbers but are still producing and making us money. So very clearly, it is value over volume. Yes, so I hope that helps.

Wael Sawan

Thank you for that, Sinead. And thanks, Amy. Giacomo? Dan, I understand Giacomo is next.

Operator

Yes. The next question is from Giacomo Romeo at Jefferies.

Giacomo Romeo

Congratulations, Wael, for your excellent start of the new tenure here as CEO. Two questions left. First one is on Chemicals. We have seen a disappointing numbers and losses getting larger. Just wanted to understand whether there’s anything you can do there on the cost side to mitigate some of these effects and whether what you’re seeing in terms of the market right now if you start to see a little bit of an improvement.

The second question is on liquefaction. You give us a liquefaction guidance for the first quarter. And it looks just over the — what you reported for this — for Q4, and it’s — which was a quarter where you had quite a bit of hiccups. So I’m just wondering what shall we expect in terms of if this range you give for first quarter, it should be a reliable level of liquefaction that we can apply for the following quarters in 2023 or whether we could see an improvement there.

Wael Sawan

Thank you very much, Giacomo. Do you want to talk about liquefaction? I can touch on Chemicals.

Sinead Gorman

Sure. I’ll be very short on the liquefaction. We put it out quarter-to-quarter, of course, because it is the best estimate that we have at the time, Giacomo. So it’s a good estimate for where we are seeing for Q1. We obviously have a different phasing for turnarounds, et cetera. We don’t tend to bring — go out with those in advance. So you’ll see that play out over the year as it’s phased. But what you’re seeing is a very good estimate for Q1.

Wael Sawan

Thanks, Sinead. And Giacomo, with your question around Chemicals. I think there’s a couple of things that we’re looking at. Firstly, of course, we’re at the bottom of the cycle on Chemicals. So it’s painful where we are, but this is a cyclical sector, of course. The structural, there’s little we can do about at this stage. The performance we’re very focused on. So indeed, we’re looking at all opportunities to be able to pull levers that we can, whether that’s from a cost perspective or how do we enhance the top line. That’s what the team is focused on and continuing to drive hard at the moment.

In addition to that, we continue to play out the strategy that we have, which is shifting more and more away from commodity chemicals to intermediate and to performance chemicals. That’s an important part of it, and we have some good opportunities to continue to do that. Earlier, we talked about Shell Polymers Monaca. The whole point of continuing to certify these 40 grades is to continue to actually add value to the molecules we have and to the pellets we have and to be able to make sure that we maximize the return that we get from selling those. So all sorts of ideas being worked to ensure that we counter the cyclicality and are ready when we start to move back up the cycle to be able to maximize value for our shareholders from that.

Thank you, Giacomo, for the question.

Operator

The next question is from Peter Low at Redburn.

Peter Low

Just one and one more on Integrated Gas. Clearly, a very strong result. Is [indiscernible] say to help us try and quantify the contribution from trading and optimization. I guess what I’m trying to gauge to what extent this was an exceptional quarter versus being within the range of normal volatility you actually expect within that business. So yes, any color around that would be very helpful.

Wael Sawan

Okay. Thank you for that, as well, Peter. Do you want to say a word on that?

Sinead Gorman

Sure. I would say Q4 was a very strong trading quarter. It was exceptional in isolation, absolutely. But we tend to, as I’ve said before, really is good to look at it across the 12 months. So when you look at it across the 12 months, our Integrated Gas as an entirety to both the physical assets and the trading and optimization part have had a great year. It really is fabulous. And when you look at that, of course, trading and optimization has played a key role in that, but I wouldn’t look at it from quarter-to-quarter. As I said, it’s much, much better to look at it across the 12 months.

Operator

So the final question is from Jason Gabelman at Cowen.

Jason Gabelman

My phone actually cut out on the part of that question, so I may be asking the same question I was just asked, and if so, I apologize. I actually have 2. The first one is on Integrated Gas. And there’s clearly an elevated seasonality in the business, as you alluded to, that seems kind of underappreciated by the market. And I’m trying to understand how to quantify that. And I guess I’ll ask the question in this way. 4Q was very strong. If we had a similar environment in 2Q or 3Q, do you have any sense of how much different the earnings would have been? Can you give us an order of magnitude on that? And then my second question is on the…

Wael Sawan

Sorry, Jason, we lost you when you started to talk about the second question. Can you repeat the second one?

Jason Gabelman

Business model. The way it was kind of communicated was add a lot of options in optimizing those electrons [indiscernible] value chain, which I would have guessed included this retail energy business. If you decide to move away from retail energy in Europe and that removes one of the avenues to optimize those electrons, does that change how you think about the return profile potential of the renewable power business?

Wael Sawan

Thank you for that, Jason. I think I picked up the second one. Let me take a shot at both and build off what you said there, Sinead, on the first one. So Jason, I think the way to reflect on this and what Sinead had mentioned earlier is the importance of looking at this across 4 quarters. And what’s important is that we typically have a portfolio that is geared towards the Northern Hemisphere winter. So we try to go — to try to go longer in the Q4, Q1 months. And the way we do that typically is through supplementing our equity production with third-party volumes.

So the best way to look at some of the underlying performance is just look at the volumes we provide on a — over the last 2 years. And what you will see is quite some differences quarter-to-quarter in terms of that volume. Now I think what’s important to recognize is there’s different ways we create value in the Integrated Gas value chain. Of course, there is at the asset side, and you can see how much equity production we’re selling. We then create a significant amount of value at the T&O side. And then there’s a small piece that is also opportunistic as we play it.

My best advice is just look across the different quarters, look at the prices there, and you’ll get a good sense of it. This is not about us trying to not be transparent, but of course, as Sinead also said earlier, our hedging, the way we price manage our exposure is such that we look at it over an entire year and not simply quarter-by-quarter. We don’t manage it on a quarterly basis. And that’s why you can see sometimes the disruptions on a quarterly basis as you did in Q3. It doesn’t mean the fundamental business is not strong. It simply means that you have to look at it in a broader perspective.

On the — on our decision around Shell Energy Retail and the broader value chain, the strategy continues to hold, which is we believe we can create more value out of a green electron than simply selling a green electron through a PPA. We do that through a few ways. One is we have a balance sheet, and we have a trading organization that can take merchant risk — measured merchant risk, maybe 20%, 30%. And that allows us to be able to use that exposure to create incremental value beyond what a smaller operator can do.

We also have a huge B2B business that allows us to also cross-sell beyond the current molecules we’re selling those businesses. We could also provide them green electrons. And so that’s another avenue. A third avenue is indeed something like what we used to — want to do with Shell Energy Retail. That works in other markets. It works for us in Australia. It works for us in the U.S. at the moment. It is not working in the U.K., and that’s more to do with the structural nature of the market. So this is not a condemnation of B2C. It’s more a fundamental issue in the structure of the market that we are currently operating in, which has, therefore, necessitated this review that is still ongoing without any firm decisions taken at this stage.

Super. Jason, thank you for that. Dan, I think we’re done, aren’t we?

Operator

No. We do have one more question. We have a question from Alastair Syme at Citi.

Alastair Syme

Wael, can you talk a little bit about the Nature Energy acquisition, just the strategic rationale and any framework to help us think about the financials?

And then as a follow-up, I’m not sure I quite got the point you’re making on Upstream longevity. I guess the question is, do you think you can or want to grow your Upstream business? And I say that across the combined Upstream and IG [indiscernible].

Wael Sawan

Yes. Thanks for that, Alastair. Do you want to start maybe with Nature Energy? I’ll talk about the Upstream.

Sinead Gorman

Happy to. So indeed, thanks, Alastair. Glad we managed to fit it in. With respect to Nature Energy, so what do we see there? It was just a very logical strategic fit. When you look at the business that we have, so we have just such a huge customer base that is out there who have a strong need to decarbonize. And of course, you see that with both the convenience retail. You see that with aviation and stuff like that, but you also see beyond that. So what we’re seeing, of course, is that with Nature Energy when we bought it, it is both cash-accretive and earnings-accretive as well. So those 2 things play out as it goes through. It has a range of projects in the hopper, which are coming up to both FID, and the team has just set it up very well for growth. So we’re going to be able to take the amazing capability that they have in terms of actually generating these projects and be able to link it into the customers and create value in that sense.

Wael Sawan

Thanks, Sinead. Alastair, to the question around longevity. We will go after the most attractive projects that come our way. We don’t have a specific restriction where we’re not going to go into oil or into gas. Clearly, we think we have more gas opportunities at the moment because we’re able to add a lot of value. So yes, we are looking at growing our production in gas. And you can see it through our efforts on Integrated Gas, for example, what we did last year.

On oil, what we’re looking to do is to have just a much longer period of ability to be able to produce our oil profitably simply given where the world is. We continue to believe that oil has a role to play. A big part of what we announced a few years ago was how are we going to be able to move to actually prune the portfolio to high grade what we have as an Upstream business. I think we have done a lot of that, and therefore, what you see right now is a lot more strength and stability in that business, and I’d like to extend that strength and stability into the coming years.

Let me pause there, and thank you, Alastair, for the last question. And thank you all for your questions and for joining the call. Wishing you all a very pleasant end of the week and hope that you can join my team at our LNG outlook later this month as well as our annual ESG update in March. Thank you, everyone.

Shell Q4 Reflections

Feb. 02, 2023

Cavenagh Research

European IOC generated $39.9 billion of profits in 2022.

As exceptional Q4 2022 quarter highlights, European Oil Major Shell continues to make and distribute loads of cash. Supported by high energy prices, paired with robust demand, the IOCr generated $39.9 billion of profits in 2022.

On the backdrop of a demand tailwind coming from PRC, following the COVID reopening, as well as an improving economic environment in Europe, I expect oil prices to be elevated in 2023, and I expect Shell to write about $25 – $35 billion of profits.

I now calculate a fair implied share price of $101.47 (SHEL reference).

Thesis