Colombia

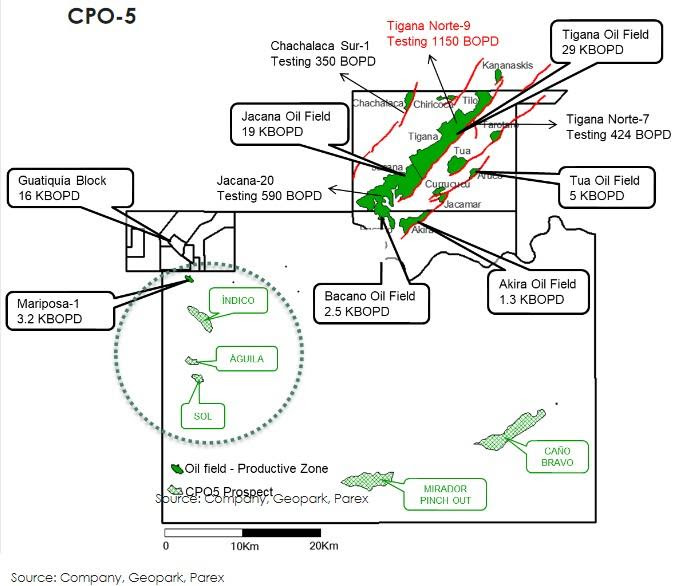

Amerisur Resources spuds Calao-1X exploration well in the CPO-5 block

04 Feb 2019

Amerisur Resources has announced that the spudding of Calao-1X, an exploration well on the CPO-5 block using rig E-2029, occurred on 1 February 2019.

Calao-1X is the second well to be drilled from the Indico pad to determine the prospectivity of the Lower Sands (‘LS3’) formation around the Indico discovery. As previously announced, initial analysis by the Company indicated that a 283 feet gross, 209 feet net, oil column is present in the LS3 formation at Indico-1.

Calao-1X will be a directional well, with a planned total measured depth of approx. 11,940 feet, targeting a structure alongside Indico to the southwest, towards the Aguila structure. On a simple structural basis, the Company estimates potential resources at Calao-1X of between 2 and 9.8 MMBO gross. However, given the results at Indico-1, which indicate the potential for combination trapping, the Company believes potential resources may be significantly higher. The drilling of Pavo Real-1, which targets a similar structure to Calao adjoining Indico to the northeast, will follow Calao-1X.

Amerisur holds a 30% non-operated interest in the CPO-5 block which is 70% owned and operated by ONGC Videsh (‘the Operator’). The Company will make a further announcement in due course once the well has been drilled and logged.

John Wardle, CEO of Amerisur Resources, said:

‘Following the positive result from Indico-1, we are delighted to report the spudding of Calao-1X from the Indico pad to determine the size of the play. We look forward to sharing the results with our shareholders throughout this busy, and potentially transformational, period for Amerisur, which has already delivered material reserves and production growth on the basis of the Indico discovery.’

Source: Amerisur Resources

Frontera Energy signs farm-in with Parex Resources

07 Feb 2019

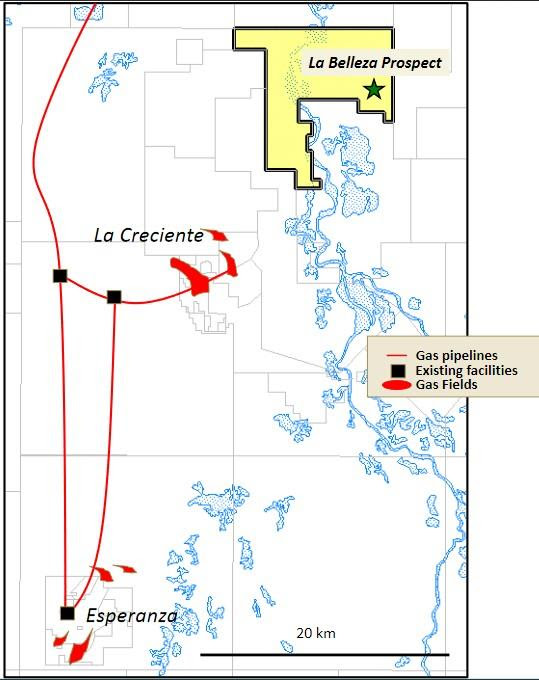

Location of VIM-1 Block (Source: Parex Resources)

Source: Frontera Energy

Frontera Energy has signed a farm-in agreement with Parex Resources, which is subject to Agencia Nacional de Hidrocarburos (‘ANH’) approval. Under the agreement, Frontera has received a 50% working interest in the VIM-1 Block in the Lower Magdalena Valley basin in Colombia in exchange for funding 100% of the first $10 million of the drilling, testing and completion costs of the La Belleza-1 exploration well, after which costs on the block will be split 50/50 with Parex.

The farm-in presents an exciting growth opportunity for Frontera and it is currently expected that the well will commence drilling during the second quarter of 2019. Capital expenditures associated with the farm-in agreement were included as part of the exploration capital budget for 2019.

Source: Frontera Energy

Fure Vinga bunkers LNG in Port of Cartagena

Fure Vinga bunkera LNG in Port of Cartagena

Image courtesy of BBG

Hamburg-based Nauticor, a unit of Linde, in cooperation with the Spanish utility company, Naturgy, bunkered liquefied natural gas to the Furetank’s Fure Vinga in the Port of Cartagena.

Fure Vinga, the second LNG-fueled vessel in the company’s fleet, received 120 tons of the chilled fuel from six tanker trucks, Bahía de Bizkaia Gas (BBG)

The 149.9 meters-long Fur Vinga, built by China’s Avic Dingheng Shipbuilding was delivered last year to Furetank.

It was also the first in a series of six LNG-fueled vessels ordered by the partners in the Swedish Gothia Tanker Alliance, Furetank, Älvtank and Erik Thun.

U.S. sanctions on Venezuela are a blessing to Colombian oil

Photo: Amerisur Resources, Colombia.

(Bloomberg) — U.S. Gulf refiners are bidding up prices for Colombian crude amid sanctions on Venezuelan imports, historically one of America’s top oil suppliers.

Colombian crude has strengthened on the back of harsher restrictions against state oil company Petroleos de Venezuela SA, a self-imposed curtailment in Canadian production and output cuts agreed on by OPEC and its allies.

Executives at Colombia SOC Ecopetrol SA, , are closely monitoring the situation in Venezuela and the impact of sanctions. The company is benefiting as it is has been able to “reliably supply customers” as Venezuelan production has fallen, CFO Jaime Caballero said in an earnings call.

“We are also seeing a big strengthening of the favorable differentials in terms of the crude we sell,” he said. “Compared to the double-digit differentials in the fourth quarter of last year, we’re now back to the single digits.”

Flagship Colombian oil Castilla, a direct competitor against heavy, sour Venezuelan oil, was sold for a discount of $4/bbl to global benchmark Brent for cargoes loading in March. That compares with a discount of $9.80 for cargoes loading in February, according to people with knowledge of the situation. More cargoes were sold to the U.S., causing Asian buyers to complain about the high price levels, the people said.

Traditional buyers of Venezuelan oil are finding alternatives. Valero Energy Corp. has bought Canadian crude to help plug the hole, according to a person familiar with the matter. PBF Energy Inc., which used to buy Venezuelan oil for its Chalmette refinery in Louisiana, bought Mexican Talam. Even Citgo Petroleum Corp., the U.S. refining unit of embattled PDVSA, got a little help from PetroChina Co. Ltd. to gain access to Colombian oil Vasconia.

While oil production in Venezuela fell to a 69-year low in 2018, Colombia is seeing a rebirth of activity, producing 898,965 bopd in January, the highest since May 2016 amid production from new oil fields.

Partners Launch Climate Transparency Hub in Grenada and the Caribbean

STORY HIGHLIGHTS

The Caribbean Cooperative MRV Hub, a project of the GHG Management Institute, aims to empower English-speaking CARICOM countries to efficiently develop GHG inventories and mitigation assessments, and track NDCs.

The Hub will enable countries to cooperate on technical challenges related to climate change mitigation, share expertise to foster regional excellence, and generate stronger policy-relevant carbon accounting.

The Hub is structured for long-term sustainability beyond the duration of the project, which is expected to run through July 2023.

21 February 2019: Project implementation partners have launched a climate transparency hub that will help to strengthen measurement, reporting and verification (MRV) of climate action under the Paris Agreement on climate change in the Caribbean region.

The Caribbean Cooperative MRV Hub, which was formally launched during a meeting of English-speaking Caribbean countries at St. George University in Grenada from 5-6 February 2019, will enable countries to cooperate on technical challenges related to climate change mitigation, share expertise to foster regional excellence, and generate stronger policy-relevant carbon accounting.

The MRV Hub, a project of the Greenhouse Gas (GHG) Management Institute, aims to empower English-speaking Caribbean Community (CARICOM) countries to efficiently develop GHG inventories and mitigation assessments, and track Nationally Determined Contributions (NDCs). The Hub is geared towards enhanced and sustainable technical GHG capacity for domestic policy making and national reporting to the UNFCCC.

Planned activities of the Hub include:

-

- operating with digital coordination systems;

- convening a steering committee;

- conducting GHG capacity needs assessments;

- mentoring and training Caribbean experts, including expert mentoring trips for

- country-specific technical issues;

- multi-country working sessions at the Hub;

- co-developing streamlined MRV and projections tools and guidance;

- co-producing transparent MRV and mitigation projection outputs; and

- developing frameworks for Hub sustainability and improvement to suit countries’ needs.

As a regional cooperative, the Hub will provide expert training, mentoring and institutional support to further enhance the technical work of countries, filling gaps where needed and empowering national experts to expand and improve their MRV outputs.

The Hub is structured for long-term sustainability beyond the duration of the project, which is expected to run through July 2023. The Hub, which represents a cost-effective regional approach to cooperatively preparing data and reporting, will be documented in an MRV Hub Framework so that countries may continue Hub operations.

The Hub is housed at St. George’s University. The 12 participating countries are Antigua and Barbuda, Barbados, the Bahamas, Belize, Dominica, Grenada, Guyana, Jamaica, Saint Kitts and Nevis, Saint Lucia, Saint Vincent and the Grenadines, and Trinidad and Tobago.

The Hub is supported by the UNFCCC, the Windward Islands Research and Education Foundation, the UN Development Programme (UNDP) and the UN Environment Programme (UNEP), among others. [UNFCCC Press Release] [GHG Management Institute Press Release] [Caribbean Cooperative MRV Hub] [Summary of Hub]

Columbia

Gran Tierra Energy acquires strategic assets in Putumayo and Llanos Basins from Vetra Energia

Following its announcement on Feb 20, Gran Tierra Energyreports that it has entered into sale agreements with Vetra Energía to purchase all of the issued and outstanding shares of Vetra’s wholly owned subsidiary, Vetra Southeast, Vetra E&P’s 50% working interest in the Putumayo-8 block (‘PUT-8’), Vetra E&P’s 100% working interest in the Llanos-5 Block (‘LLA-5’), and Vetra E&P’s entire interest in the Suroriente Block, in exchange for aggregate cash consideration of $104.2 million.

The closing of the Transactions is subject to the satisfaction or waiver of customary conditions, including compliance by each party in all material respects with certain of its covenants. The Transactions related to Vetra Southeast, Suroriente and LLA-5 are expected to close on or before March 11, 2019, following the provision of notice to the Superintendence of Industry and Commerce of the Republic of Colombia, with the Transaction related to Suroriente closing immediately following the Transactions related to Vetra Southeast. The Transaction related to PUT-8 is subject to a right of first refusal.

Click here for previous announcement: Gran Tierra Energy acquires strategic assets in Putumayo and Llanos Basins

Source: Gran Tierra Energy

22 Feb 2019

Gran Tierra Energy has entered into agreements with private companies (the ‘Vendors’) to acquire the Vendors’:

Working interest (‘WI’) in and operatorship of the Suroriente Block, which would increase Gran Tierra’s WI in Suroriente from 15.83% to 52%

50% WI in and operatorship of the Putumayo-8 Block (‘PUT-8’), which is contiguous with Suroriente and Gran Tierra’s PUT-31 Block (100% WI)

100% WI in the Llanos-5 Block (‘LLA-5’), which is contiguous with Gran Tierra’s LLA-1, -10 and -70 Blocks, representing a new core area for the Company

The purchase price for this acquisition is $104.2 million, subject to certain adjustments and the satisfaction of certain customary conditions. All dollar amounts are in United States (‘U.S.’) dollars unless otherwise indicated.

All reserves, future net revenue and production are on a WI before royalties basis unless otherwise indicated. Transfer of operatorship is subject to regulatory recognition and the terms of any applicable joint operating agreements.

Key Acquisition Highlights

- Highly strategic acquisition further strengthens and consolidates Gran Tierra’s position as the premier operator and top landholder in the Putumayo Basin, and makes the Company the operator of 100% of its Putumayo Blocks

- Consistent with Gran Tierra’s focused strategy to grow the Company’s exploration, development and production opportunity portfolio within Colombia

- As of December 31, 2018, the Vendors’ Suroriente WI had:

- Proved plus probable (‘2P’) reserves of 6.1 million barrels of oil (‘MMbbls’)

- $175 million of 2P before tax free cash flow forecasted over the next 5 years

- 2P before tax net present value discounted at 10% (‘NPV10’) of $140 million

- 2P plus possible (‘3P’) reserves of 8.1 MMbbls

- 3P NPV10 of $202 million

- Current production of approx. 2,200 barrels (‘bbl’) of oil per day (‘bopd’)

- By securing operatorship of Suroriente, Gran Tierra expects to accelerate waterflooding on the Block, which is forecasted to further increase value

- Gran Tierra believes PUT-8 contains at least two exciting drill-ready exploration prospects, which could potentially be drilled in 2019 using existing pads.

- The addition of the LLA-5 Block compliments Gran Tierra’s existing acreage in the Llanos Basin and creates a contiguous land base of 620,000 gross acres (525,000 net acres) located near the prolific Cano Limon production complex and the Capachos block

- The acquisition is expected to be funded from cash on hand and existing credit facilities with no need for external financing

- In order to maintain the Company’s currently strong balance sheet, Gran Tierra intends to reduce its 2019 capital program by approximately $30 million to $50 million, with an immaterial expected impact on the Company’s 2019 average production

- Gran Tierra plans to provide updated 2019 guidance with the release of its fourth quarter and year end 2018 results on or before February 27, 2019

Gary Guidry, President and Chief Executive Officer of Gran Tierra, commented

‘This highly strategic acquisition further consolidates our dominant position in the Putumayo Basin, with assets that are highly complementary to our existing land base, and adds a new core area in the Llanos Basin. A major US independent has also acquired a material position in the Putumayo and Llanos basins, offsetting Gran Tierra.

The acquisition immediately adds production, reserves, cash flow and drill-ready exploration prospects to our portfolio. We are excited by the opportunity to accelerate Suroriente’s already successful waterflood in the Cohembi N Sand field and to apply technical knowledge from this field to our N Sand plays across the Putumayo Basin.

This acquisition fits perfectly with Gran Tierra’s focused strategy by further expanding our portfolio in the proven, underexplored Putumayo Basin, with access to established infrastructure. We will also become the operator of 100% of our Putumayo asset base and have complete flexibility and control over the allocation of our capital in the Putumayo.’

Source: Gran Tierra Energy

Cuba Meteorite

VinaleS (Cuba): A piece of a meteorite that fell in Cuba on Friday.—AFP

Witnesses reported seeing a ball of fire and a smoke trail in a clear midday sky, and a rain of black stones fell on the tourist town of Vinales and other parts of Pinar del Rio province. Explosions were also heard and a smoke trail seen in Havana. There were no reports of damage or injuries. “We were coming from the centre … and we saw a ball of fire cross the sky,” said Spanish tourist Jesus Nicolas, 34, in Havana. “Sure, it was a meteorite and a very big one.”

Amid speculation on social media, state media in Cuba denied that a plane had crashed and called it a “natural, physical phenomenon”. Later on Friday, a statement from Cuba’s Ministry of Science and the Environment read on a nightly newscast confirmed that it was a meteorite strike.

Efren Jaimez Salgado, head of the Environmental Geology, Geophysics and Risks department of Cuba’s Institute of Geophysics and Astronomy, earlier told state newspaper Granma that preliminary information suggests a meteorite or meteorite fragments struck an area near the Mural of Prehistory in Vinales and that a team was heading to the area to take samples.

Photos published showed small black stones which when split open had dark red veins. People in the archbishopric of Pinar del Rio confirmed that two strong explosions were heard and in rural areas of the province rumblings were heard and some houses shuddered.

Published in Dawn, February 3rd, 2019

Building Resilience to Natural Disasters and Climate Change in Grenada and the Caribbean

Grenada

February 13, 2019

Ladies and gentlemen, good afternoon! It is an honor for me to speak with you today on my first visit to Grenada.

Before coming here, I had often heard Grenada being referred to as an “Isle of Spice.” This simple catch-phrase distinguished it from other Caribbean destinations. I have been curious to know what this term means. Over the past day or so, I have seen the beauty and diversity of Grenada’s natural landscape, tasted exceptional – and spiced up – food, and enjoyed interactions with intelligent, dynamic, and very welcoming people. I am of course just beginning my learning process. But I am already very hungry to know more about the ingredients of Grenada’s story, including what drove its impressive economic recovery over the past few years.

Earlier this week, I traveled to Dominica. I was moved by the change in the landscape in Dominica I saw from the devastation the category 5 hurricane Maria in 2017. And that, of course, reminded me of Grenada’s own trials in 2004 during Hurricane Ivan. Your remarkable recovery since then, and Dominica’s over the past year, testify to the determination of the people of the Caribbean to build a better future in the face of extraordinary challenges.

I am pleased to meet today with Grenada’s officials, parliamentarians, business community, and development partners. This is part of an important discussion of how to work together to further strengthen your resilience against natural disasters and climate change. It also is an element of a broader strategy to attain strong and sustainable growth in Grenada and the Caribbean region.

A Collective Strategy

This idea of a collective strategy to address climate challenges is what I would like to examine in greater depth this afternoon. But let’s first set the stage with an overview of the economic prospects for the ECCU region and Grenada.

The regional outlook is improving. Several countries have seen a pickup in economic activity owing to greater tourism demand. This has been supported by robust growth in the United States. In this context, Grenada registered strong growth of about 5 percent in 2017. And we estimate it grew at a similar pace last year. Solid tourism demand is expected to continue this year. That should help the continuing recovery in the region, including in countries hit by the 2017 hurricanes.

But there are still significant risks. The risks posed by natural disasters in the region are touching all sectors and are intensifying with climate change.

Financial sector risks continue to be present. While there is some progress with reforms in this area, long-standing weaknesses need to be addressed. The legacy of bad loans continues to weigh on economic prospects. Corresponding banking relationships also need to be monitored.

As regards the external sector, current account deficits remain sizable. This highlights the region’s competitiveness and growth challenges.

Finally, for a long time, this region has been struggling with the challenge of high public debt in the context of low growth. To be sure, public debt in the ECCU has recently been declining. But this trend in some countries reflects temporary factors, including revenues from the Citizenship-by-Investment Programs. As a result, the ECCU debt target of 60 percent of GDP by 2030 remains elusive for most countries – although not for Grenada, which has made impressive progress. Stronger fiscal discipline will be essential to achieving this target across the region.

Grenada’s Important Breakthroughs

Against this background, Grenada has made important breakthroughs in coping with its economic challenges.

First, let’s take a closer look at the policy response to natural disasters, an area where Grenada is also making notable progress. Hurricane Ivan caused damage equal to more than 200 percent of GDP. Over the past decade, your country has pursued a strategy centered on rebuilding infrastructure and enhancing institutional capacity. Public investment plans increasingly include resilient infrastructure projects. The authorities’ climate change policy and national adaptation plan of 2017 are detailed and costed. Sectoral plans are progressing. A dedicated Ministry for Climate Resilience was recently created. The recent successes in obtaining grant financing from climate funds — including for the water project — are notable achievements. And innovative hurricane clauses were introduced into debt contracts to limit resource outflows in case of damaging storms.

After the deep economic crisis 5 years ago, your government decided on a policy of fiscal discipline — supported by the fiscal responsibility law — that helped break a pattern of high debt and low growth. This fiscal adjustment helped cut the deficit by almost 10 percent of GDP. It also reduced public debt from 108 percent of GDP in 2013 by more than 40 percentage points by now.

Despite fears that such a large fiscal adjustment would hurt output, growth in Grenada has averaged 5 and a half percent annually. This compares favorably with other countries in the ECCU and the Caribbean. Crucially, the government’s strong efforts received broad backing from domestic stakeholders through a negotiated Social Compact.

To sum up, Grenada’s authorities have done remarkable things in bringing down debt and leaving better public finances for future generations. These important gains are a national asset and a product of the hard work of all Grenadians. They deserve to be protected.

These are all positive developments, but it is necessary to recognize that more can be done—by Grenada and the broader Caribbean region. The focus on post-disaster recovery should be supplemented with better all-around preparedness. The experience with hurricanes in the region continues to highlight the need to build more resilient infrastructure and have resources to address problems immediately.

There are many examples of good practices around the world. New Zealand and the Philippines created effective natural disaster funds. Japan demonstrates the importance of both prioritizing resilient infrastructure and budget mechanisms for contingency planning.

Project Planning and Implementation

To make further progress in these areas, Grenada and other Caribbean countries should focus their efforts on improving project planning and implementation capacity. Grant financing of the Caribbean region, despite some of the successes, remains small compared to the needs. And the focus of donors should also shift from supporting recovery to supporting preparedness.

Preparing for a disaster can make a huge difference. It is more effective than responding after the event. Preparation not only reduces the immediate impact. Our research shows that, over time, it helps boost growth and private investment and reduce emigration and brain drain. Most Caribbean countries can do much more in terms of developing resilient public infrastructure and protecting key sectors of the economy.

That’s why a comprehensive approach—or Disaster Resilience Strategy, as we call it–to address climate-related issues is so important. This country-driven strategy would take stock of ongoing efforts to cope with natural disasters, prioritize actions, build consensus across all stakeholders, and anchor progress in upgrading capacity. A crucial goal would be to work toward long-term economic sustainability.

The strategy would start from a realistic assessment of the economic impact of climate-related risks and desirable policy responses. Policymakers also need to integrate these assessments and policies explicitly into their operational plans, including budget policies. And this strategy should be fully financed for a long multi-year period.

The comprehensive strategy also requires policy responses to be practical. In this regard, I see three pillars:

First, more investment in emergency preparedness and response, such as early warning systems, shelter and security, and distribution of essential goods and services.

Second, an emphasis on resilient physical and social infrastructure. There are several practical steps that can help reduce the risks posed by future storms. For example, investing in disaster-resilient infrastructure, enforcing land-use and zoning rules to limit deforestation and coastal exposure, and ensuring appropriate building standards.

And third, steps to ensure financial resilience will be crucial. These include insurance mechanisms and cash reserves that allow disaster preparation and post-disaster response to progress swiftly and effectively.

What is needed for such a strategy to be carried out in practice in the region?Stronger government efforts, particularly in upgrading budgeting and project execution capacity, are key to this success. It would also involve maintenance of strong fiscal discipline and acceleration of progress in reforms to rationalize and improve efficiency of all public spending. This would greatly support the countries’ credibility with the international community.

The International Dimension

There is an important international dimension to implementation of this strategy.At the recent joint IMF/World Bank/IDB high-level conference on building resilience in the Caribbean, many leaders voiced their support for “building an alliance” among key stakeholders. There is a need for regional coordination.

And there is an important role of international development partners. They could offer help in formulating and implementing such a comprehensive and integrated resilience strategy, thereby addressing the resource and implementation capacity issues that all small countries face. We see a clear case for coordinating the work of the IMF, the World Bank, multilateral development banks, bilateral partners, insurance companies, the climate funds, and business.

The IMF could contribute to the resilience strategy in a number of areas.

We could help the countries develop an appropriate macroeconomic policy-framework. One way to accomplish this is with a new analytical tool jointly developed with the World Bank. This so-called Climate Change Policy Assessment provides a big-picture assessment of a country’s policy response to climate change. It takes into account the macroeconomic, fiscal, and other policy requirements and identifies key areas for improvement. These assessments already have been undertaken by several countries in the Caribbean and other regions of the world and one is being presently conducted in Grenada.

The IMF could identify fiscal actions that create space for resilience projects in the most efficient way; incentivize climate-smart activities such as clean energy; and at the same time ensure debt sustainability. It could also help provide technical assistance in areas that target resilience.

And finally, the Fund could help develop integrated policy advice on financial resilience, including on the design and use of insurance and debt instruments. In this context, we could contribute to financing, including through engaging donor funds.

These are significant challenges. Climate change — in the Caribbean and around the world — demands a response from the international community. Grenada and the other small states are feeling the effects of this looming crisis in a way that is very different from most other countries. You are paying the price for a problem you did not create. So, the time has come for a global response. Let’s work together to achieve solutions that protect my home, your home and our way of life.

Thank you!

Statement by IMF : Meeting with Prime Minister of Grenada Keith Mitchell

Mr. Tao Zhang, Deputy Managing Director of the International Monetary Fund (IMF), met yesterday with The Rt. Hon. Prime Minister Keith Mitchell in the city of St. George’s. Following the meeting, Mr. Zhang made the following statement:

“It is my pleasure to visit Grenada for the first time. I would like to thank Prime Minister Mitchell, members of the Parliament and cabinet, and representatives of the private sector for their warm welcome, hospitality, and productive discussions.

“During our meeting, Prime Minister Mitchell and I discussed the latest economic developments. I congratulated him on Grenada’s successful record of policy implementation. Growth is among the highest in the Caribbean region, unemployment is falling, and public debt is declining.

“PM Mitchell and I also discussed the importance of early preparedness to protect Grenada against natural disasters and climate change and key dimensions of resilience-building policies. We at the IMF value our relationship with Grenada and stand ready to help the country build a more prosperous and inclusive economy.”

IMF Communications Department

PRESS OFFICER: RANDA ELNAGAR

IMF Communications Department

EMAIL: MEDIA@IMF.ORG

IMF Staff Concludes Visit to Panama

A staff team of the International Monetary Fund (IMF), led by Alejandro Santos, visited Panama during February 6–13, 2019. At the conclusion of the visit, Mr. Santos issued the following statement:

“Panama remains one of the most dynamic growing countries in Latin America, but economic activity has been less dynamic than expected, with growth estimated at 3.6 percent in the first nine months of 2018 (compared to 5.6 percent in the same period of 2017), reflecting broad slowdown in key sectors, including construction, which was partly affected by the strike in April–May. While there are clear signs of an economic recovery, the prolonged cyclical weakness has led us to revise down our growth estimate for 2018 to 3.9 percent (from 4.3 percent estimated in our recent report) and to 6.0 percent for 2019 (from 6.3 percent). The authorities estimate the overall fiscal deficit of the non-financial public sector at 2 percent of GDP for 2018 (from a revised deficit of 1.9 percent in 2017), which is in line with the modified fiscal responsibility law. Progress on financial integrity continues, including the recent approval of the legislation to criminalize tax evasion and the introduction of a procedural tax code among other legislative amendments.

“Panama’s fundamentals remain solid, with the economy on track to recover from the temporary slowdown and subsequently converging to its potential growth of 5½ percent over the medium term, and no overheating pressures in the horizon as inflation is projected to remain contained at about 2 percent, while credit is expected to grow in line with income. The external position is expected to strengthen significantly as the large copper mine starts production this year, and oil prices stay low, while remaining well financed by FDI. The balance of risks to the outlook is tilted to the downside, mostly related to fears of rising trade protectionism, potentially weaker global outlook, and continued oversupply in some segments of the domestic property market.

“We reiterated the need to sustain fiscal discipline and to improve the fiscal position as the economy recovers in the years ahead, aided by the stronger fiscal framework, to keep the public debt to GDP ratio on a downward trajectory. We encouraged the authorities to rely less on turnkey projects and to continue improving their statistical framework by bringing it closer to best practices. We also recommended the authorities to further raise revenue including through improvements in revenue administration and to rein in current spending to support growth-enhancing investments.

“While the banking system remains well capitalized and liquid with low non-performing loans, the authorities should continue to advance their efforts towards strengthening banking regulation and supervision (including FinTech). It will also be important to reinforce the structural reform agenda to maintain strong inclusive and sustainable growth, including by strengthening policies related to education, social security and public health services. Finally, sustained efforts to enhance AML/CFT and tax transparency are of paramount importance to strengthen Panama’s position as a regional financial center.”

The mission is grateful to the authorities for their kind hospitality, excellent cooperation and open discussions.

IMF Communications Department

MEDIA RELATIONS

PRESS OFFICER: RAPHAEL ANSPACH

PHONE: +1 202 623-7100EMAIL: MEDIA@IMF.ORG