Liberia forms O&G technology department in response to fleet registry growth

Liberia’s Offshore and Gas Technology Department head Stephen Bomgardner; Source: LISCRria’s Offshore and Gas Technology Department head Stephen Bomgardner;

Liberia’s Offshore and Gas Technology Department head Stephen Bomgardner; Source: LISCRria’s Offshore and Gas Technology Department head Stephen Bomgardner;

Liberia has established its Offshore and Gas Technology Department, renewing the registry’s focus in these sectors.

The creation of the department strengthens Liberia’s presence in the offshore and gas sectors and is a response to the registry’s growth in 2018.

Liberia, dubbed the fastest growing major open registry in both shipping and offshore, has now formalized its in-house technical and commercial capabilities in the offshore sector with the formal creation of the Department at its U.S. headquarters, comprising members from its global network of industry experts.

This Offshore and Gas Technology Department is headed by Captain Stephen Bomgardner, a consultant with offshore experience as a Master and OIM of drillships. The department includes technical, safety, and registrations personnel and capabilities.

Alfonso Castillero, CCO of the Liberian International Ship & Corporate Registry (LISCR) and the US-based manager of the Liberian Registry, said: “The reasons for establishing this department are twofold – to service the exacting requirements of our existing offshore clients, and to keep up with the growth we have experienced in the offshore sector with so much demand for the flagging of drillships, rigs, and FPSOs in our registry.”

Liberian-flag fleet growth has reached 9.8% so far this year, far surpassing all other flag states.

Source: LISCR

“The first half of 2018 has shown what a strong presence the Liberian flag has in the offshore sector, with an increase in market share more than three times that of the next major open registry. This is due in no small measure to the strong fundamental understanding by the registry’s staff – many of whom have practical experience of the offshore industry – of the problems facing this fluctuating sector,” Castillero added.

Integrated IOCs

Integrated IOCs are reporting profits while SOC Petrotrin is imploding and abandoning refining, long the mainstay of the economy of Trinidad & Tobago.

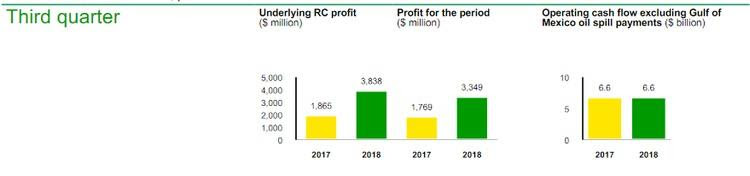

BP third quarter 2018 results

30 Oct 2018

Highlights:

Strong earnings driven by high reliability and major project delivery

- Strong earnings and cash flow:

- Underlying replacement cost profit for the third quarter of 2018 was $3.8 billion, more than double a year earlier and the highest quarterly result in more than five years, including significant earnings growth from the Upstream and Rosneft.

- Operating cash flow excluding Gulf of Mexico oil spill payments for the quarter was $6.6 billion, including a $0.7 billion working capital build (after adjusting for inventory holding gains).

- Gulf of Mexico oil spill payments in the quarter were $0.5 billion on a post-tax basis.

- Dividend of 10.25 cents a share for the third quarter, 2.5% higher than a year earlier.

- Strong operating performance:

- Very good reliability, with the highest quarterly refining availability for 15 years and BP-operated Upstream plant reliability of 95%.

- Reported oil and gas production was 3.6 million barrels of oil equivalent a day.

- Upstream underlying production, which excludes Rosneft and is adjusted for portfolio changes and pricing effects, was 6.8% higher than a year earlier, driven by ramp-up of new projects. Rosneft production of 1.2 million barrels of oil equivalent a day was 2.8% higher than last year.

Strategic delivery:- The Thunder Horse Northwest expansion project in the Gulf of Mexico and the Western Flank B project in Australia began production in October, both ahead of schedule. They are BP’s fourth and fifth Upstream major projects to start up in 2018.

- Further expansion in fuels marketing, with now around 1,300 convenience partnership sites worldwide and network growth in Mexico.

BHP transaction:

The acquisition from BHP is expected to complete on 31 October.

Reflecting confidence in cash generation and continued capital discipline, and assuming oil prices remain firm in the recent trading range, BP now expects to fund the entire transaction from available cash, rather than using equity for the deferred consideration. In this case, proceeds from the associated $5-6 billion of divestments will be used to reduce net debt.

Bob Dudley, Group chief executive, said:

‘Our focus on safe and reliable operations and delivering our strategy is driving strong earnings and growing cash flow. Operations are running well across BP and we’re bringing new, higher-margin barrels into production faster through efficient project execution. We have made very good progress with our acquisition from BHP and expect to complete the transaction tomorrow. This will transform our position in the US Lower 48 and we expect it to create significant value for BP. This progress all underpins our commitment to growing distributions for our shareholders’.

Source: BP

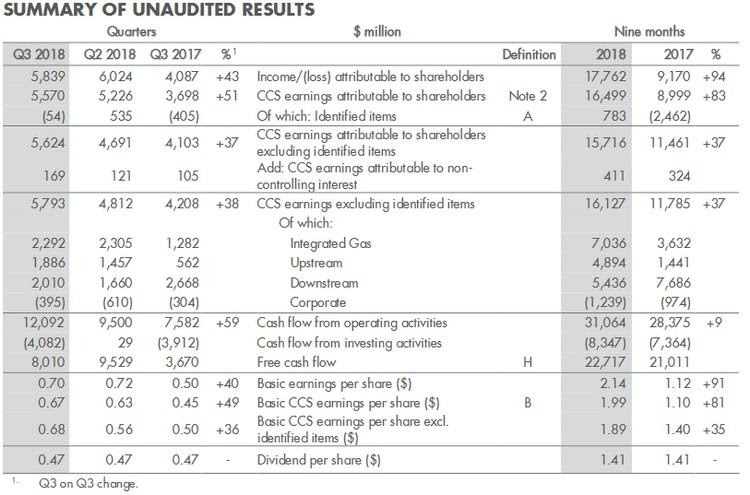

Shell third quarter 2018 unaudited results

01 Nov 2018

CCS earnings attributable to shareholders excluding identified items were $5.6 billion, compared with $4.1 billion in the third quarter 2017. Earnings primarily benefited from increased realised oil, gas and LNG prices as well as higher contributions from trading in Integrated Gas, partly offset by lower margins in Downstream, higher deferred tax charges in Upstream and adverse currency exchange effects.

Cash flow from operating activities for the third quarter 2018 was $12.1 billion, which included negative working capital movements of $2.6 billion, compared with $7.6 billion in the third quarter 2017, which included negative working capital movements of $1.3 billioni. Excluding working capital movements, cash flow from operations of $14.7 billion mainly reflected increased earnings and higher dividends received.

Total dividends distributed to shareholders in the quarter were $3.9 billion. In October, the first tranche of the share buyback programme was completed, with almost 61 million A ordinary shares bought back for cancellation for an aggregate consideration of $2.0 billion. Today, Shell launches the second tranche of the share buyback programme, with a maximum aggregate consideration of $2.5 billion in the period up to and including January 28, 2019.

Royal Dutch Shell Chief Executive Officer Ben van Beurden commented:

‘Good operational delivery across all Shell businesses produced one of our strongest-ever quarters, with cash flow from operations of $14.7 billion, excluding working capital movements. Our strong financial performance allowed us to cover the cash dividend, interest payments, share buybacks and to further pay down debt.

Our strategy remains on track. We have completed the first tranche of share buybacks, in line with our intention to purchase $25 billion of our shares by the end of 2020, and today I’m pleased to announce the second tranche. Meanwhile, the transformation of our portfolio continued, with further divestments of nonstrategic assets and the final investment decision on LNG Canada.’

Source: Shell

The petroleum industry is rolling in cash again but company bosses show devotion to austerity.

Third-quarter earnings season started with the Equinor CEO promising to “take good care of our cash” even as profit rose to a four-year high. His counterpart at Total gave a commitment to “resolutely” cut costs. Staying “laser-focused on discipline” was ConocoPhillips CEO

Analysts forecast record cash flows this year after the surge in crude prices. All majors are exceeding those estimates. Most CEOs — such as Eni boss who used $1.1 billion of surplus cash to pay down debt — show no sign of being generous with either spending or shareholder payouts.

Oil companies want new projects to be resilient, because oil prices will fall back in a cyclical market. They want to reassure investors, wary that risks of rising capex would jeopardize share buybacks. There are many reasons for caution in a market that remains uncertain and volatile. Since Brent crude rallied to $86/bbl earlier this month, it fell about $10 due to concerns over demand. These gyrations reflect risks to both supply and demand that are too big even for giants to manage: From the slump in global equity markets to weakness in the global economy; from the collapse of Venezuela’s oil industry to U.S. efforts to sanction Iran’s crude exports out of existence.

Oil chiefs are keen to avoid falling into the cost inflation trap that accompanies recovering prices. Equinor vowed not to forget the lessons of the last boom, when much of the gains from $100/bbl crude were eaten up by the rising cost of drilling, raw materials and wages.

Restraint cannot last forever, especially with investors keen for higher returns but majors should be able to afford it. For the next three years production will grow while costs and prices remain stable.

This is a sweet spot for integrated oil. They are all likely to increase shareholders returns through higher dividends and buy-backs in the coming quarters.

profit surged by more than expected at Total as rising prices combined with record production. The French company can afford a little moderation in spending while enjoying the growth benefits of a series of acquisitions and new projects.

Eni cash flow from operations doubled from a year earlier to a record $4.7 billion. The company left its dividend and capital expenditure plans unchanged and used surplus cash to pay down debt.

ConocoPhillips, the largest independent explorer, trounced estimates. It raised its full-year spending estimate by 1.7% to $6.1 billion, citing decisions outside its control such as drilling partners expanding operations.

Equinor cut planned investments for 2018 to $10 billion from $11 billion, maintained a dividend of $0.23, in line with earlier promises, and made no mention of a potential share buy-back program it’s been considering.

Gas is key to energy transition

The 2018 Offshore Energy Exhibition and Conference opened on October 23.

The day saw the close of the Offshore Wind Event that kicked off a day earlier and continued with the launch of a Global Gas Event, a new feature at Offshore Energy, building on the Offshore Energy Industry Panel which presented the current supply and demand forecasts, hot regions for the business as well as the place of gas in the overall energy mix.

Hosted by Navingo B.V.’s own Femke Perlot-Hoogeven, the conference manager, Global Gas Event speaker line-up included DNV GL’s Sverre Alvik, Clingendael International Energy Programme’s researcher Luca Franza, Neptune Energy’s Lex de Groot, SBM Offshore’s Ellen Kroijmans, and Lux Research’s Harshit Sharma.

Keynote speakers addressed the most important strategic and commercial challenges associated with the current and future gas industry.

Gas key to transition

Starting the discussion was, Svere Alvik, project director at DNV GL’s Energy Transition Outlook who discussed DNV GL’s Energy Transition Outlook 2018.

“We are approaching peak energy, and the ongoing energy transition will see large shifts in how we consume and produce energy. Gas has a key role and is likely already in 2026 to take over as the largest energy source. Improved energy efficiency, decarbonization and electrification of the energy system will make the energy system of 2050 very different from today,” he said.

DNV GL, a global quality assurance and risk management company, through its Energy Transition Outlook forecasts the energy future through to 2050.

Franza discussed Gas and Geopolitics, noting various drivers are molding different gas markets and Europe’s efforts to phase out coal for electrification, while the gas demand remains uncertain. Politicization of gas is an issue, but it is overinflated. Clingendael International Energy Programme was launched in 2001 with support from public and private institutions. It contributes to the public debate on international political and economic developments in the energy sector (oil, gas and electricity). CIEP contributions include research, events, publications, comments, lectures and training. The programme’s current research and activities revolve around the issues of the geo-political and geo-economic consequences of changing supply and demand patterns in energy, in particular, oil and natural gas, and the development of European energy markets and energy policy-making against the background of international energy market developments and climate change policies.

SBM Offshore working Mid-Scale FLNG

Ellen Kroijmans, global project office director and general manager of SBM Offshore’s Schiedam office unveiled plans to focus on opportunities in the mid-scale FLNG market.

SBM is a trailblazer in the supply and operation of large Oil FPSOs. SBM is for 20 years engaged in gas and LNG projects. With gas becoming increasingly important in the current Energy Transformation, SBM’s ambition is to further expand in the gas business. This objective is achieved through embarking on innovative products and teaming up with strategic partners.

Associated gas from the oil fields where SBM’s FPSO’s are operating could be liquefied by mid-scale floating LNG units. However, it is the matter of scale as deploying one FLNG unit to operate in tandem with a single FPSO would not be viable. In terms of technology, the move from FPSO to FLNG would not be such a huge step up for the company.

Harshit Sharma, practice lead oil & gas, at LUX Research, discussed Innovations Reducing the Oil and Gas Industry’s Environmental Footprint. With the Paris Agreement finalized, momentum around carbon and methane emissions reduction spurred the oil and gas industry to strategically position itself for the energy future. With both commercially viable solutions today and disruptive technologies in the future, Sharma highlighted the potential impact carbon emission policies, such as carbon pricing, will have on the industry. He analyzed the industry’s collaborative initiatives with external innovation sources creating genuine value in the near- and long-term vision of the industry. He elaborated on carbon pricing and shared views on oil & gas climate initiative, saying that the investment in carbon capture solutions is a positive step, a small portion of what can and should be done. Low carbon taxes and no incentives to big market players to invest in new technology make progress slow .

Sverre Alvik remarked that gas is clean and a positive in the near-term, however, in the long-term it is not clean enough. It is a solution to bring down pollution and global CO2 emissions, but it could never reach zero. Without CCS it will only be a medium-term solution, and the Paris objective can never be reached with gas alone.

The six keynote speakers from DNV GL, Crystol Energy, Staatsolie Maatschappij Suriname, OGUK, Schlumberger and GoodFuels addressed the most important strategic and commercial challenges associated with the current and future oil industry.

Gas to overtake oil in 2026

Sverre Alvik, the project director for DNV GL’s Energy Transition Outlook discussed DNV GL’s Energy Transition Outlook 2018. According to the data from the Outlook, global spending on energy is set to slow sharply because world energy demand will decline from 2035 onwards.

Decarbonization of the energy mix would be reflected in investment trends with spending on renewables set to triple by 2050. His first sentence was not what oil enthusiasts wanted to hear- that the largest energy source by 2026 will be gas. Energy demand will decline since the world is becoming more energy efficient. The oil age will not end due to a lack of oil. The ice age did. Oil will not. There would be a cost-paring between electric vehicles and those running on combustion engines by 2024 and transport was the focal point for oil.

There was a need for new oil until 2040 but oil demand will grow slowly for five years and then go flat during the 2020s. A decrease will begin in ten years time. This is earlier than some estimate. Earlier than Shell which predicts oil will peak in 2030 and BP in 2040.

Wild-cards to tip the oil price scales

Carole Nakhle, CEO of independent energy consultancy and advisory firm Crystol Energy addressed geopolitics and fundamentals of the oil sector with focus on the short and medium term. She reviewed oil prices and the effort by OPEC and NOPEC countries to stop the decrease in oil prices. Due to instabilities in-country, Iran, Iraq, Libya, Nigeria and Venezuela were difficult to predict regarding oil production. Venezuela has the lowest level of production since 1949 with a tendency to decline further, below one million barrels a day. These wild-cards will be key in the following months and will tilt the oil price up or down.

Suriname the place to be?

Rudolf Elias, CEO of Staatsolie Maatschappij Suriname, discussed prospects for the offshore industry in Suriname, a new interesting location for oil majors following the massive discoveries in neighboring Guyana. Elias spoke of the company’s plan for drilling the near offshore next year to analyze how the oil migrated to the huge Liza discovery. Seasoned offshore oil explorers Equinor, Kosmos, Apache, and Exxon acquired acreage for Suriname, hoping to replicate the exploration successes made in Guyana. Regarding the company’s plans, Elias added: “In the coming two years, we know that we will drill at least five nice wells and we now expect to find oil in the reservoir.”

UKCS still able to compete

Gareth Wynn of Oil & Gas UK explained how the mature UKCS basin adapted to compete with other commercial basins. The UKCS basin saw a steady rise in production in the next five years with this year producing 20% more than five years ago.

Adrian Cretoiu, managing director for Western Europe at Schlumberger, was the penultimate speaker. The Global Oil event was capped off by Eric van der Meer, a board advisor at GoodFuels, a producer of 2nd generation biofuels.

Industry downturn. No better time to get innovative. The innovation, collaboration and cost-reduction session focused on new technological advances in the offshore industry. The moderator was Robert Plat of Royal IHC, Dutch equipment, vessels and services provider.

In every industry downturn, service providers and operators respond with cost-reducing innovations and new forms of collaboration in various stages of the oil & gas life cycles.

Chief commercial officer of Maersk Decom, Jens Klit Thomsen, senior inspection engineer of Bluestream Offshore Malcolm Newton and Gusto MSC’s Han Tiebout presented innovations from their companies. This was the first time they filled these roles at OEEC while Plat reprised his moderator role from last year when he moderated another innovation-focused session named “Ten years of innovation, what’s next?“. Last year’s session focused on challenging processes of innovations in the current market and attempted to predict future technological innovations which could be applied in a rapid-changing offshore energy marketplace.

Thinking outside the box is key

Thomsen, former head of decommissioning business development at Maersk Supply Service and current chief commercial officer of Maersk Decom, a joint venture decommissioning company between Maersk Drilling and Maersk Supply Service, addressed the topic of integrated project and innovation. He explained how Maersk Drilling and Maersk Supply Services collaborated on decommissioning even before the merger on the Janice and James fields as well as on Leaden. Thomsen showed how each asset owned by the company was utilized to provide an integrated solution for decommissioning of the fields.

He presented practical solutions of Maersk Supply on its vessels like a flexible riser cut table on the Maersk Achiever AHTS and a six-kilometer flexible riser spool transformed from existing parts aboard the Maersk Master. Steel parts from the risers were 99,8 percent decommissioned while the plastic covers were converted to artificial grass now on a football pitch in Aberdeen.

The “think outside the box” approach and innovations never before considered in a traditional industry helped, accelerated and cheapened the Janice decom job.

Smaller ROVs, smaller vessels

Malcolm Newton, of Bluestream Offshore, a Den Helder-based subsea service provider, covered the issue of reducing the cost of subsea inspections utilizing the advances in compact ROV systems and inspection tooling. The company has an ROV fleet of 20 units and Newton was initially trained as an ROV technician before his subsea inspection career. Newton elaborated on survey and cleaning options which the company could conduct from its fleet of Seaeye Tiger and Seaeye Cougar ROVs.

Use of smaller ROVs and innovative solution on the ROVs enables Bluestream, predominantly a diving company to use smaller and smaller vessels and become cost-effective.

Safety is paramount

Han Tiebout, of Dutch design and engineering company Gusto MSC, presented the technical development and project execution of the under cantilever crane Chela. The Chela lifting and wireline operations smart crane was introduced in March this year. Chela, Greek for crab’s claw, can reach below the cantilever as well as elevate towards the main deck, providing crane access to an area usually blocked by the cantilever when drilling. The double-jointed crane can conduct a larger scope of work and, since it is remote operated, the crane operator will not do ‘blind’ lifts which was once the case and always a safety hazard. This new crane design was immediately recognized by Maersk Drilling which contracted Gusto in May to install it on the Maersk Invincible drilling rig, operating on the Valhall field for AkerBP.

Best Innovation Award

Winner was ECE Offshore B.V. and the company’s OASYS solution which improves monitoring of power cables during installation of wind farms.

Presentations came from the other two nominees, Barge Master & GustoMSC for their jointly developed S. Offshore wind feeder solution, and IHC IQIP for its Combi Lifting Spread. All three nominees come from the offshore wind industry.

Unlocking mature basins to bridge the supply gap

The Offshore Energy Exhibition & Conference (OEEC) kicked off on October 23, in Amsterdam RAI with a technical session “Exploration in a mature basin.”

Inger Salomonsen, Annemiek Asschert, Imad Mohsen, Eric van Ewijk, Nick Ford, Alexander Mollinger; Source: Navingo

With energy demand high, investments in exploration and production in mature basins, like the North Sea, could be a way to bridge the demand gap. This was the first time mature basins were discussed at OEEC.

The session was moderated by Eric van Ewijk, of EBN, a Dutch government investor in exploration, extraction and storage of oil and gas on behalf of the state.

Dutch North Sea still underexplored

Annemiek Asschert, deputy exploration manager of EBN discussed the Dutch Exploration Initiative in a mature basin. Asschert highlighted opportunities still found in the northern offshore, which was mostly underexplored. The Netherlands, although moving towards a greener future, still has to find ways to bridge the supply gap during the transition period.

The way to do so was to reshoot 3D seismic data, some of which dates back to the ‘70s. New seismic can help produce additional 100-300 bcm still trapped in the Dutch North Sea.

Government-planned reshoots are scheduled for 2020.

Offshore elephants

Alexander Mollinger of Discover Exploration surveyed unlocking the potential in a mature but still prospective basin, chasing elephants, massive oil and gas deposits in offshore deepwater. The company’s “elephants” are located offshore Comoros, New Zealand and West Africa.

Staff started their careers in the North Sea and had returned to their roots with several plays off Germany, the Netherlands and Denmark. There is an unexpected revival in the North Sea. The new FIDs since last year gave the North Sea a second life.

Discover set a target to fill the supply gap in the Netherlands when its GEms prospect goes online. The FID is expected in early 2019.

There was a higher chance of success in the North Sea while there was a higher chance for reward in New Zealand, but with significantly higher risks.

New technology and data vital in mature basin

Imad Mohsen of Tulip Oil described the way his company was developing its prospects in the North Sea. Not all mature basins were created equal. North Sea data was old and behind the times. The North Sea is a mature basin explored with 1995 technology. Some like Tulip’s Q10-A discovery had no 2D or 3D seismic but seismic shot on it by the company uncovered additional prospects around it. Seismic exploration lacking is the reason why companies left discoveries behind, underlining the need for new data.

Inger Salomonsen of Nordsøfonden Exploration discussed opportunities remaining in the Danish North Sea., Denmark has produced 3,9 billion barrels since 1972 but still has around 3 billion barrels in the ground. The session’s final speaker was Nick Ford representing EEGR.

Van Ewijk concluded that oil and gas were still needed and exploration should start in areas companies know. The big guys are gone but there is more oil and gas to be found!

World Energy

Investment of $350m over the next two years will fund conversion of the Paramount, California facility into a clean fuel refinery.

The project will enable World Energy Paramount to process 306 million gallons annually. The conversion to renewable jet, diesel, gasoline and propane will reduce both refinery and fuel emissions while supporting more than 100 advanced, green economy jobs.

World Energy Paramount said significant investments in California will create more local construction and full- time jobs. This facility is a direct and tangible result of environmental policies passed by the California State Legislature.

Assembly Speaker Anthony Rendon said: “The environmental state policies we have written are working and have paved the way for these significant investments in our communities. World Energy is demonstrating the economic potential of renewable fuels for California.”

World Energy said: “This project will transform the Paramount facility into California’s most important hub for the production and blending of advanced renewable fuels.

This investment will better enable us to deliver much needed low-carbon solutions to our customers. Importantly, with 150 million gallons of annual renewable jet production capacity, World Energy will be able to help the commercial aviation industry combat its greenhouse gas emissions.”

International Energy Agency

Exporters face unprecedented challenges

Major oil and gas exporters weathered many upheavals in recent decades but a renewed commitment to reform and economic diversification will be vital to cope with the changing dynamics of global energy. These include rising production from new sources such as shale, uncertainties over the pace of oil demand growth and deployment of new energy technologies, according to a new report from the IEA.

The analysis, the Outlook for Producer Economies – a special report in the World Energy Outlook series – examined six resource-dependent economies that are pillars of global energy supply: Iraq, Nigeria, Russia, Saudi Arabia, United Arab Emirates and Venezuela. It assessed how they might fare to 2040 under a variety of price and policy scenarios.

The rollercoaster in oil prices over the last decade has brought into sharp relief the structural weaknesses in many of the major exporters. Since 2014, the net income available from oil and gas fell by between 40% (in Iraq) and 70% (in Venezuela), with wide-ranging consequences for economic performance.

The volatility of hydrocarbon revenues presents dilemmas for countries whose budgets depend on them, especially if their economies and finances are not resilient. The extent to which producer countries steer through essential economic transformation can have major implications for energy markets, global environmental goals, and energy security, according to the report.

The new report comes at a time of high oil prices, a double-edged sword. Higher revenues provide the means to reform, but they can also appear to reduce its urgency. However, as in the past, higher energy prices encourage production elsewhere while accelerating structural changes in demand, which affect the producers’ long-term markets.

“More than at any other point in recent history, fundamental changes to the development model of resource-rich countries look unavoidable,” said Dr. Fatih Birol, the IEA’s executive director. “Following through with the announced reform initiatives is essential, as failure to take adequate action would compound future risks for producer economies as well as for global markets.”

The countries examined are very diverse and the report considers a wide range of experiences and prospects. Many have plans to boost investment and growth in the non-oil sectors of their economics. Venezuela is an example of how badly things can turn out when economic and energy headwinds gather strength.

Some of the largest producers face strong pressures from rising numbers of young people entering the workforce. Over 50% of the population across the Middle East is under the age of 30; the proportion is over 70% in Nigeria. In many , income from oil and gas will not be large enough to provide for these growing populations, even in scenarios where oil demand continues to grow to 2040 and prices remain relatively robust.

The energy sector has an important part to play in the reform agenda. This report focuses on six key responses: capturing more domestic value from hydrocarbons, for example via petrochemicals; using natural gas as a means to support diversified growth; harnessing the large but under-utilized potential for renewable energy, especially solar; phasing out subsidies that encourage wasteful consumption; ensuring sufficient investment in the upstream (the ability to maintain oil and gas revenues at reasonable levels is vital for economic stability); and playing a role in deploying new energy technologies, such as carbon capture, utilisation and storage.

The reform process should be much wider than energy; but it relies on a well-functioning energy sector. Successful reform programs can open a broader range of strategic options for producers, as well as new opportunities for engagement on a range of energy issues. There is a lot at stake.

Chevron sees double in 3Q earnings

U.S. Oil major Chevron doubled its third quarter earnings on the back of higher crude oil prices.

Chevron reported earnings of $4 billion for third quarter 2018, compared with $2 billion in the third quarter of 2017.

Included in the current quarter were a write-off, an asset impairment, and a non-recurring contractual settlement totaling $930 million in the upstream segment, and a gain of $350 million on the sale of southern Africa refining, marketing and lubricant assets.

Foreign currency effects decreased earnings in the 2018 third quarter by $51 million, compared with a decrease of $112 million a year earlier.

Chevron’s sales and other operating revenues in third quarter 2018 were $42 billion, compared to $34 billion in the year-ago period.

Chevron Chairman and CEO, Michael Wirth, said: “Our strong financial results reflect higher production and crude oil prices coupled with a continued focus on efficiency and productivity.

Net oil-equivalent production of 2.96 million barrels per day represents our highest quarter ever. Ramp-up of Wheatstone in Australia and the Permian Basin in Texas and New Mexico drove a production increase of 9 percent over the prior year quarter.”

U.S. upstream operations earned $828 million in third quarter 2018, compared with a loss of $26 million a year earlier. The improvement reflected higher crude oil realizations and production, partially offset by higher depreciation and exploration expenses, primarily reflecting a $550 million write-off of the Tigris Project in the Gulf of Mexico.

The company’s average sales price per barrel of crude oil and natural gas liquids was $62 in third quarter 2018, up from $42 a year earlier. The average sales price of natural gas was $1.80 per thousand cubic feet in third quarter 2018, unchanged from the prior year’s third quarter. Net oil-equivalent production of 831,000 barrels per day in third quarter 2018 was up 150,000 barrels per day from a year earlier. Production increases from shale and tight properties in the Permian Basin in Texas and New Mexico and base business in the Gulf of Mexico were partially offset by the impact of asset sales of 19,000 barrels per day. The net liquids component of oil-equivalent production in third quarter 2018 increased 25 percent to 654,000 barrels per day, while net natural gas production increased 14 percent to 1.06 billion cubic feet per day.

ExxonMobil third quarter earnings up 57 pct

Oil major ExxonMobil boosted its third quarter earnings by 57 percent as crude and natural gas prices strengthened compared to the same period last year.

According to its financial report , the company’s earnings increased by 57% to $6.2 billion in the third quarter of 2018 compared to $3.97 billion in the same period last year.

ExxonMobil’s revenues rose to $76.6 billion from $61.1 billion in the prior-year quarter.

Oil-equivalent production was 3.8 million barrels per day, down 2 percent from the third quarter of 2017. Excluding entitlement effects and divestments, liquids production increased 6 percent, as growth in North America more than offset decline and higher downtime. Natural gas volumes decreased 4 percent.