Barbados

IMF Reaches Staff Level Agreement

May 17, 2019

End-of-Mission press releases include statements of IMF staff teams that convey preliminary findings after a visit to a country. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF’s Executive Board for discussion and decision.

A staff-level agreement was reached between the IMF staff and theBarbadian authorities on the First review of Barbados’ Economic Recoveryand Transformation program (BERT) supported by the Extended Fund Facility.

Barbados continues to make good progress in implementing its ambitiousand comprehensive economic reform program.

At the request of the Government of Barbados, an International Monetary Fund (IMF) team led by Bert van Selm visited Bridgetown from May 7–17, 2019 to discuss implementation of Barbados’ Economic Recovery and Transformation (BERT) plan, supported by the IMF under the Extended Fund Facility (EFF). To summarize the mission’s findings, Mr. van Selm made the following statement:

“Following productive discussions, the IMF team and the Barbadian authorities reached staff-level agreement on the completion of the first review under the EFF arrangement. The agreement is subject to approval by the IMF Executive Board, which is expected to consider the review in June. Upon completion of the review, SDR 35 million (about US$49 million) will be made available to Barbados, bringing the total disbursement to SDR 70 million.

“Barbados continues to make strong progress in implementing its ambitious and comprehensive economic reform program. International reserves, which reached a low of US$220 million (5–6 weeks of import coverage) at end-May 2018, have more than doubled since then. The rapid completion of the domestic part of a debt restructuring has been very helpful in reducing economic uncertainty, and the new terms agreed with creditors have put debt on a clear downward trajectory. The authorities have started the reform of State-Owned Enterprises (SOEs) by tightening reporting requirements and shedding excess staff.

“All program targets for end-March under the EFF have been met. The program target for Net International Reserves was met by a wide margin, as was the target for the Central Bank of Barbados’ Net Domestic Assets (NDA). The targets for the primary surplus, central government grants to SOEs, central government domestic arrears, and social spending were also met.

“In March, parliament adopted a budget FY2019/20 targeting a primary surplus of 6 percent of GDP. Full year effects of reforms set in motion during FY2018/19, including the introduction of several new taxes (an airline travel fee, room levies, a new fuel tax, and a new health service contribution), should help achieve this target. A broadening of the base of the VAT and the land tax, adopted in March 2019 in the context of the FY2019/20 budget, will help support revenue. The budget approved for FY2019/20 provides a solid basis for the targeted fiscal consolidation; the authorities stand ready to take additional measures if necessary to reach the targeted 6 percent primary surplus.

“The Barbadian authorities continue to make good progress in implementing structural benchmarks under the EFF, including those that contribute to an improved business climate such as a new Planning and Development Act passed in January 2019 and a Sandbox regime to regulate fintech start-ups set up in October 2018. A new Public Financial Management Act passed in January 2019 introduced wide-ranging measures to strengthen fiscal transparency and accountability. The government has also introduced a system for monitoring SOE arrears on an ongoing basis and has submitted a consolidated report on the performance of SOEs to parliament.

“Progress being made by the authorities in furthering good-faith discussions with external creditors is welcome. Continuing open dialogue and sharing of information will remain important in concluding an orderly debt restructuring process.

“The team would like to thank the authorities and the technical team for their openness and candid discussions.”

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: RANDA ELNAGAR

PHONE: +1 202 623-7100EMAIL: MEDIA@IMF.ORG

Dominica

Staff Concluding Statement of 2019 Article IV Mission

May 14, 2019

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF’s Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

1. The economy is recovering strongly following the destruction wrought by hurricane Maria. Output growth in 2019 is estimated at 10 percent, largely offsetting the cumulative decline of 10 percent since the hurricane. Construction has been the main sector leading the recovery, with large investments in infrastructure and public services, aimed at building resilience to natural disasters. Tourism and agriculture, key for exports and employment, are growing with support from government programs and financing, but remain significantly below potential in light of the significant loss of trees and equipment. Output is projected to reach pre-hurricane levels by 2020, and growth to rise above potential in the medium-term, owing largely to significant foreign investment in new hotels expected to start operations by end-2019. In the context of an uptick in tourism prospects, the increase in room supply above pre-hurricane levels should give a fillip to economic activity.

2. Large-scale public investment aimed at rehabilitation, reconstruction and resilience while contributing to growth, has worsened the fiscal outlook. The fiscal deficit is projected to remain large in FY2019/20 at 7 percent of GDP, but this is a significant improvement (4 percent of GDP) relative to the estimated outturn for FY2018/19. The narrowing of the deficit is explained by the recovery of tax revenues and more measured execution of public investment, owing to the decline of readily-available Citizenship-by-Investment (CBI) deposits. Beyond the near term, fiscal deficits are expected to narrow gradually with financing constraints becoming binding, constraining the space to sustain elevated levels of public investment. Based on conservative projections of CBI revenues and loan disbursements from multilateral and bilateral creditors, and given downwardly-rigid recurrent spending, staff projects the fiscal space for public investment to decline to 4 percent of GDP by 2023. This low level of investment is insufficient to sustain resilient infrastructure needs and is a large decline from the 15 percent of GDP annual investment average in the previous five years. Public debt remains high at around 80 percent of GDP in the medium term.

3. External current account deficits are projected to decline over the medium term, from over 40 percent of GDP in 2018 to 10 percent of GDP by 2024. This goes in tandem with a recovery of exports and a depletion of CBI and insurance deposits, which would reduce domestic demand to more sustainable levels. The outlook is, however, subject to significant uncertainty. In particular, higher-than-projected CBI revenues would increase external and fiscal deficits and increase growth further.

4. Reaching the ECCU public debt target of 60 percent of GDP by 2030 while sustaining resilient investment requires a well-designed fiscal consolidation plan. The government should prepare fiscal consolidation measures expeditiously, targeting savings of at least 6 percent of GDP to be adopted gradually over the medium term. Measures should be staggered over 5-6 years to smooth the likely negative impact on growth. The plan will support growth by increasing fiscal space for public investment while reducing government consumption, along with tax measures aimed at improving the efficiency of resource allocation:

5. On the revenue side, key measures could include a rationalization of tax incentives, with a cap on discretionary concessions and clear prioritization consistent with national development plans; a strengthening of tax auditing, which will require additional human resources; a restructuring of water and sewage service tariffs to achieve financial sustainability of the public provider; and a broadening of the base for personal income taxes, including by introducing a presumptive tax.

On the expenditure side, the government could consider a review of public wage allowances and a containment of wage increases below inflation; an acceleration of ongoing social security reform by bringing forward the planned increase in the retirement age and contribution rates and review of conditions for retirement eligibility–including longer contribution period and revised rules for pension determination in line with contribution effort. The efficiency of social transfers can be improved with proxy means-testing and better monitoring system of beneficiaries to minimize duplication and abuse.

5. Fiscal institutions can be strengthened to support the achievement of the regional debt target. Key enhancements could include (i) the adoption of a fiscal rule anchored on public debt, with escape clauses for natural disasters and other specified challenges; (ii) establishing a system to monitor the operations of state-owned enterprises, including for fiscal planning and identifying contingent liabilities; and (iii) setting aside CBI revenue in a well-governed government saving fund for natural disaster insurance, resilient investment, and debt reduction. These enhancements will help safeguard the fiscal space for building resilience to natural disasters, especially costly physical infrastructure and financial insurance, the core objective in the government’s national development plan. These measures will also support fiscal sustainability, by helping internalize the future costs associated with natural disasters and contain public debt accumulation.

6. The financial sector remains stable and is recovering gradually from the impact of the hurricane. However, more decisive action is needed to safeguard financial stability and support growth. Bank lending is expected to remain soft, owing to insufficient bankable projects, lack of financial statements required for loan qualification for most micro and small entrepreneurs, and lingering difficulties to enforce lending contracts in courts, including lengthy procedures for foreclosures and the seizing of collateral. The government should explore new options to strengthen capitalization and reduce NPLs of the indigenous banking sector. To this end, the plan submitted to the ECCB to assess the balance sheet impact of alternative capitalization options is an important first step. However, decisive action is needed to fully assess banks’ capitalization requirement. In this regard, two important steps are needed. First, the impact of IFRS9 standards on banks’ investment portfolio should be completed. Second, absent banks’ acceptance of NPL acquisition offers by the Eastern Caribbean Asset Management Corporation and the International Finance Corporation Asset Management Company, write-offs should begin expeditiously—NPLs remained stable, albeit elevated, at 17 percent in the past year. Progress on reducing NPLs would increase space for private sector financing to support growth.

7. Addressing balance sheet weakness of credit unions is important to safeguard membership savings, maintain financial inclusion, and minimize contingent fiscal cost. Capital and provisioning should be increased to meet the regulation requirement while doubling the effort to reduce NPLs. Options could include the use of retained earnings, notably by prohibiting dividend distribution if undercapitalized, capital calls to the membership, or through mergers to increase efficiency and reduce operating cost. To this end, the government should approve the already-prepared legislation to strengthen the enforcement power of the Financial Services Unit (FSU). This legislation should be passed without further delay and could be amended at a later stage when there is agreement on harmonized regulation across the region. In addition, the legislation should be reviewed to ensure the regulator has enough power to monitor and regulate high-interest pay-day lending, which is accelerating—it explains the bulk of the loan portfolio growth in 2018. Financial and human resources in the FSU need strengthening and would benefit from technical support from international experts. To strengthen regulation enforcement, the FSU should be established as an independent entity outside the Ministry of Finance. It should also be granted financial independence with legal power to collect fees and issue penalties for non-compliance.

8. Operations of the domestic insurance company should be discontinued, considering its insolvency and inability to honor outstanding claims following the hurricane. To this end, the government should approve the FSU plan recommending intervention and liquidation. Given risk of natural disasters, strong regulatory enforcement would enhance competition in the insurance market with more participation of internationally-diversified institutions and risk transfer.

9. Progress on improving AML/CFT legislation towards international standards will help reduce the risk of losing correspondent banking relationships. Ongoing actions to strengthen the AML/CFT framework, in line with 2018 CFATF mutual evaluation recommendations, will facilitate information access and coordination among all competent authorities, while improving the FSU’s analysis and enforcement. The phase-out of the off-shore banking sector should continue, and approval of revisions to the Offshore Banking Act, including higher capital requirements, license application process reform, and enactment of regulations, should be expedited.

10. The private sector needs to play a more prominent role to sustain growth in the long term:

To increase employment, legal constraints on working hours should be removed and severance payments for redundancy should be reviewed. Addressing educational gaps, in consultation with private employers, will help improve labor force adaptability and facilitate mobility –important considering seasonal demand in key sectors. The government could reform existing employment programs to facilitate labor market entry with on-the-job training in expanding sectors, especially tourism and agriculture.

Ongoing efforts to review construction and zoning regulations should be enforced strictly in light of vulnerability to natural disasters. This could reduce insurance costs and help coverage.

With low-cost geothermal generation expected by mid-2021, reduction of electricity tariffs will be feasible, improving competitiveness and reducing dependence on imported fossil fuels.

11. Data provision has shortcomings due to resource constraints in the statistical agency, resulting in insufficient coverage, accuracy, frequency, and timeliness of data. More timely and improved data pertaining to the national and fiscal accounts, labor market, the balance of payments, and non-bank financial institutions are needed for improved economic monitoring, budget planning, and policy formulation. Stronger incentives could be adopted for timely provision of data to the Central Statistics Office by reporting public and private entities.

Dominican authorities; Eastern Caribbean Central Bank (ECCB); and Fund staff estimates and projections.

[table id=14 /]

1/ At market prices.

2/ Data for fiscal years from July to June.

3/ Does not include grants received but not spent.

4/ Includes estimated commitments under the Petrocaribe arrangement with Venezuela.

5/ Includes public capital expenditure induced imports from 2019 onwards to account for possible mitigation of natural disasters.

6/ Comprises public sector external debt, foreign liabilities of commercial banks, and other private debt.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: RANDA ELNAGAR

PHONE: +1 202 623-7100EMAIL: MEDIA@IMF.OR

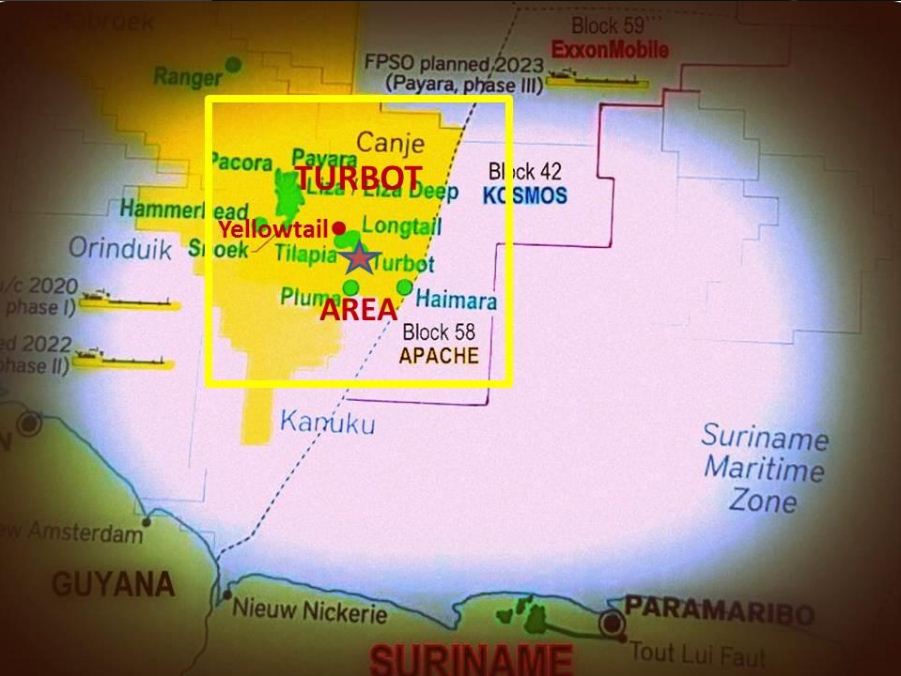

Suriname

Apache’s Block 58 in perspective to the oil finds by ExxonMobil offshore Guyana

Apache’s Block 58 in perspective to the oil finds by ExxonMobil offshore Guyana

Prolific oil discoveries offshore Guyana are not only splendid news for shareholders and the Government, but also for the neighbour to the east, Suriname.

Tax lawyer, Roy Shyamnarain reports that Block 58 offshore Suriname, got a de-risking boost, when ExxonMobil announced its 13th oil discovery at the Yellowtail-I. Block 58 is operated by Apache Corporation of Houston.

Yellowtail-I marks the fifth discovery in the Turbot Area in the eastern section of Stabroek. Block 58 is contiguous to Stabroek and is expected to hold a play type similar to the Turbot Area which further includes discoveries at Turbot-1, Longtail, Pluma and Tilapia-I.

The tax lawyer , a participant in international mining and petroleum conferences advised that the Stabroek and Block 58 lie in the Guyana-Suriname Basin, estimated to hold 13.6 billion barrels of oil and 32 trillion cubic feet of natural gas.

ExxonMobil expects the Turbot Area to become a major development hub, following Liza and Payara.

Another discovery in Stabroek, Haimara-I, is just miles away from Block 58 and is considered a potential new area by ExxonMobil. Location of Haimara proximate to Block 58 may be evidence that the play type of Stabroek must extend to the Suriname side .Turbot lies 40 km west of the maritime border with Suriname and 50 km east of the Liza well. Turbot, Longtail, Pluma, Tilapia, Yellowtail and Haimara indicate high quality hydrocarbon bearing sandstone reservoirs.

Grenada

Staff Concluding Statement of the 2019 Article IV Mission

May 28, 2019

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF’s Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

Growth has remained strong, reflecting external tailwinds and the fruits of past reforms. The outlook is promising, but is subject to downside risks. The focus of policy should shift toward making growth more sustainable, resilient, and inclusive. Fiscal policy should balance further progress in debt reduction against a gradual use of well-earned fiscal space to close the country’s infrastructure and resilience gaps, in tandem with capacity and efficiency improvements to bolster the impact on growth. Policies to enhance resilience to climate change and natural disasters should be fully integrated into a credible medium-term fiscal framework. Continued progress in financial sector oversight, structural reforms, economic governance, and data provision is necessary to support and enhance sustainable growth.

Developments and outlook

1. The Grenadian economy continues to grow robustly. GDP expanded by 4¼ percent in 2018, driven by strong activity in construction and tourism. Unemployment has been falling, but remains high at 21.7 percent as of mid-2018. Inflation has remained low. After trending down for several years, bank credit growth has turned positive with continued improvements in asset quality, while lending by credit unions has continued to expand rapidly. The external current account deficit likely narrowed in 2018 due to strong tourism receipts, but remains elevated at around 11 percent of GDP. Robust FDI flows, including from the citizenship-by-investment (CBI) program, are financing the external deficit while supporting economic growth.

2. Adherence to the fiscal responsibility framework has enabled further debt reduction. The key targets under the Fiscal Responsibility Law (FRL) are estimated to have been met. The fiscal surplus increased further in 2018, reflecting a combination of strong revenues and the FRL-mandated expenditure restraint. The public wage bill has been contained by the attrition policy, although several strategic exemptions and relaxations have recently been introduced to this policy. Low execution of grant financing and institutional bottlenecks in project execution combined to keep capital outlays subdued at 2¾ percent of GDP. Central government debt fell from 70 to 63½ percent of GDP in 2018, but arrears to certain bilateral creditors remain to be regularized. This measure of debt excludes non-guaranteed debt of public enterprises of around 3.4 percent of GDP and the debt to Petrocaribe (some 11½ percent of GDP). The improved debt situation has helped lower interest rates and boost access to concessional financing. Robust CBI inflows have helped channel sizable resources to the contingency fund that could be used for mitigating the effects of natural disasters.

3. Economic prospects are promising, but risks are tilted to the downside.

Growth is set to remain solid in 2019, but is projected to ease somewhat over the medium-term, consistent with a waning of FDI-driven construction. The fiscal position is projected to loosen in line with the FRL’s provisions that take effect after public debt falls below 55 percent of GDP, and should provide some support to the economy.

External risks are mainly on the downside, and are centered on prospects for U.S. growth and global financial conditions. Domestic risks are two-way. On the one hand, the use of the fiscal space for productive investment could improve growth. On the other hand, boosting public spending, without reforms aimed at improving efficiency and productivity, could undermine long-term growth. Other risks include the loss of corresponding banking relationships, damaging natural disasters, pension settlements or other spending that could breach the FRL, and regional risks due to spillovers from Venezuela.

Fiscal policy

4. The FRL has been successful in guiding fiscal policy to date, but its next phase of implementation should strike a proper balance between fiscal prudence and much-needed increases in productive spending. The government’s 3-year medium-term fiscal framework charts a policy course of continued large primary surpluses through 2021. However, once the public debt ratio reaches 55 percent of GDP, the FRL allows scope for recalibrating the primary balance target to stabilize debt at that level. An effective and prudent use of fiscal space could maximize the economy’s productive potential and resilience to shocks. However, if the fiscal space is used to finance unproductive spending, it could fuel debt sustainability concerns.

5. Grenada’s infrastructure and resilience gaps are key priorities that need to be addressed with the increased resource envelope. Public capital spending has been particularly low in recent years. The authorities’ assessments of infrastructure and maintenance needs call for substantially raising investment spending. In addition, significant advances are being made in understanding Grenada’s resilience-building needs and benefits, in the context of large expected losses from climate change. The ongoing climate change policy assessment (CCPA) has documented progress to date and laid out a comprehensive approach to address climate risks. It has identified the need for additional resilience-related investment of up to 3 percent of GDP annually over the next 10 years, some of which will need to be financed by domestic resource mobilization to back-stop and catalyze external concessional financing.

6. A scaling-up of public productive spending should have a substantial payoff for sustained growth, if it is supported by capacity improvements.The outcomes would crucially depend on specific policies and absorptive capacity improvements in public spending. Pro-actively pursuing capacity improvements (including in hiring and training professional staff and project prioritization and screening) in parallel with using the fiscal space to address infrastructure and resilience-building objectives would improve the quality and resilience of the public capital stock. Staff analysis indicates a substantial payoff of this investment for economic growth, both due to higher production and reduced losses from natural disaster and climate change events. Such investment spending could be supported by moderate increases in essential current spending and well-targeted increases in expenditures for social protection.

7. Moderate changes to the FRL and other elements of the fiscal framework could facilitate high-quality spending while further improving debt sustainability. First, targeting a safer debt level of below the FRL’s current ceiling (55 percent of GDP) and shifting to a broader coverage of public debt (to include non-guaranteed SOE debt) would support a proper balance between fiscal prudence and upscaling productive spending. Second, the analysis of fiscal risks in budget documents should be strengthened—notably to analyze and internalize fully the impact of natural disasters, climate change, and long-term aging—along with a comprehensive assessment of public enterprises, public-private partnerships, and other contingent liabilities. Third, the primary expenditure rule could be re-framed to simplify its operation and facilitate resilience-building objectives. However, prior to making any changes to the fiscal rule, significant enhancements should be made to boost capacity to implement resilience-related spending and improve the classification criteria and institutional accountability framework. The provisions of the medium-term debt management strategy that public capital spending be financed only from concessional sources should be reinforced. The changes to the FRL should be carefully prepared to allow sufficient time for fully-consistent implementation.

8. Extensive “second-generation” reforms should anchor improvements in the spending structure and implementation capacity in the following areas.

Public service and wage bill. The pace of implementation of the 2017-19 Public Management Reform Strategy has been slower than anticipated.Functional reviews, development of performance indicators, and payroll audits of ministries should be accelerated. Given the delays in these reforms, prudent wage setting parameters should be agreed for the new 2020-22 bargaining cycle.

Public investment management. The new institutional structure for coordinating capital projects that was created in early-2019 has yet to be tested. In any case, planning and implementation of public investment projects should be improved across the board, through better screening and design of projects, enhanced project management capacity, fuller information on inventory and valuation of public assets, continued improvements in public procurement, and more rigorous project prioritization criteria.

Public enterprises. The oversight committee for advising SOE operations should be re-activated and progress in adjusting tariffs to reflect cost recovery and investment needs should be followed through in the water sector and implemented in other sectors.

Social assistance. Social protection programs should be strengthened and consolidated around the Support for Education, Empowerment, and Development (SEED) program.

Pensions. The immediate costs of public pensions and health care initiatives should be contained and spillovers for increases in future spending limited through parametric reforms. The reforms to raise social security contribution rates initially from 9 to 11 percent and gradually increase general retirement age from 60 to 65 should be followed through as part of a package of measures to contain the costs of aging as well as insure the viability of the national insurance scheme and sustainability of pension benefits.

Other policies

9. Financial sector policies need to monitor potential imbalances to solidify the sector’s contribution to growth. In the banking sector, the impact on competition and corresponding banking relationships from the envisaged sale of Scotiabank should be analyzed and monitored. The rapid expansion of lending by credit unions should be matched by strengthening their oversight, data provision, and capital buffers. Growing property markets and proliferation of non-bank financial intermediaries raise the need for a full assessment of risks, including by monitoring systemic financial institutions, analyzing interconnectedness, and collecting better property market data. New accounting (IFRS9) and bank valuation and provisioning standards call for careful implementation strategies. The capacity of GARFIN and its coordination with ECCB and ECCU’s peer regulators should be further strengthened, with a view to continually harmonizing oversight of non-banks. This is particularly important for the insurance sector, which has extensive cross-border linkages. Strict compliance with AML/CFT standards and due diligence requirements should help to forcefully pre-empt any related concerns, as well as risks to correspondent banking relationships.

10. Improving the business environment and labor market institutions should help make private sector growth more broad-based, resilient, and job-intensive. Grenada’s Doing Business rankings continue to denote sizable gaps in the processing of construction permits, property and land registration, trading across borders, and investor protection. Ongoing efforts to close gaps through digitalization of procedures should be intensified. Further steps are needed, notably to reduce high port charges and other export/import costs and dismantle monopolies on export/import of certain products. Recent progress in promoting links between tourism and other sectors (agriculture) should be further enhanced and expanded by improving conditions for medical, sports, and educational tourism. The operationalization of the public utilities regulatory commission should be used as an opportunity to unlock investment in renewables. Improved labor market institutions are needed to match job opportunities with Grenada’s still-young labor force. Upgrading education, existing training programs, and employment matching services (through well-functioning central depository of labor market data) should help tap this potential.

11. Grenada could benefit from integrated strategies that leverage further improvements in operational planning, statistics, governance, and implementation capacity. Grenada’s forthcoming 2020-35 development plan should be supported by successor medium-term plans to operationalize progress, secure financing, and ensure implementation. A national Disaster Resilience Strategy could target comprehensive improvements in resilient infrastructure, financial protection, and post-disaster response. The strategy could act as a platform for coordinated action and support from development partners. All these plans should rely on the development of strong monitoring and evaluation systems and improved statistics, with the overdue update of social data being essential to the design of inclusive growth policies. These steps require improved economic governance and better coordination between all government’s agencies.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: RANDA ELNAGAR

PHONE: +1 202 623-7100EMAIL: MEDIA@IMF.ORG

Antigua

zoomIllustration. Source: Pxhere under CC0 Creative Commons

Cruise port operator Global Ports Holding (GPH) has reached an Antigua & Barbuda partnership agreement with Royal Caribbean Cruises.

GPH (Antigua) Ltd, a wholly owned subsidiary of Global Ports Holding, was recently awarded an exclusive 30-year concession in respect of the cruise port facilities at St John’s Port in Antigua and Barbuda and Falmouth Harbour and Barbuda Island.

Under the partnership deal, GPH will operate and manage the cruise port facilities, with both parties investing in the completion of the new pier, which will allow the port to handle Oasis-class ships and a material upgrade of the current and new retail and F&B facilities.

full financial closure, including the final terms of the partnership agreement and commencement of the concession, is expected to occur before the end of July 2019.

Bunker One Expands to Caribbean

zoomIllustration. Source: Pxhere under CC0 Creative Commons Marine fuel supplier Bunker

Bunker One expanded its offshore US Gulf and Caribbean fleet with bunker tanker Waltz.

The company will commence operations in Freeport, the Bahamas, from June 1.

Waltz will provide refueling options to vessels sailing outbound from the US Gulf to Europe, longhaul markets in Asia and elsewhere.

Supplying fuel at outer anchorage and Freeport Offshore, the 2008-built tanker will join the company’s bunker tanker Barbarica, which operates in the US Gulf. Equipped with twin engines and rudder propellers, Waltz will carry out major oil vetting and approvals with a capacity of 750 cubic meters/hour.

The expansion came ahead of the industry-wide demands presented by the transition to IMO 2020 and the global sulphur cap on marine fuels.

“The continued growth of our physical supply platform will allow our customers flexibility and choice in their fuel purchasing requirements as we enter 2020, creating efficient ‘bunkers only’ port calls,”Georgia Kounalakis, Managing Director, Bunker One (Gulf of Mexico & Caribs), said.

CANARI Launches SDG Platform for Caribbean Civil Society

The Caribbean Natural Resources Institute launched an online space to connect people and organizations with an interest in or information on the role of Caribbean civil society in implementing the SDGs.

CSOs can showcase stories related to their experiences in advocating for or implementing each of the 17 SDGs.

CSOs can also use the Platform as a networking forum.

The Caribbean Natural Resources Institute launched an online space to connect people and organizations with an interest in or information on the role of Caribbean civil society in implementing the SDGs.

7 May 2019: The Caribbean Natural Resources Institute (CANARI) launched a knowledge platform to enhance civil society contributions to the SDGs. The ‘Caribbean Civil Society SDGs Knowledge Platform’ addresses implementation, monitoring and review of the 17 Goals. The platform highlights funding opportunities for civil society organizations to attend meetings, among other tools and resources.

The Platform is an online space to connect people and organizations with an interest in or information on the role of Caribbean civil society in implementing the 2030 Agenda for Sustainable Development and the SDGs. Users can click on icons of each SDGs to view relevant action by Caribbean civil society organizations (CSOs). For example, on SDG 16 (peace, justice and strong institutions), news stories highlight an advocacy paper on improving the legal, fiscal and funding frameworks for civil society networks in Trinidad and Tobago, and share a case study on enhancing civil society’s contribution to governance and development in Trinidad and Tobago.

The Platform enables CSOs to showcase their own stories of their experiences in advocating for or implementing the SDGs through case studies, videos and photos, thus enhancing their capacity, voice and visibility in regional and national SDG actions and policies. CSOs can also use the Platform as a networking forum to exchange ideas and share lessons learned. The Platform also features a calendar of SDG-related events as well as SDG-related opportunities, such as funding for CSOs to attend meetings.

CANARI aims to promote and facilitate equitable participation and effective collaboration in the natural resources management critical for development in the Caribbean islands, including through supporting efforts to achieve the SDGs. CANARI created the Platform as part of project supported by the EU. [Caribbean Civil Society SDGs Knowledge Platform] [Video Introduction to the Platform] <info@canari.org>

Green Fund underutilised

Senior Technical Officer, Caribbean Natural Resources Institute, Anna Cadiz-Hadeed. PHOTO BY COREY CONNELLY

THE Green Fund is vastly underutilised. This is the contention of Senior Technical Officer, Caribbean Natural Resources Institute (CANARI), Anna Cadiz-Hadeed at the recent Tobago Environmental Partnership Conference.

Her presentation assessed the contributions of civil society organisations in fulfilling the objectives of the Multilateral Environmental Agreements (MEAs) to which TT is a signatory.

Cadiz-Hadeed, a consultant with the Ministry of Planning and Development, revealed there is over $6 billion in the Green Fund, according to the latest Auditor General’s report in September 2018. Over $373 million was allocated to 23 projects and 77 per cent of the $373 million went to state agencies.

Over 93 per cent of the Green Fund has not been utilised. So there is a need to try to support the civil society more.

Cadiz-Hadeed, who has over ten years of experience in sustainable development and participatory natural resource management, said her assessment revealed there is no money to fund the Green Fund’s website and it also does not have a Facebook page.

“When we ask why the Green Fund does not have a website, the response is that they don’t have the financial resources. So, the unit is under-resourced.” Out of the 24 eligible staff positions within the fund, only eight are currently filled.

“That is a huge human resource gap there. So, out of the $6 billion that sits within the Green Fund right now, none of that money goes towards the management of the fund.” Her assessment revealed there is a need to increase the number and quality of applications groups and organisations.

“Why aren’t more projects being funded?” She said respondents also found the application process to be onerous and difficult to complete. There is no legally-stipulated time frame to review applications. “In talking to at least 100 CSOs in TT, they said they submitted applications that have been stuck in the system. Fifty-three said they were not sure at what stage their application was at.”