Exxon Mobil

Suriname Just Became Significant To The Future

Dec. 07, 2023 Seeking Alpha

The Petronas discovery in Suriname has the potential to double the basin development projects available for Exxon Mobil Corporation. Suriname is supportive of the oil and gas industry and has no active border disputes.

Exxon Mobil and its partners can develop multiple FPSO projects simultaneously as needed. A second partnership discovery makes it very possible that basin production growth will become significant to Exxon Mobil.

The market is seeing the value of discoveries in Suriname and Guyana because there is cash flow from operating FPSOs in Guyana. Exxon Mobil Corporation has been developing the Guyana discoveries for some time. That is likely to continue as very strong allies want Guyana just as it is now.

Petronas appears to have found enough oil, partnered with Exxon Mobil to put Suriname up the priority list for the foreseeable future. Together, these two countries represent a lot of growth potential, even for a giant like Exxon Mobil. It will take a couple of years for the cash to begin flowing but once it does, it is likely to be very significant to the partners.

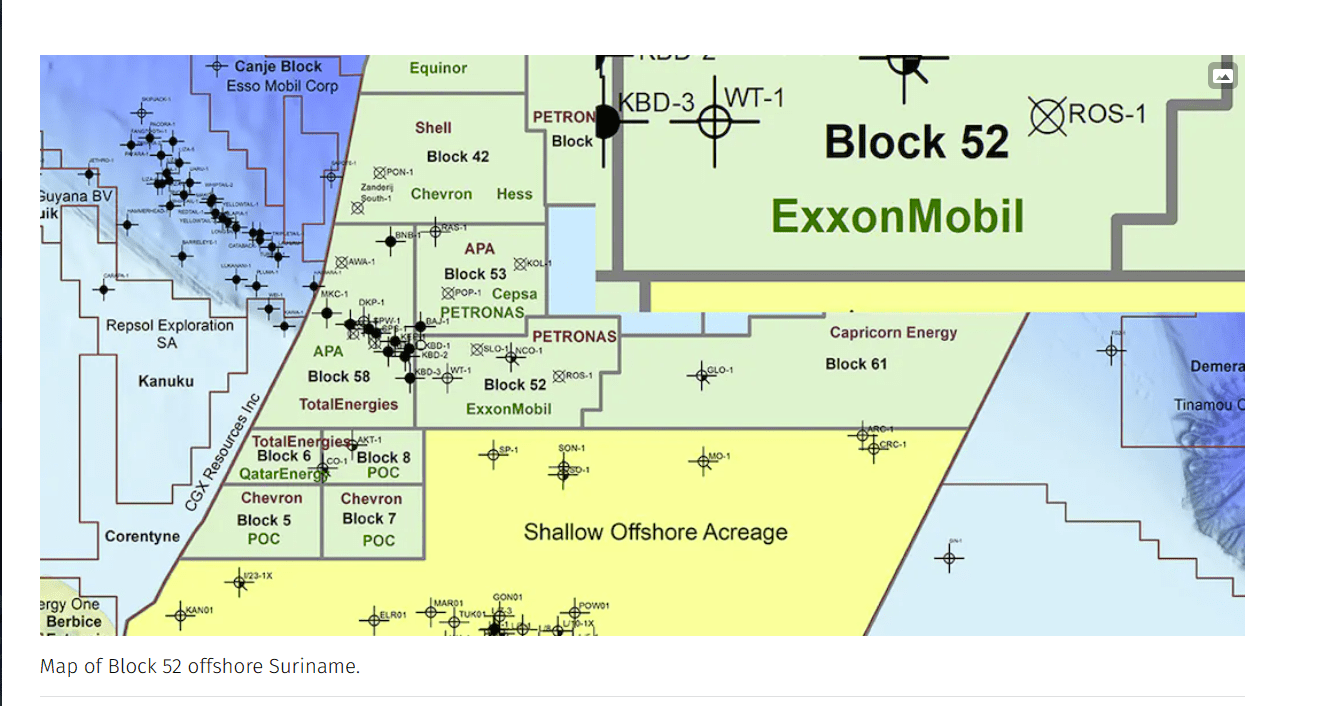

Suriname

This former Dutch colony, now independent, is supportive of the petroleum industry because it will be generating foreign currency for the government to use in its budget. Unlike Guyana, there is little or no active border disputes. Therefore, oil and gas development will be far more unfettered than might be the case in Guyana.In early November, Petronas, the operator of the partnership, announced a major discovery in block 52 of Suriname, of which Exxon Mobil is a 50% participant.

Exxon Mobil In Partnership with Petronas Discovers Oil In Suriname – Exxon

Exxon

Petronas is a very large state-owned Malaysian company with several public subsidiaries, responsible for a fair amount of government income. Both companies in this partnership, Petronas and Exxon Mobil bring experience and resources “to the table.”

What this discovery means for shareholders of Exxon Mobil is that the discoveries very likely will extend the Guyana oil fields into Suriname for one giant project (split between the two countries appropriately).

More wells need to be drilled, but like Guyana, there are a lot of wells finding oil and not too many dry holes to the current trend. There appears to be a lot of upside potential with multiple FPSOs producing that needs to be further de-risked in the future. As with any projection, there are the usual offshore upstream risks to reaching that final production goal.

Many investors stated that the current pace of development in Guyana was not all that significant to a company like Exxon Mobil. As more lease areas discover oil, there will be multiple development projects that will in total be significant to Exxon Mobil. This discovery is probably the most visible step in that development to shareholders because the discovery is clearly on another lease that appears to have significant upside potential.

With any discovery, dry holes can be encountered “tomorrow” with no more successes in sight. While that result appears to be a minimal risk now, it is worth keeping in mind because at some point this basin will have outer limits.

The Market

The market is hoping for a giant extension that can produce results similar to what is seen in Guyana:

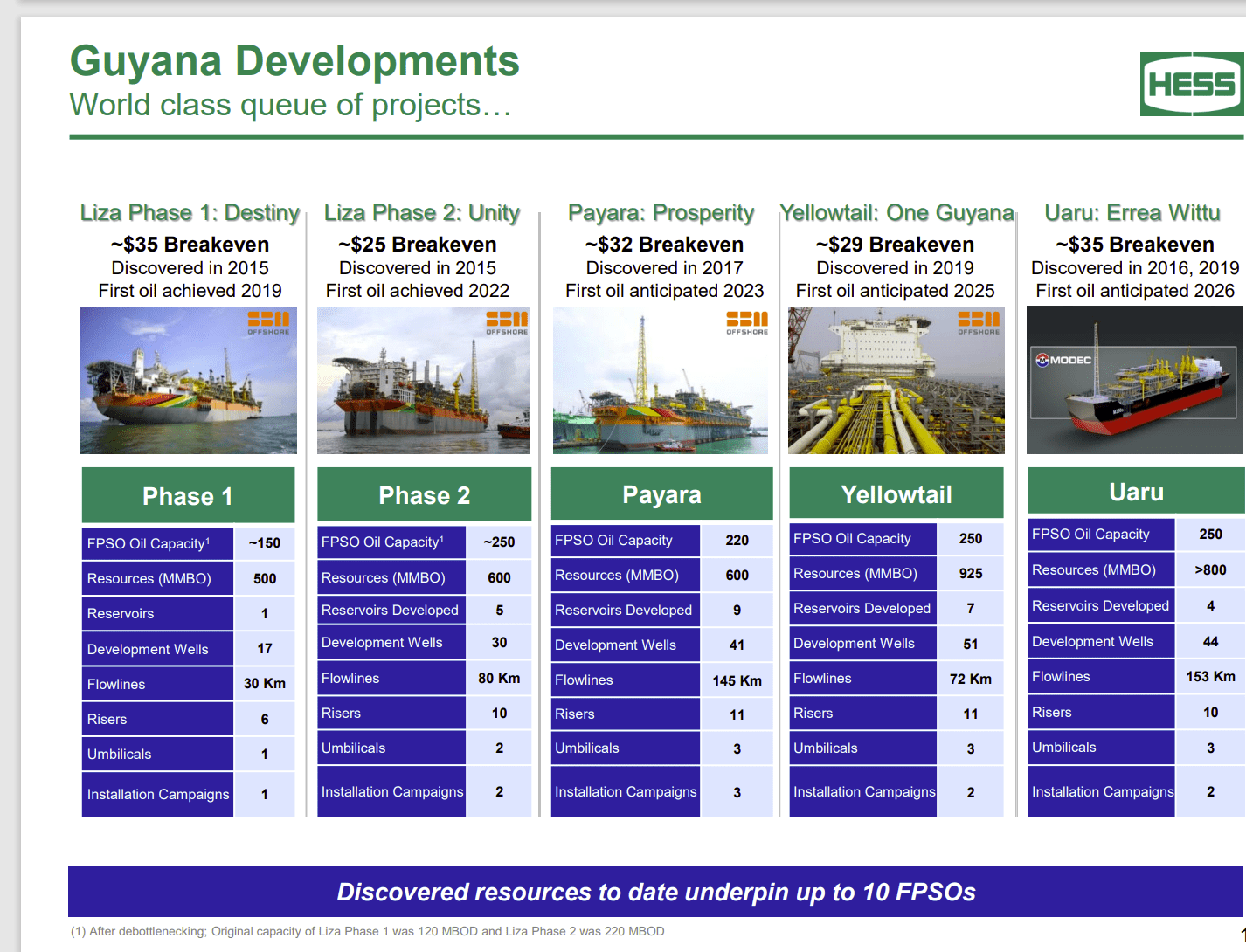

Hess Corporation Description Of Approved Projects And Projects Under Review

(Hess Corporation Corporate Presentation September 2023)

Exxon Mobil is the operator in Guyana. Because the Guyana project is a few years ahead of the discovery in Suriname, there is now some industry nearby that will help facilitate the development of the oil industry in Suriname. Exxon Mobil had to begin “from scratch.” Now a discovery that might not have been commercial is more likely to be commercial with existing production nearby.

If the Guyana business does not help the situation, then the discovery on the Total block shown above is also available. With the number of discoveries mounting in Suriname, the hope is that the industry will be every bit as large as the Guyana business appears to be.

The rumors are having a field day with this as a result. However, the “party can be over tomorrow.” That is always the risk with any discovery. It does look far more likely that the Suriname business will be a significant addition to the business in Guyana, with the possible upside potential to be equal in size.

Wall Street sees a lot of potential profits in Suriname but the profit parameters have yet to be discussed by any operator in Suriname and that discussion is likely a couple of years away. There are a lot of profitable scenarios from the discoveries in Suriname so far that are commercially viable, but may not match results in Guyana. So Wall Street could be potentially disappointed with the relative profitability of Suriname wells, even though major projects are viable. We just do not know yet.

Boundary Dispute

The Guyana border dispute is highly unlikely to affect the offshore business in Guyana, let alone the offshore business in Suriname. Guyana has too many boosters like Brazil that would likely put an end to any unfavorable outcomes quickly. The United States and Britain have a presence in Guyana.

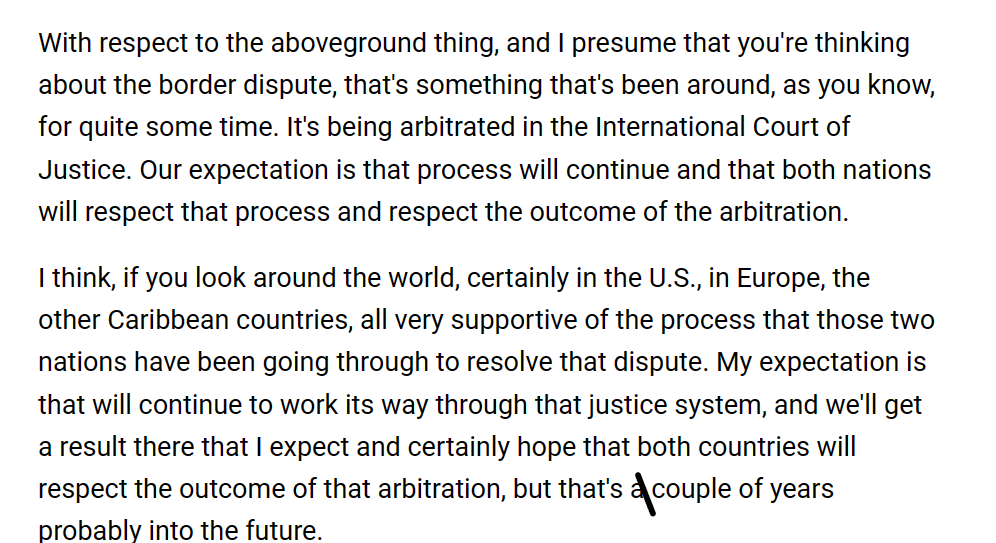

Darren Woods, CEO and Chairman, Exxon Mobil said:

Exxon Mobil CEO Darren Woods Answering A Question About the Guyana Dispute During the 2023 Plan Update Presentation

It would be a very small chance that Venezuela would gain control of the industry in Guyana. Should that happen, it may set back the development of the Suriname industry but it would not prevent development of the industry.

Anytime there is existence of oil and gas infrastructure nearby, there is usually some development aid available to the next set of discoveries. So Suriname should be able to initiate production a bit faster than was the case in Guyana, where the Exxon Mobil partnership was the first.

Overall Importance

To a certain extent, this discovery diversifies the country risk for what is becoming a very large project even for Exxon Mobil. Even large companies do not want to be too dependent on any one area.

The discovery has the potential in the eyes of many to double the existing business. Exxon Mobil and its partners are more than capable of handling the startup of two or more FPSO’s at one time. The good news is that Exxon Mobil and its partners can easily handle a big project like this with large upfront costs.

The slide from the Hess presentation shows there are a lot of costs that go into a producing FPSO. There are still more costs to be done first, though, to ensure the first FPSO is even needed. While that appears to be likely to many, it is far from assured until the operator completes all the necessary due diligence.

Nonetheless, discoveries like this keep the market excitement going, now that there is cash flow from one project. For a very long time, the market paid no attention to the events in this area because no one project had any positive cash flow. Obviously, that has now changed to where the market can see at least some potential.

The more of this basin that gets developed, the more likely there will be a market reaction to later basin extension discoveries. So far, this basin has world-class low breakeven points. That great profitability could diminish closer to the basin boundaries. For now, this basin is in the “building excitement” stage, even for a company as large as Exxon Mobil.

Suriname signed three offshore PSCs

Dec. 18, 2023

Staatsolie has signed production sharing contracts for three offshore blocks offered under the Demerara Bid Round, which closed this May.

Dreamstime.com offshore_suriname View Image Gallery Courtesy TotalEnergies

View Image Gallery – Courtesy TotalEnergies totalenergies_suriname_map Offshore staff

Signing followed a series of negotiations with the designated partners.

Petronas signed PSCs for two concessions in the Demerara area of the Guyana-Suriname Basin. The company has a 100% operated interest in Block 63, covering 5,425 sq km 200 km offshore in water depths of about 1,700 m.

In Block 64 (6,262 sq km and 250 km from the shore in water depths of 1,300 m), the company will partner with QatarEnergy (both 30%) and operator TotalEnergies (40%).

Shell subsidiary BG International will operate shallower-water Block 65 (60%), in partnership with QatarEnergy (40%).

An exploration well is due to be drilled in both Block 64 and Block 65 during the initial three-year exploration phases, while in Block 63 the first exploration well will take place in the second exploration period.

If commercial oil or gas discoveries follow, Staatsolie has the right to back into up to 20% from the start of the development period.

All three PSCs are valid for 30 years.

12.18.2023

Staatsolie signs production sharing contracts for blocks 63, 64, and 65

The blocks were part of the Demerara Bid Round held from November 2022 to May 2023 and in line with Staatsolie’s strategy of bringing in as many international investors and offshore operators as possible and Suriname’s pro-business outlook.

- A Production Sharing Contract (PSC) has been signed for Block 63 with PETRONAS, who had submitted a bid for this block.

- The PSC for Block 64 was signed with the collaborating companies TotalEnergies, QatarEnergy and PETRONAS, who submitted a joint bid. TotalEnergies is in the lead in the partnership (operator) with a forty percent participation interest; QatarEnergy and PETRONAS each have a thirty percent stake.

- BG International (a subsidiary of Shell) and QatarEnergy had made a joint bid for Block 65. QatarEnergy has a forty percent participation interest; Shell has a sixty percent interest and will act as operator.

The PSCs, which are valid for thirty years, were signed by Staatsolie’s General Manager Annand Jagesar and for Block 65, the representatives of BG International and QatarEnergy, Mark Regis and Ali Abdulla Al-Mana respectively. For Block 64, the representatives of TotalEnergies, QatarEnergy and PETRONAS, Artur Nunes Da Silva, Ali Abdulla Al-Mana and Zamri Baseri, respectively, signed. For Block 63 it was Zamri Baseri from PETRONAS. The signing took place in the presence of the Minister of Natural Resources, David Abiamofo.

Guyana-Suriname Basin

CGX Energy and Frontera Energy

04 Dec 2023

CGX Energy and Frontera Energy, joint venture partners in the Petroleum Prospecting License for the Corentyne block offshore Guyana, announced today that on December, 11, 2023, at 10:00 am ET, senior operational and technical team members will host a virtual informational presentation on the Guyana-Suriname basin, the Corentyne block and the Integrated Well Results.

Participants are encouraged to submit questions in advance to: info@cgxenergy.com or ir@fronteraenergy.ca. Questions may also be submitted during the informational presentation. The Joint Venture cordially invites all shareholders, stakeholders, investors, and media to attend the virtual presentation.

To join the presentation, visit:

Source: Frontera Energy

Saipem awarded subsea work for Whiptail, Raia

Nov. 29, 2023

Saipem has secured two contracts for major deepwater projects offshore Guyana and Brazil, with a combined valued of about $1.9 billion.

Courtesy

Saipem Constellation

Offshore staff

MILAN, Italy — Saipem has secured two contracts for major deepwater projects offshore Guyana and Brazil, with a combined valued of about $1.9 billion.

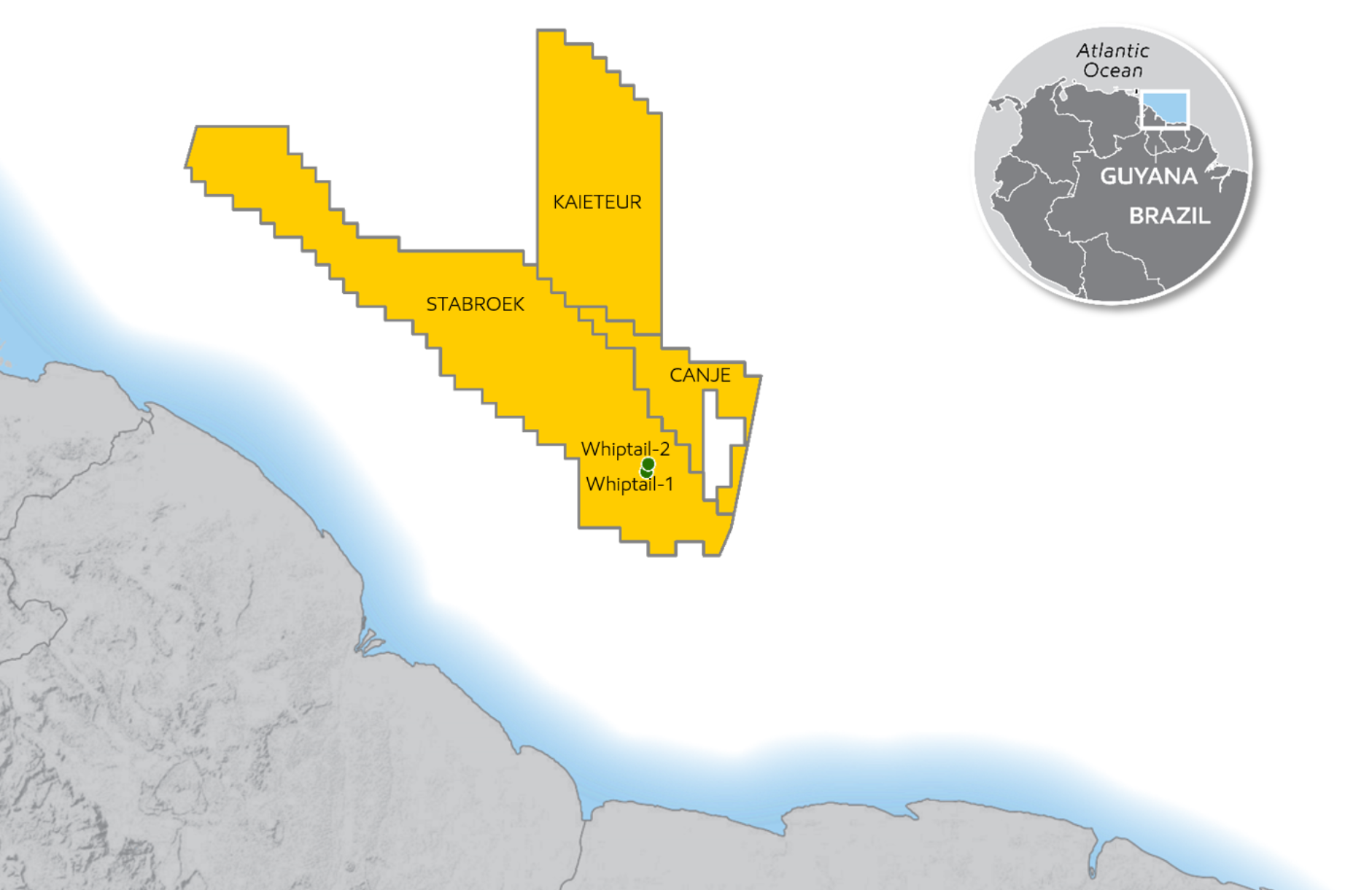

ExxonMobil Guyana has asked the company to design, fabricate and install subsea structures, risers, flowlines and umbilicals for the Whiptail oilfield development in the Stabroek Block offshore Guyana, in about 2,000 m water depth.

Saipem will deploy the FDS2, Constellation and Castorone vessels for the offshore installations, and perform fabrication at its offshore construction facility close to Georgetown.

Pending approvals from the government for the development and FID by the partners, Saipem will focus for the time being on detailed engineering and procurement.

Equinor has contracted the company to provide pipeline services for its presalt gas/condensate Raia Field development in the Campos Basin, 200 km offshore Rio de Janeiro.

The work scope covers transportation and installation of the subsea gas export line and associated equipment in water depths of about 2,900 m and horizontal drilling for the shore approach. Castorone will perform the installation.

Raia’s gas will be transported through pipelines to a new reception facility at Cabiúnas, Macaé.

11.29.2023

ExxonMobil, Equinor award Saipem two offshore contracts in Guyana, Brazil

November 29, 2023

(WO) – Saipem has been awarded two offshore contracts, one in Guyana and the other in Brazil, worth approximately $1.9 billion.

Source: ExxonMobil

Source: ExxonMobil

The first contract has been awarded by ExxonMobil’s subsidiary ExxonMobil Guyana Limited for the proposed Whiptail oil field development located in the Stabroek block offshore Guyana, at a water depth of approximately 2,000 m. Saipem’s scope of work includes the design, fabrication and installation of subsea structures, risers, flowlines, and umbilicals for a large subsea production facility.

Saipem will perform operations using its state-of-the art vessels FDS2, Constellation, and Castorone, and will deploy as a key fabrication site for its execution model, Saipem’s Guyana Offshore Construction Facility, located at the Port of Georgetown, enhancing a sustainable steady growth in the country.

The second contract has been awarded by Equinor for the Raia project, the development of a pre-salt gas and condensate field in the Campos basin, located about 200 km offshore the state of Rio de Janeiro in Brazil.

Saipem’s scope of work encompasses the offshore transport and installation of a subsea gas export line and associated equipment in water depths of around 2,900 m, as well as the horizontal drilling activities for the shore approach. Saipem will deploy its state-of-the-art pipelaying vessel Castorone for the installation works.

With this project, Saipem will contribute to the realization of one of the most important gas development projects in Brazil, which could represent 15% of the total domestic demand of the country. The extracted gas will be transported through pipelines installed by Saipem for approximately 200 km from the field to a gas receiving facility to be built in Cabiúnas, in the city of Macaé in the State of Rio de Janeiro.

US, UK aid Guyana in boundary dispute

7 DECEMBER 2023

USA and UK allies sent clear messages of support for Guyana, amid Venezuela’s threat to annex the Essequibo region.

“Secretary of State Antony J Blinken spoke with Guyanese president Dr Mohamed Irfaan Ali to reaffirm the US’ unwavering support for Guyana’s sovereignty,”

Blinken reiterated the US call for a peaceful resolution to the dispute and for all parties to respect the 1899 arbitral award setting the Venezuela/Guyana border, unless/until the parties reach a new agreement or a competent legal body decides otherwise.

“Secretary Blinken and President Ali noted the International Court of Justice order issued on December 1, which called for parties to refrain from any action that might aggravate or extend the dispute.

“The secretary reiterated that the US looks forward to working closely with Guyana once it assumes its non-permanent seat on the UN Security Council in January 2024. The two leaders concluded the call by agreeing upon the importance of maintaining a peaceful and democratic Western Hemisphere.”

The UK Foreign, Commonwealth and Development Office condemned Venezuela’s intended grab for Guyana’s Essequibo region.

“The UK is concerned by the recent steps taken by Venezuela, with respect to the Essequibo region of Guyana. We believe this is unjustified and should cease. We are clear that the border was settled in 1899 through international arbitration.”

The UK was the colonial power ruling Guyana, known as British Guiana before independence in 1966

UK High Commissioner to TT Harriet Cross said “The UK is clear that the border was settled in 1899 through international arbitration and we continue to support this decision. We urge the parties to resolve this issue peacefully.”

British Foreign Secretary David Cameron emphasised the UK position at a news conference with Blinken in Washington, DC, which focused on the wars in Ukraine and Gaza. Cameron said the two diplomats had discussed the Essequibo situation.

“These borders were settled in 1899. I see absolutely no case for unilateral action by Venezuela. It should cease. It is wrong.”

He was delighted by the earlier announcement by the US on the threat.

“I hope to be having some telephone calls later on with the President of Guyana and others in the region to make sure that this very retrograde step that has been taken does not lead any further.”

US and UK pledged support after Venezuelan President Nicolas Maduro announced several steps to take control of the Essequibo, declaring it part of Venezuela in a new map, naming a military governor, telling Venezuelan companies to take charge of oil exploration there and promising a census of locals with Venezuelan ID cards.

Claiming a ten million turnout in the referendum, which global media criticised as poorly attended, Maduro ordered the National Assembly to draft a law to establish Guayana Esequiba as Venezuela’s 24th state, portrayed as part of his new map of an enlarged Venezuela. Ahead of the referendum, Venezuelan troops were reportedly clearing jungle to build an airstrip near the Venezuela/Guyana border. He vowed to administer Essequibo from the Venezuelan town of Tumeremo.

The US military’s Southern Command said it would fly over Guyana as a security partner, in a statement posted at the US Embassy in Guyana.

“In collaboration with the Guyana Defence Force (GDF), the US Southern Command will conduct flight operations within Guyana on December 7. This exercise builds upon routine engagement and operations to enhance security partnership between the United States and Guyana, and to strengthen regional cooperation.”

The US Southern Command promised to continue collaboration with the GDF for disaster preparedness, aerial and maritime security and countering transnational criminal organisations.

“The US will continue its commitment as Guyana’s trusted security partner and promoting regional co-operation and interoperability.”

Colombia and Brazil have significant military capability in the area, as Venezuela’s neighbours and have been training with the US Southern Command.

The US Southern Command hosted a visit by head of the Colombian Military Forces (Fuerzas Militares de Colombia), Gen Helder Giraldo, to the command’s headquarters in Florida. He discussed US-Colombia defence co-operation with senior leaders. Strengthening our partnership with Colombia, Giraldo and command vice admiral Alvin Holsey showed a document, described as an engagement and co-operation framework to strengthen bi-lateral cooperation in national defence and security.

The command’s website showed camouflaged US and Brazilian troops on a training exercise from November 6-16 in Belem, Macapa, and Oiapoque in Brazil. Titled Southern Vanguard 2024, the exercise involved 300 US Army and National Guard soldiers training alongside over 1,000 Brazilian soldiers.

Reuters reported Brazil’s Ministry of Defence as saying its military was reinforcing its northern border due to rising tensions between Venezuela and Guyana after the referendum to annex the Essequibo.

“The Brazilian army is moving armoured vehicles and more troops to Boa Vista, the capital of Roraima state that borders both Venezuela and Guyana.”

Venezuela Minister of Defence Vladimir Padrino publicly introduced Maj Gen Alexis Rodriguez Cabello and another army official as being named administrator of Guayana Esequiba. clenching their fists in the air the trio declared in Spanish that the sun in Venezuela rises in the Esequiba.

Telesur reported Padrino’s speech.

“Through collaborative work, the sole authority and the Bolivarian National Armed Forces will deploy all their logistical and human potential in the sector. We are already co-ordinating to promptly fulfil the mandate of the people with all the social policies towards the territory of Guayana Esequiba. There is no rest, no break, and we work for our Esequibo.”

Brazilian President Luiz Inacio da Silva told the Mercosur summit in Rio de Janeiro of his growing concern at the Essequibo row. “If there’s one thing we don’t want here in South America it’s war. We don’t need conflict. We need to build peace.”

Guyana, Venezuela agree not to escalate conflict

December 15, 2023

Venezuela and Guyana agreed not to use force to settle a border dispute over the oil-rich Essequibo region. The territorial dispute dates back to the 19th century. After their leaders met on the island of St. Vincent ,

Guyana and Venezuela have agreed to avoid any escalation of conflict over the disputed border area. In a joint statement the two countries pledged not to resort to violence to settle a long-simmering dispute over the oil-rich Essequibo region.

Guyana and Venezuela “directly or indirectly will not threaten or use force against one another in any circumstances, including those consequential to any existing controversies between the two states.”

Disputes over the 160,000-square-kilometer (62,000-square-mile) Essequibo region go back decades but Venezuela renewed its claim, including to offshore areas, in recent years after major oil and gas discoveries.

Venezuela revived its territorial claim after US energy conglomerate ExxonMobil discovered a significant amount of oil offshore Essequibo in 2015, transforming Guyana into the world’s fourth-largest offshore oil producer.

Tensions rose after Venezuela staged a non-binding referendum over the claim, to stoke nationalist fervour and distract from calls for free and fair elections.

Official results state over 95% of voters approved “the creation of the new Venezuelan state of Guayana Esequiba “ in the territory of Essequibo and its “incorporation into the map of Venezuelan territory”, thus declaring Venezuela the rightful owner, Essequibo residents were not polled in the ballot.

Elvis Amoroso, head of the National Electoral Council said that 10.5m votes had been cast – “historic” ifor an electorate of 20.7million. Henrique Capriles suggested that 10.5m votes only equated to two million voters. Opposition media reported quiet polling stations, casting doubt on a high turn-out. .

Maduro then started legal maneuvers to create a Venezuelan province in Essequibo. In an unprecedented gerrymander, he ordered state oil company PDVSA to to establish a base in disputed Essequibo and issue licenses for extracting crude.

The dispute dates back to the 19th century.

Venezuela claims Essequibo is part of its territory because the region was part of its boundaries during the Spanish colonial era. International arbitrators in 1899 handed Essequibo to former British and Dutch colony Guyana, which used this decision as its justification for control of the region.

Litigation at the ICJ seeking a decision over the border dispute is pending. The ICJ had appealed to Venezuela to refrain from taking action that could influence the case on Essequibo — which Maduro ignored, pressing ahead with his non-binding referendum .

dh/sms (AFP, Reuters)

CDB Pilots Monitoring, Reporting, and Verification System for Tracking Climate Finance for Caribbean Countries

DUBAI, United Arab Emirates – December 5, 2023

The Caribbean Development Bank (CDB) is spearheading the development of a regional online Monitoring, Reporting, and Verification (MRV) system for climate finance tracking. Once fully operationalised the system will enable CDB’s Borrowing Member Countries (BMCs) to improve tracking and reporting of finance flows from various sources for climate change related actions.

Developed through a grant from the Green Climate Fund Readiness and Preeparatory Programme, the MRV mechanism was piloted in Belize, Haiti, Jamaica, and St. Kitts and Nevis. The readiness project created a platform that permits the central management of source funding flows, facilitates greater sharing of information to reduce duplication among donors, and enables more efficient use of finances. It also delivered an operational manual and guidance notes with processes and procedures for the MRV tracking system, guidelines with a methodology for classifying climate finance, and training for persons from the participating countries.

During a panel discussion on December 4, 2023, at the 28th Annual United Nations Climate Change Conference (COP28) currently underway in Dubai, United Arab Emirates, CDB and senior representatives from the Government of Jamaica, and the Caribbean Community Climate Change Centre (CCCCC) discussed the results of the pilot. The dialogue focused on the need for the Region to adopt a credible MRV system which can improve understanding and management of financial flows from public, private, national, and international sources for climate change mitigation and adaption. The dialogue also shed light on how MRVs help shape climate change policy and improve how climate change data is captured.

Mr. Omar Alcock, Principal Director (Actg.), Climate Change Division, Ministry of Economic Growth and Job Creation, said a fully functioning MRV system helps countries identify existing gaps.

“When we have a framework that is clear on what the requirements are, we are able to identify where we can’t meet these requirements and then put things in place to improve the reporting that is required under the agreement,” Mr. Alcock said.

The MRV system should also provide regional decision-makers with greater visibility of the climate fund’s portfolio and necessary information to aid the conceptualisation and development of initiatives to increase resilience to climate change impacts.

CDB’s Division Chief, Environmental Sustainability, Valerie Isaac, emphasised the Bank’s readiness to work with its regional and international partners to standardise the MRV system across BMCs.

“It is important for the countries that participated in the readiness project to engage with their other country partners, sharing experiences and encouraging the establishment of national systems that are credible and transparent including the understanding of the benefits of a regional and collaborative approach to tracking climate finance flows,” she said.

Executive Director of the CCCCC, Dr. Colin Young, noted that it was important to have alignment on what constitutes climate finance as this will assist countries in capturing and reporting data necessary to achieve their targets, while sustaining trust with financing partners.

“For an MRV Framework to be most effective there should be an understanding between the donors and recipient countries about what constitutes climate finance. This is essential for trust and transparency,” Dr. Young said.

The development of an MRV system for use by CDB’s BMCs aligns with the Paris Agreement which underlines the need for climate finance MRV systems and transparency as core aspects of the effective implementation of countries National Determined Contributions. Prior to the GCF Readiness project no MRV system, which captures the portfolio investment details from different climate funds and donors, existed for the Caribbean region.

IDB

A new action plan has been introduced to bolster collaboration and coordination among the organisations in the Caribbean region as a whole.

DUBAI, United Arab Emirates – December 4, 2023

The Inter-American Development Bank (IDB), IDB Invest, and the Caribbean Development Bank (CDB) signed an Addendum to the 2020 Mutual Cooperation Agreement yesterday at the 28th Annual United Nations Climate Change Conference (COP28) currently underway in Dubai, United Arab Emirates.

This new action plan strengthens activities aimed at addressing climate change resilient –physical and digital- infrastructure, project preparation and execution in priority areas, private sector productivity and development, and exposure exchange agreements and other financial products, among others.

Since 1977, the IDB and the CDB have collaborated on areas of common interest. In 2017, both institutions formalized their collaboration through a Memorandum of Understanding (MoU) to support Sustainable Development Goals (SDGs) in the Caribbean. In 2020, they further bolstered collaboration through a Mutual Agreement, focusing on co-financing projects, providing financial and advisory services, promoting partnerships, and fostering knowledge exchange.

The Addendum signed today, along with the new Action Plan, complements the existing Mutual Cooperation Agreement. It emphasized collaborative actions and partnership activities aimed at addressing upcoming development challenges in the Caribbean aligned with IDB’s “One Caribbean”, a new regional flagship program that aims to promote the sustainable development of the Caribbean with a sharpened focus on high-impact interventions. The “One Caribbean” program includes four key pillars: climate adaptation, disaster risk management and resilience; citizen and business security; sustainable development through private sector engagement; and food security.

Ilan Goldfajn, President of the IDB, said: “The IDB, IDB Invest and the CDB reinforce today their commitment to identifying synergies and enhancing collaboration for the benefit of the entire Caribbean. Our mutual priorities include boosting regional infrastructure resilience to climate change both physical and digital, enhancing mutual project preparation and execution capacity in priority areas, promoting private sector productivity, growth and development, and exploring financial solutions to extend the organizations’ reach and impact in the region. This new chapter with the CDB is aligned and reinforces IDB’s new regional program “One Caribbean”.

James Scriven, CEO of IDB Invest, said: “No other region has been more affected by climate change than the Caribbean, and bolstering our relationship with the CDB will allow us to support sustainable projects for the local ecosystems, economies and communities.”

Dr. Hyginus ‘Gene’ Leon, President of the CDB, said: “The Addendum to the existing Agreement includes a 3-year action plan for strengthening the resiliency ecosystem including, capacity building on project execution, joint research and knowledge sharing activities and co-financing for private sector growth. These initiatives are critical flagstones along the path to resilient prosperity. We look forward to the enhancing of this partnership with IDB as we could not deliver on these programmes on our own.”

CDB COP 28 News Update

PRESS RELEASE

December 1, 2023

Green Climate Fund approves grant to support further development of the CDB-managed Blue Co Caribbean Umbrella Coordination Programme

BRIDGETOWN, Barbados: The Green Climate Fund (GCF) has approved a grant for further development of the Blue Co Caribbean Umbrella Coordination Programme which aims to scale up financing and investment to support the transition to a low-emission, climate-resilient blue economy across the Region.

The Project Preparation Facility grant, which was announced today at the 28th Annual United Nations Climate Change Conference (COP28), currently underway in Dubai, United Arab Emirates, will be managed by the Caribbean Development Bank (CDB).

The full programme, once approved, will facilitate the development and updating of blue economy frameworks at the national and regional levels, the establishment of a regional mechanism to support a more coordinated response to the Caribbean’s blue economy needs, and directly finance the implementation of innovative projects that help scale up private sector investment in a resilient and sustainable blue economy. More than 56,000 people across the Region will benefit directly from the initiative and an additional 600,000 will be indirect beneficiaries.

At the launch event, President of the CDB, Mr. Hyginus Gene Leon, said the Umbrella Coordination Programme was timely because while the Caribbean Sea has an estimated economic value of USD407 billion per year and supports multiple important marine ecosystems such as coral reefs, mangroves, and seagrasses, more than 700 species are under threat.

“Despite widespread reliance on the ocean for livelihoods, recreation, health, well-being, and culture by the Caribbean’s 19 million people, sustainable development goal 14 which speaks to life below water, is the least funded of all 17 SDGs,” Dr. Leon said.

He added, “Decisive action is now critical because the Caribbean already faces multiple climate-related threats such as tropical storms, flooding, droughts, sea level rise, increasing ocean temperatures, and climate change-induced ocean acidification and now the multiple global crises of the last two years have exacerbated our vulnerability.”

Executive Director of the GCF, Ms. Mafalda Duarte said, “The Caribbean needs approximately $175 billion by 2030 to fortify marine biodiversity, enhance sustainable fishing practices, and bolster coastal defenses against climate change. Yet less than $10 billion has been invested in these critical areas since 2015.” She added, “The Green Climate Fund is ready to be a partner for transformative action. We are the world’s largest climate fund, and we are focusing efforts on coastal and marine areas.”

H.E. Philip Davis, Prime Minister of The Bahamas said, “I applaud the Green Climate Fund for its efforts to support the developing world in creating climate resilient pathways to a sustainable future”. He added, “Through this platform, Caribbean nations will be able to strengthen their blue economy frameworks and develop projects that can be replicated and scaled across the Region.”

H.E. Roosevelt Skerrit, Prime Minister of Dominica expressed gratitude for the input of the GCF and other partners “I am very grateful for the advocacy which the Green Climate Fund is advancing on our behalf and for the Blue Co Caribbean Umbrella Coordinating Programme which is serving as a lifeline for us in accessing the resources to put a framework in place to benefit from the financing.”

ANSA McAL, KGL sign MoU for New, viable green energy projects

COP28, Dubai

ANSA McAL Group and Kenesjay Green Limited (KGL) – a regional leader in green energy project development – signed an MOU to accelerate development of new and commercially viable green energy regional projects .

Ministers of Caribbean states, applauded the signing, significantly during the COP28 Climate Summit session on Regional Green Hydrogen Developments in the Caribbean, supported by co-hosts in the auspicious Nationally Determined Contributions (NDC) Pavilion in the Blue Zone – Dominica, the Caribbean Climate-Smart Accelerator (CCSA) and Kenesjay Green Limited. Multilateral financing institutions and other key stakeholders witnessed the signal event.

At the signing ceremony, ANSA McAL Group CEO Anthony N. Sabga said, “I am proud of this first step taken today to partner with KGL to explore projects to harness the Caribbean’s natural resources to provide more sustainable solutions that impact the lives of the people of our region. It is our intent to bring considerable resources in people, capital and technology to support the efforts of our region in the fight for a greener future. This resonates deeply with our purpose: Inspiring Better Choices for a Better World.”

Philip Julien, founder and chairman of KGL – an affiliate of Kenesjay Systems Limited – said, “We bring our track record of project development expertise which has recently focused on bankable low carbon and green hydrogen projects in the Caribbean.

“Our collaboration in Dominica to deliver Geothermal to Green Hydrogen bears testimony to this focus. This MOU with a Caribbean corporate heavyweight like ANSA McAL is an important next step in advancing potential green projects in the region, including other geothermal-rich countries in the Caribbean.”

COP28, the United Nations’ Climate Change Conference in Dubai, United Arab Emirates, runs from November 30 to December 12 and is the world’s only multilateral decision-making forum on climate change with almost complete membership of every country.

Kenesjay Green Limited (KGL), based in Trinidad and Tobago, is an indigenous leader in the Caribbean’s energy transition, through its development of a pipeline of viable decarbonising and green project opportunities.

The company is an affiliate of Kenesjay Systems Limited, a knowledgeable resource for innovative ideas and solutions for the energy sector.

The Bahamas:

IMF

Staff Concluding Statement of the 2023 Article IV Mission

November 27, 2023

A Concluding Statement describes the preliminary findings of IMF staff at the end of an official staff visit (or ‘mission’), in most cases to a member country. Missions are undertaken as part of regular (usually annual) consultations under Article IV of the IMF’s Articles of Agreement, in the context of a request to use IMF resources (borrow from the IMF), as part of discussions of staff monitored programs, or as part of other staff monitoring of economic developments.

The authorities have consented to the publication of this statement. The views expressed in this statement are those of the IMF staff and do not necessarily represent the views of the IMF’s Executive Board. Based on the preliminary findings of this mission, staff will prepare a report that, subject to management approval, will be presented to the IMF Executive Board for discussion and decision.

Washington, DC:

The Macro Outlook

The Bahamas’ economy continued to rebound vigorously in 2022. Real GDP growth reached 14.4 percent and unemployment fell to 8.8 percent with a broad-based expansion that was especially strong for tourism. However, labor force participation, particularly among men, remained below pre-pandemic levels. In 2023, international flight and cruise arrivals rose well above their pre-pandemic levels leading to a projected 4.3 percent expansion in the year, bringing the economy back to estimates of potential output.

After peaking at 7.1 percent in July 2022, inflation has fallen steadily to 2.3 percent in July 2023, largely driven by the fall in global energy prices.

Risks to the outlook are skewed to the downside. A fall in tourism demand, due to an economic slowdown in source markets could weigh negatively on the growth outlook. Furthermore, renewed pressures on global food and oil prices could impose a burden on lower income households and put pressure on the balance of payments. Any associated fiscal measures to dampen the pass-through of global prices to the domestic economy would have to be well-targeted to mitigate further strain the fiscal position. . Finally, The Bahamas is highly exposed to risks emanating from climate change and natural disasters. In the event that risks are realized, domestic financing challenges could increase.

Creating A More Efficient and Progressive Fiscal Framework

A strong cyclical recovery in revenues and a wind down of pandemic-related spending have reduced the fiscal deficit to 4.1 percent of GDP in FY2022/23, bringing the central government debt down to 84 percent of GDP at end-June 2023.The authorities intend to reduce the deficit to 0.9 percent of GDP in 2023/24, reaching an overall surplus of 2.1 percent of GDP by FY2026/27. The bulk of this adjustment would come from a 3½ percent of GDP increase in revenue collections, largely from improvements in administration. In addition, ½ percent of GDP in additional capital spending are expected to be funded from lower current spending. This fiscal path is expected by the authorities to bring public debt to 68 percent of GDP by FY2026/27.

While the objectives of the authorities’ medium term fiscal plan are laudable, staff assesses that more policy measures will be needed to achieve this targeted adjustment. In particular, based on current policies, the fiscal deficit is expected to be 2.6 percent of GDP in 2023/24 (considerably larger than that expected in the budget). Over the medium-term, debt would fall to 78 percent of GDP by 2027/28 but gross financing needs would remain high for the next several years (at around 20 percent of GDP). Even though, under this path, debt is judged to be sustainable, a faster reduction in debt would be valuable in lessening the risk of sovereign stress and, in so doing, would be rewarded through a lower interest burden for the public debt.

Beyond reducing the fiscal deficit, a set of comprehensive tax reforms would be valuable in both raising revenues and improving progressivity. In particular, the implementation of the OECD global minimum corporate tax by trading partners provides an opportunity for The Bahamas to introduce a well-designed corporate income tax accompanied by a personal income tax on the highest earners. There is also scope to significantly rationalize existing preferences, loopholes, and exemptions in the tax system.

Efficiency gains in spending programs and improvements in the financial management of state-owned enterprises will be needed to offset some of the budgetary pressures arising from an aging population. To improve longer-run growth and strengthen social inclusion, there will be a need to reorient spending priorities toward education, healthcare, targeted social transfers and infrastructure (particularly those which will increase resilience to the effects of climate change).

Better debt management would help reduce the vulnerabilities created by The Bahamas’ high debt rollover needs. Recent reforms to strengthen the primary and secondary debt markets should help increase the liquidity of government bonds and incentivize an increase in domestic holdings of longer duration securities. In particular, the central bank continues to facilitate the issuance of T-bills by competitive auction and intends to extend this across domestic government security maturities. Further reforms to bolster these efforts can include improving investor relations and increasing the transparency and predictability of sovereign issuance plans.

Additional steps should be taken to place more binding limits on central bank financing of the fiscal deficit. The authorities have made amendments to the Central Bank Act prohibiting financing the government via the primary bond market and have also imposed a lower limit on central bank advances; however, this limit is above that of regional peers with pegged regimes. A reduction in the limit on central bank financing should be accompanied by a well-defined “escape clause” that would be triggered in exceptional circumstances (e.g., in the event of a large scale natural disaster). Repaying central bank advances, already at the ceiling, could also serve to strengthen the credibility of the exchange rate regime.

Recent welcomed amendments to the new Public Finance Management (PFM) and Public Procurement Acts will usefully strengthen the governance framework of SOEs and improve the transparency of public procurement. The publication of beneficial ownership information is now mandatory for public contracts funded by an international funding agency but should be the applicable standard for all providers that obtain public contracts. Similarly, procurement documents and audited financial statements of SOEs should be published on a regular basis. An independent process should be put in place to select members of the fiscal council. Finally, any deviations from the targets mandated in the PFM Act should be time-bound and underpinned by clear guidance on the speed at which the authorities will revert back to their goals.

Strengthening the Financial System

Protection of the exchange rate peg requires sustained preservation of international reserves. The recovery in tourism, external public sector borrowing, and the presence of long-standing capital flow management measures have supported international reserve accumulation even as domestic short-term interest rates remain well below those in the United States. However, capital flows can be sensitive to interest rate differentials, especially during periods of uncertainty or volatility. Liquidity management operations, as well as allowing interest rates to rise as needed by market conditions could be useful for mitigating these risks, reduce banks’ carrying cost of reserves and, in turn, narrow the spreads between deposit rates and rates on loans to private borrowers.

Usage of the Sand Dollar, the central bank’s digital currency, remains limited. Despite the large diffusion of electronic wallets, the Sand Dollar still represents a small, albeit growing, percentage of money in circulation. The central bank is continuing its outreach efforts to the public and has formalized the governance framework surrounding the Sand Dollar. The Bank multipronged approach to increasing Sand Dollar adoption has the potential to increase financial inclusion and increase the resilience of the payment system. Continued efforts to identify and manage cybersecurity risks and improve the security infrastructure will also bolster confidence in the Sand Dollar, and strengthen prospects for a larger circulation.

Deeper efforts are recommended to analyze, monitor, and mitigate financial stability risks stemming from crypto assets. The regulatory framework for crypto assets has been updated and the authorities have legislated an amendment to the Digital Assets and Registered Exchanges (DARE) Act to strengthen the regulation and supervision of crypto assets. Critically, this should be accompanied by the provision of more resources for onsite inspections to help identify and rectify operational deficiencies and reduce reputational risks.

Further amendments to the legislation to fully align The Bahamas’ framework for crypto assets with global standards like the Financial Stability Board’s high-level recommendations on crypto assets and the Basel Committee standards on the prudential treatment of crypto exposures are advised. Vigilance in this nascent but rapidly-evolving area of regulatory oversight will be of the essence.

The progress made by the authorities in implementing the 2019 FSAP recommendations are welcome, but some areas remain to be addressed. A separate Resolution Unit within the central bank has been established but will require adequate staffing to become fully operational. Plans are underway to establish The Bahamas Financial Stability Council (BFSC) to improve interagency coordination and information exchange among financial stability regulators. Efforts should be furthered to increase the coverage of deposit insurance for domestic banks by increasing premiums levied on banks for all deposit liabilities, while improving the Deposit Insurance Corporation’s governance and operational structure. The collection of loan-level data by supervisors would assist in identifying systemic risks and, if needed, in designing macroprudential policies.

Boosting Resilience and Growth

New avenues for climate finance have the potential to bolster fiscal and environmental sustainability. Building credible measurement, reporting and verification frameworks for climate-related projects, developing projects that have co-benefits across other Sustainable Development Goals, and partnering with established institutions in climate finance will help set high standards in assessing projects through an environmental lens. Creating a credible domestic framework for climate-related investments can help catalyze investor interest in green and blue debt instruments as well as the sale of carbon credits. Similarly, developing a domestic framework for Environmental, Social and Corporate Governance bonds (including introducing reporting standards for sustainability disclosures by companies) would help support new avenues for climate financing to Bahamian public and private sector entities.

Accelerating the transition to renewable energy will help boost private sector growth and reduce the country’s exposure to global swings in commodity prices. High and volatile energy prices and supply reliability issues are a disincentive to private investment. Accelerating solar projects and improving the national electricity company’s governance structure could help lower costs, increase the continuity of energy supply, and raise the share of renewables toward the authorities’ goal of 30 percent by 2030. Other investments in renewables—particularly roof-top solar—should be incentivized through either subsidies or tax preferences and private-public partnerships should be encouraged, especially on remote islands.

Property insurance premiums have been steadily increasing due to the high costs of reinsurance. This is leading to decreased insurance coverage which, in the event of an extreme weather event, can potentially lead to significant losses for the population and, ultimately, create large fiscal needs. Partial public funding of micro-insurance products could be expanded in combination with a public mandate to carry a minimum level of property insurance. Increased fiscal buffers will be needed to provide some relief to those that may be affected in a future disaster. Finally, the authorities could consider designing financial instruments that incentivize private self-insurance.

The government has made significant progress in the digitalization of public services and data gathering. Addressing the remaining gaps has the potential to help reduce frictions that dis-incentivize private investment as well as improve the targeting of social assistance programs.

The IMF staff team is grateful to the Bahamian authorities and other counterparts for their time, warm hospitality, and constructive discussions.

Prof Emeritus Winston Mellowes

Former chairman of the National Institute of Higher Education Research Science and Technology (NIHERST) Prof Emeritus Winston Mellowes has died.

Mellowes, who served as chairman from 2017-2020, played a pivotal role in steering the institute towards robust advancements in science, technology, engineering, and mathematics (STEM) across TT.

“Prof Mellowes was a transformational leader where his impactful tenure witnessed the infusion of a strategic vision into the institute’s plan, setting a robust course for its development. His visionary 2019 initiative to establish a strategic collaboration with Shell Trinidad and Tobago Ltd resulted in the commissioning of the Shell STREAM Programme, powered by NIHERST,” the release said.

Mellowes was awarded the 2021 Chaconia Medal (Gold) and earned a fellowship with the Caribbean Academy of Sciences (CAS).

“His contributions to the CAS, where he served as Foreign Secretary and later attained the prestigious position of president, underscored his profound impact on the scientific community.”

At UWI, Mellowes led the Department of Chemical Engineering.

He was president of the Association of Professional Engineers of TT, chairman of the Board of Engineering of TT, member of the Board of the Accreditation Council of TT, the TT Group of Professional Organisations, and the board of the UWI Credit Union.